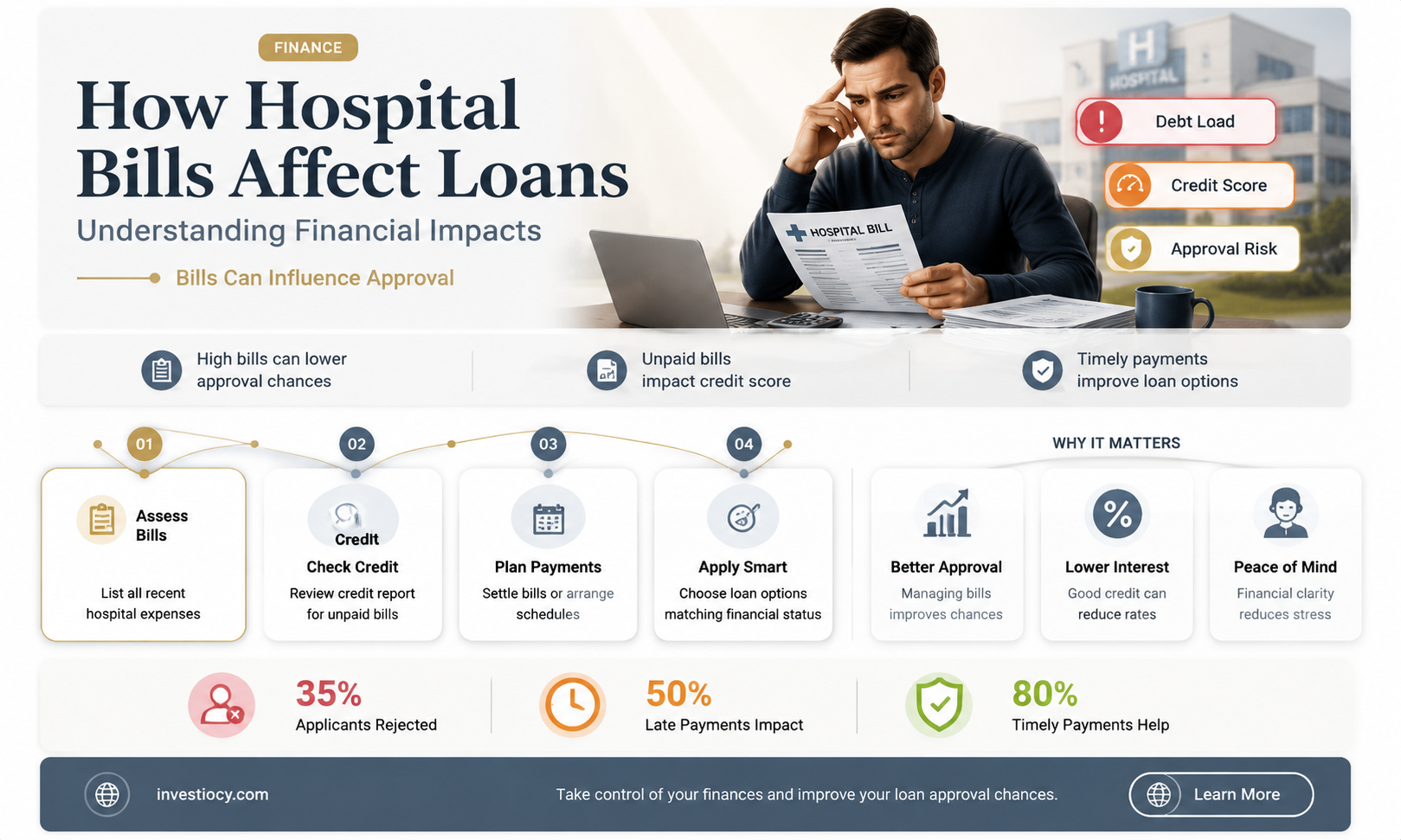

Hospital bills can significantly impact loan decisions, as lenders often scrutinize an applicant's credit history and outstanding debts. High medical expenses can lead to financial strain, causing individuals to miss payments or accumulate debt, which in turn affects their credit score. This can make it challenging to secure loans or result in higher interest rates. Lenders may also consider the applicant's ability to repay the loan, taking into account their current financial obligations, including medical bills. Therefore, it is crucial for individuals to manage their medical expenses responsibly and maintain a good credit history to improve their chances of obtaining favorable loan terms.

| Characteristics | Values |

|---|---|

| Impact on Credit Score | Hospital bills can negatively impact credit scores if left unpaid or if payment is delayed, as they may be reported to credit bureaus. |

| Loan Approval | Unpaid hospital bills can affect loan approval decisions, as lenders may view them as a sign of financial irresponsibility or instability. |

| Debt-to-Income Ratio | High hospital bills can increase an individual's debt-to-income ratio, which is a key factor lenders consider when making loan decisions. |

| Credit Utilization | If hospital bills are charged to credit cards, they can increase credit utilization, which may also negatively impact credit scores and loan eligibility. |

| Loan Terms | Borrowers with unpaid hospital bills may face less favorable loan terms, such as higher interest rates or shorter repayment periods. |

| Credit Report Errors | It's important to check credit reports for errors related to hospital bills, as these can be disputed and potentially removed, improving creditworthiness. |

| Medical Collections | Hospital bills that go into collections can have a more severe impact on credit scores and loan decisions than regular late payments. |

| Bankruptcy Considerations | In some cases, individuals may consider bankruptcy to discharge overwhelming hospital debt, but this should be a last resort as it can have long-term financial consequences. |

| Negotiation with Hospitals | Borrowers can try negotiating with hospitals to set up payment plans or reduce the amount owed, which may help mitigate the impact on loan decisions. |

| Credit Counseling | Seeking credit counseling can provide guidance on managing hospital bills and improving overall financial health, which can positively influence loan decisions. |

| Loan Alternatives | Individuals with hospital bills may need to explore alternative loan options, such as secured loans or loans from credit unions, which may have more lenient lending criteria. |

| Financial Assistance Programs | Some hospitals offer financial assistance programs for low-income patients, which can help reduce or eliminate outstanding bills. |

| Medicaid and Insurance | Understanding how Medicaid and other insurance programs cover hospital bills can help individuals avoid unexpected costs and manage their finances more effectively. |

| Budgeting and Financial Planning | Creating a budget and financial plan can help individuals prioritize payments, including hospital bills, and demonstrate financial responsibility to lenders. |

| Credit Score Monitoring | Regularly monitoring credit scores can help individuals track the impact of hospital bills and take steps to improve their creditworthiness over time. |

Explore related products

What You'll Learn

- Medical Debt Impact: How outstanding hospital bills can influence loan eligibility and interest rates

- Credit Score Connection: The relationship between unpaid medical bills and credit score fluctuations

- Loan Approval Process: Steps lenders take to evaluate borrowers with medical debt

- Debt-to-Income Ratio: The role of hospital bills in calculating this crucial financial metric

- Options for Managing Debt: Strategies to handle medical bills to improve loan approval chances

![]()

Medical Debt Impact: How outstanding hospital bills can influence loan eligibility and interest rates

Outstanding hospital bills can significantly impact an individual's loan eligibility and interest rates. When lenders assess a borrower's creditworthiness, they scrutinize their credit report for any signs of financial distress or mismanagement. Medical debt, particularly when it is unpaid or in collections, can be a red flag that signals to lenders that the borrower may be a higher risk. This can lead to loan denials or, if approved, higher interest rates to compensate for the perceived increased risk.

One of the primary ways medical debt affects loan decisions is through its impact on credit scores. Credit scoring models, such as those developed by FICO and VantageScore, take into account various factors including payment history, credit utilization, and the presence of collections or judgments. Unpaid medical bills can result in negative marks on a credit report, which can lower a credit score and make it more challenging to secure loans at favorable terms.

Moreover, medical debt can also influence the debt-to-income ratio (DTI), which is another critical factor lenders consider when making loan decisions. A high DTI indicates that a significant portion of a borrower's income is dedicated to debt repayment, which can limit their ability to take on additional loans. Medical debt, especially if it is substantial, can contribute to a higher DTI, thereby affecting loan eligibility and interest rates.

Furthermore, the type of medical debt and how it is handled can also play a role in loan decisions. For instance, medical bills that have been sent to collections or have resulted in judgments may be viewed more negatively by lenders compared to medical bills that are simply outstanding but not yet in collections. Additionally, some lenders may differentiate between medical debt and other types of debt, potentially treating medical debt more leniently due to its often-unpredictable nature.

In conclusion, outstanding hospital bills can have a profound impact on loan eligibility and interest rates. Borrowers with unpaid medical debt may face challenges in securing loans or may be subject to higher interest rates. It is essential for individuals to manage their medical debt responsibly and to be aware of how it can affect their financial health and borrowing capabilities.

Understanding Hospice Care: Equipment Loans and Support Services

You may want to see also

Explore related products

![]()

Credit Score Connection: The relationship between unpaid medical bills and credit score fluctuations

Unpaid medical bills can have a significant impact on an individual's credit score, which in turn can affect their ability to secure loans. This is because credit scores are calculated based on a person's credit history, including their ability to pay off debts on time. When medical bills go unpaid, they can be sent to collections, which can then be reported to the credit bureaus and negatively impact the individual's credit score.

The relationship between unpaid medical bills and credit score fluctuations is complex. On one hand, medical bills are often unexpected and can be difficult to pay off, especially for those without adequate insurance coverage. On the other hand, lenders may view unpaid medical bills as a sign that an individual is not responsible with their finances, and therefore may be less likely to lend to them.

It's important to note that not all medical bills will have the same impact on an individual's credit score. For example, a small medical bill that is paid off quickly may not have any significant impact, while a large medical bill that goes unpaid for an extended period of time could have a much more serious effect. Additionally, some lenders may be more lenient when it comes to medical bills, as they understand that these types of debts are often unavoidable.

Individuals who are struggling with unpaid medical bills should take steps to address the issue as soon as possible. This may include contacting the hospital or medical provider to set up a payment plan, or seeking assistance from a credit counselor. By taking proactive steps to address unpaid medical bills, individuals can help to mitigate the negative impact on their credit score and improve their chances of securing loans in the future.

In conclusion, the relationship between unpaid medical bills and credit score fluctuations is a complex one, but it is clear that unpaid medical bills can have a significant negative impact on an individual's credit score. By understanding this relationship and taking steps to address unpaid medical bills, individuals can help to protect their credit and improve their financial standing.

Reviving Dreams: The Current Status of HomePath Renovation Loans

You may want to see also

Explore related products

![]()

Loan Approval Process: Steps lenders take to evaluate borrowers with medical debt

Lenders evaluate borrowers with medical debt through a meticulous loan approval process, which involves several key steps. The first step is to assess the borrower's creditworthiness by reviewing their credit report and score. Medical debt can significantly impact credit scores, as unpaid bills may be reported to credit bureaus, leading to derogatory marks. Lenders will scrutinize these marks to determine the borrower's ability to manage debt responsibly.

The next step in the process is to verify the borrower's income and employment status. Lenders need to ensure that the borrower has a stable source of income to repay the loan. Medical debt can sometimes lead to financial instability, especially if the borrower has been out of work due to illness or injury. Therefore, lenders may require additional documentation, such as pay stubs or tax returns, to confirm the borrower's financial situation.

Lenders also consider the borrower's debt-to-income ratio (DTI), which compares the total monthly debt payments to the gross monthly income. A high DTI ratio, particularly one that is inflated by medical debt, may raise concerns about the borrower's ability to take on additional debt. Some lenders may have specific DTI requirements, and borrowers with medical debt may need to provide explanations or documentation to mitigate the impact of their debt on their DTI ratio.

Another important factor in the loan approval process is the borrower's payment history. Lenders will review past payment behavior to predict future payment patterns. Late payments or defaults on medical bills can be a red flag, indicating that the borrower may struggle to repay the loan. Borrowers with medical debt should be prepared to explain any late payments or defaults and provide evidence of their efforts to resolve these issues.

Finally, lenders may consider the borrower's overall financial situation, including their savings, assets, and other debts. Borrowers with medical debt may need to demonstrate that they have a plan to manage their debt and that they have sufficient financial reserves to handle unexpected expenses. This could involve providing a budget, a debt repayment plan, or proof of a savings account.

In conclusion, the loan approval process for borrowers with medical debt involves a thorough evaluation of creditworthiness, income, employment, DTI ratio, payment history, and overall financial situation. Borrowers should be prepared to provide detailed documentation and explanations to address any concerns raised by their medical debt. By understanding these steps and taking proactive measures to improve their financial standing, borrowers with medical debt can increase their chances of securing a loan.

Exploring Honda's Extended Loan Options: 84 Months and Beyond

You may want to see also

Explore related products

![]()

Debt-to-Income Ratio: The role of hospital bills in calculating this crucial financial metric

Hospital bills can significantly impact your debt-to-income ratio, a critical financial metric lenders use to determine your creditworthiness. This ratio compares your total monthly debt payments to your gross monthly income. A high debt-to-income ratio can signal to lenders that you may struggle to repay additional debt, potentially leading to loan denials or higher interest rates.

When calculating your debt-to-income ratio, it's essential to include all sources of debt, including hospital bills. These bills can be particularly problematic because they often result from unexpected medical emergencies, which can lead to substantial, unplanned expenses. If you're unable to pay these bills in full, they may be sent to collections, further damaging your credit score and increasing your debt-to-income ratio.

To mitigate the impact of hospital bills on your debt-to-income ratio, it's crucial to manage your medical debt proactively. This may involve negotiating payment plans with healthcare providers, seeking financial assistance programs, or consolidating medical debt into a single, more manageable loan. By addressing hospital bills promptly, you can prevent them from ballooning into a larger financial burden that could jeopardize your loan approval chances.

In addition to managing existing hospital bills, it's also important to consider the potential future impact of medical expenses on your debt-to-income ratio. This may involve reviewing your health insurance coverage to ensure it adequately protects you from high out-of-pocket costs or exploring supplemental insurance options to cover unexpected medical bills. By taking a proactive approach to managing both current and future medical debt, you can maintain a healthier debt-to-income ratio and improve your overall financial stability.

Exploring Homestyle Loan Coverage: Does Landscaping Qualify?

You may want to see also

![]()

Options for Managing Debt: Strategies to handle medical bills to improve loan approval chances

Medical bills can significantly impact loan approval chances due to their high costs and the potential for long-term financial strain. To manage debt effectively and improve loan approval odds, consider the following strategies:

Firstly, prioritize communication with healthcare providers. Negotiate payment plans directly with hospitals or clinics to spread out costs over time. Many medical facilities offer interest-free payment options for patients who are upfront about their financial limitations. This proactive approach can prevent bills from being sent to collections, which would negatively impact credit scores.

Secondly, explore options for consolidating medical debt. Personal loans or balance transfer credit cards can be used to combine multiple medical bills into a single, more manageable payment. This strategy can simplify debt repayment and potentially lower interest rates, making it easier to pay off the debt quickly and avoid long-term financial burdens.

Thirdly, consider seeking assistance from a credit counselor. Non-profit credit counseling agencies can provide guidance on managing debt, including medical bills. They may offer debt management plans that can help negotiate lower interest rates and fees with creditors, as well as provide budgeting advice to ensure timely repayments.

Lastly, it's crucial to monitor credit reports for any errors related to medical billing. Disputing inaccuracies can help improve credit scores, which in turn can enhance loan approval chances. Regularly reviewing credit reports also helps in identifying any potential issues early on, allowing for prompt resolution and minimizing the impact on loan applications.

By implementing these strategies, individuals can effectively manage medical debt, protect their credit scores, and improve their chances of loan approval.

Frequently asked questions

Yes, hospital bills can affect your loan application. Lenders often review your credit report and medical debts can appear on it, potentially impacting your credit score and loan eligibility.

Lenders may view medical debt differently because it's often considered an unexpected expense. However, it's still a debt that you're responsible for paying, and it can affect your creditworthiness if not managed properly.

A single hospital bill may not significantly impact your credit score if it's paid promptly. However, if it remains unpaid or goes to collections, it can have a more substantial negative effect on your credit score.

To prevent hospital bills from affecting your loan decisions, it's essential to pay them on time. If you're unable to pay the full amount, consider setting up a payment plan with the hospital. Additionally, regularly monitoring your credit report can help you identify and address any medical debts that may impact your credit score.

Some loan programs may have more lenient guidelines regarding medical debt, but it's crucial to research and compare different lenders and loan options. You may also want to consult with a financial advisor or loan officer to discuss your specific situation and find the best loan program for you.