A federal lien does indeed take precedence over a mortgage in New York State. This is because federal liens, such as those for unpaid taxes or student loans, are considered superior to other types of liens, including mortgages. This means that if a property owner in New York has a federal lien placed against their property, it will supersede any existing mortgage. The federal government has the authority to place liens on property to collect debts owed to it, and these liens have priority over other financial claims against the property. This can have significant implications for property owners and lenders in New York, as it means that the federal government can potentially seize property to satisfy a debt, even if there is an existing mortgage.

Explore related products

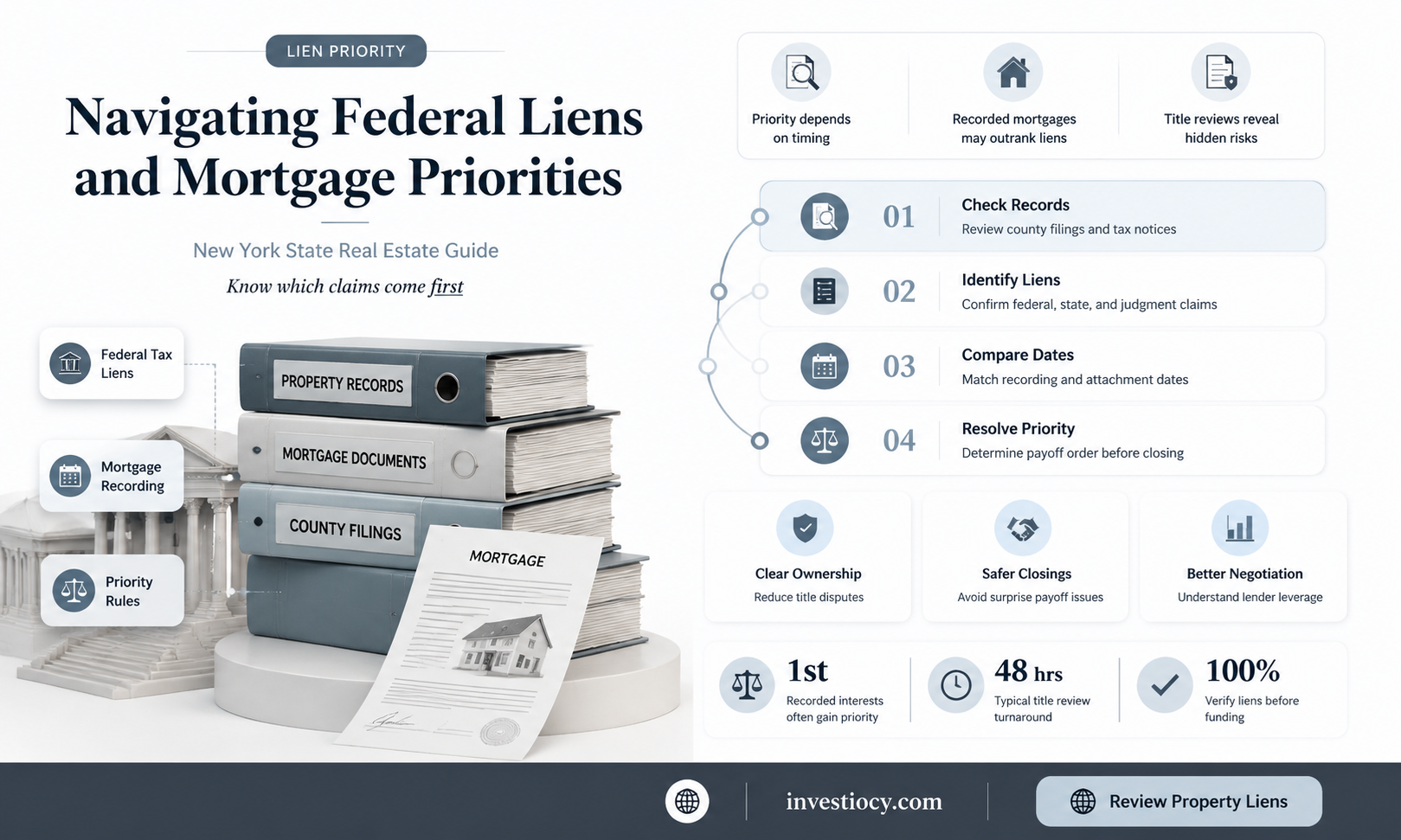

What You'll Learn

- Definition of Federal Lien: A federal lien is a legal claim by the government on a debtor's property

- Impact on Mortgage: A federal lien can potentially supersede a mortgage, affecting the lender's rights

- New York State Laws: Specific state laws in New York may influence the precedence of federal liens over mortgages

- Legal Precedents: Court rulings and legal precedents can determine how federal liens interact with mortgages in New York

- Implications for Property Owners: Property owners in New York need to understand the implications of federal liens on their mortgages

![]()

Definition of Federal Lien: A federal lien is a legal claim by the government on a debtor's property

A federal lien represents a legal claim by the government on a debtor's property, arising from unpaid taxes or other financial obligations owed to federal entities. This lien is a powerful tool in the government's arsenal for collecting debts, as it allows them to place a claim on real estate, personal property, or other assets owned by the debtor.

In the context of New York State, a federal lien can indeed supersede a mortgage under certain circumstances. This occurs when the federal lien is properly filed and recorded, giving it priority over other liens or encumbrances on the property, including mortgages. The process typically involves the government issuing a Notice of Federal Tax Lien, which is then recorded with the appropriate state or local authorities.

Once a federal lien is in place, it can have significant implications for the debtor's ability to sell or refinance their property. Potential buyers or lenders may be hesitant to proceed with a transaction if a federal lien is present, as it could complicate the transfer of ownership or the establishment of a new mortgage.

To avoid such complications, debtors are often advised to address federal liens promptly by either paying off the underlying debt or negotiating a settlement with the government. In some cases, a debtor may be able to obtain a release of the lien by demonstrating that they have made arrangements to satisfy the debt or by showing that the lien was improperly filed.

In conclusion, a federal lien is a serious matter that can have far-reaching consequences for debtors, particularly in situations where it supersedes a mortgage. Understanding the nature and implications of federal liens is crucial for individuals and businesses alike, as it can help them navigate the complexities of debt collection and property ownership.

Securing Your Dream Home: Does a Down Payment Guarantee a Mortgage?

You may want to see also

Explore related products

![]()

Impact on Mortgage: A federal lien can potentially supersede a mortgage, affecting the lender's rights

A federal lien can have significant implications for a mortgage, potentially superseding it and affecting the lender's rights. This is particularly true in New York State, where the interplay between federal liens and mortgages is governed by specific statutes and case law. When a federal lien is placed on a property, it can take precedence over existing mortgages, depending on the circumstances and the type of lien involved.

For instance, a federal tax lien can arise when a property owner fails to pay federal taxes. In such cases, the Internal Revenue Service (IRS) can file a lien against the property, which may take priority over a mortgage. This can lead to complications for the lender, as they may not be able to foreclose on the property or collect on the mortgage until the federal lien is satisfied.

Similarly, a federal judgment lien can be filed against a property when a court orders the property owner to pay a debt or damages. If the property owner does not comply, the creditor can file a lien against the property, which may again supersede a mortgage. In New York State, the priority of such liens is determined by the date they are filed, with earlier liens generally taking precedence over later ones.

The impact of a federal lien on a mortgage can be further complicated by the specific terms of the mortgage agreement. Some mortgages may include clauses that address the issue of federal liens, either by requiring the borrower to keep the property free of such liens or by specifying how the lender will handle the situation if a lien is filed. In any case, it is crucial for lenders to be aware of the potential for federal liens to affect their rights and to take steps to mitigate any risks.

One way for lenders to protect themselves is to conduct thorough due diligence before issuing a mortgage. This includes checking for any existing federal liens on the property and ensuring that the borrower has a clear understanding of their obligations under the mortgage agreement. Additionally, lenders may want to consider including specific language in their mortgage agreements that addresses the issue of federal liens and outlines the lender's rights and remedies in such situations.

In conclusion, the impact of a federal lien on a mortgage in New York State can be significant, potentially superseding the mortgage and affecting the lender's rights. Lenders must be aware of this risk and take steps to protect themselves, including conducting due diligence and including specific language in their mortgage agreements. By doing so, they can help ensure that their interests are protected and that they are able to collect on their mortgages even in the face of federal liens.

Navigating Divorce and Mortgages: Understanding the Legal Override

You may want to see also

Explore related products

![Discussion on Land Bank of the State of New York ... 1914 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

New York State Laws: Specific state laws in New York may influence the precedence of federal liens over mortgages

In the realm of real estate and finance, the interplay between federal liens and mortgages can be complex, especially in a state like New York with its unique legal landscape. New York State laws have specific provisions that can influence the precedence of federal liens over mortgages, which is crucial for lenders, borrowers, and investors to understand.

One key aspect of New York law is the concept of "lien priority," which determines the order in which liens are paid off in the event of a foreclosure or sale of the property. Generally, federal liens, such as those from the IRS or SBA, take precedence over mortgages and other state liens. However, New York State has certain statutes that can modify this priority, particularly in cases involving tax liens or other state-imposed liens.

For instance, under New York Real Property Law § 291, a state tax lien can have priority over a federal lien if the state lien was filed before the federal lien. This is a significant exception to the general rule of federal lien priority and can have substantial implications for lenders and borrowers. Additionally, New York's homestead exemption laws can further complicate the situation, as they may limit the amount of equity that can be reached by creditors, including federal lien holders.

Another important consideration is the impact of bankruptcy on lien priority. In bankruptcy proceedings, the automatic stay can halt foreclosure actions and alter the priority of liens. New York State laws may provide additional protections or requirements in this context, which can affect the outcome of bankruptcy cases involving federal liens and mortgages.

In conclusion, while federal liens typically take precedence over mortgages, New York State laws can significantly influence this dynamic. Understanding these nuances is essential for navigating the complexities of real estate finance and ensuring compliance with state and federal regulations.

Boosting Your Mortgage Amount: The Power of a Cosigner Revealed

You may want to see also

Explore related products

![]()

Legal Precedents: Court rulings and legal precedents can determine how federal liens interact with mortgages in New York

In the realm of New York real estate law, the interplay between federal liens and mortgages is a complex and nuanced area. Court rulings and legal precedents play a pivotal role in shaping how these financial instruments interact, often determining the priority and enforcement of each. A federal lien, which can arise from various government claims such as unpaid taxes or defaulted student loans, can indeed supersede a mortgage in certain circumstances, but this is not a straightforward process.

The determination of whether a federal lien takes precedence over a mortgage in New York State hinges on several factors, including the timing of the lien's filing, the nature of the debt, and the specific legal procedures followed. For instance, a federal tax lien, once properly filed, can attach to all property owned by the debtor, including real estate, and may take priority over a subsequently recorded mortgage. However, this priority is not absolute and can be challenged under certain conditions, such as when the mortgagee can demonstrate that they were unaware of the lien at the time of lending.

One key legal precedent in this area is the case of United States v. Rodgers, which established that a federal tax lien can be superior to a mortgage even if the mortgage was recorded before the lien, as long as the government can show that the mortgagee had actual knowledge of the lien. This ruling underscores the importance of thorough due diligence in real estate transactions, as failure to uncover and address potential federal liens can lead to significant legal and financial repercussions.

In practice, navigating the intersection of federal liens and mortgages requires a deep understanding of both federal and state laws, as well as the procedural intricacies involved in lien filing and enforcement. Real estate professionals, including attorneys, title companies, and lenders, must stay abreast of the latest legal developments and precedents to effectively advise their clients and mitigate risks associated with federal liens.

In conclusion, while federal liens can indeed supersede mortgages in New York State under certain conditions, the legal landscape is fraught with complexities and nuances that necessitate careful consideration and expert guidance. By understanding the relevant court rulings and legal precedents, stakeholders can better navigate this challenging area of law and protect their interests in real estate transactions.

Understanding Cosigner Rights in a Mortgage Agreement

You may want to see also

Explore related products

![]()

Implications for Property Owners: Property owners in New York need to understand the implications of federal liens on their mortgages

Property owners in New York must be aware of the significant implications that federal liens can have on their mortgages. A federal lien, which is a legal claim against a property, can arise from various federal debts or obligations, such as unpaid taxes, student loans, or judgments from federal courts. When a federal lien is placed on a property, it can affect the property owner's ability to sell, refinance, or obtain a new mortgage.

One of the primary implications for property owners is the potential for a federal lien to take precedence over other liens, including mortgages. This means that if a property owner defaults on their mortgage payments, the federal lien holder may have the right to foreclose on the property before the mortgage lender. This can lead to a loss of the property for the owner and may also impact their credit score and financial stability.

Another implication is that federal liens can remain on a property for an extended period, often up to 20 years or more, depending on the type of lien and the circumstances. This can make it difficult for property owners to sell their property or obtain a new mortgage, as potential buyers or lenders may be hesitant to take on a property with an outstanding federal lien.

Property owners in New York should also be aware that federal liens can be filed without their knowledge or consent. This can happen if a federal agency determines that the property owner owes a debt or obligation to the government. In such cases, the property owner may only become aware of the lien when they attempt to sell or refinance their property.

To mitigate the implications of federal liens, property owners should take proactive steps to manage their finances and ensure that they are in compliance with all federal laws and regulations. This includes paying taxes on time, making student loan payments, and addressing any outstanding judgments or debts. Additionally, property owners should regularly review their credit reports and property records to ensure that there are no liens filed against their property without their knowledge.

In conclusion, federal liens can have significant implications for property owners in New York, affecting their ability to sell, refinance, or obtain a new mortgage. By understanding the potential consequences of federal liens and taking proactive steps to manage their finances, property owners can minimize the risks associated with these legal claims and protect their property and financial well-being.

Understanding Fannie Mae Mortgage Notes: Grace Periods Explained

You may want to see also

Frequently asked questions

A federal lien is a legal claim or charge against property to secure the payment of a debt or obligation owed to the federal government. In New York State, a federal lien can supersede a mortgage if it is properly filed and recorded. This means that the federal lien takes priority over the mortgage, and the property owner must satisfy the federal lien before the mortgage can be paid off.

The filing of a federal lien can significantly impact the mortgage process in New York State. If a federal lien is filed against a property, it can delay or even prevent the mortgage from being approved. This is because the federal lien takes priority over the mortgage, and the lender will not want to take on the risk of the lien being enforced and the property being seized.

There are several common reasons for a federal lien to be filed against a property in New York State. These include unpaid federal taxes, unpaid child support, unpaid student loans, and unpaid judgments or fines. If a property owner fails to pay these debts or obligations, the federal government may file a lien against the property to secure payment.