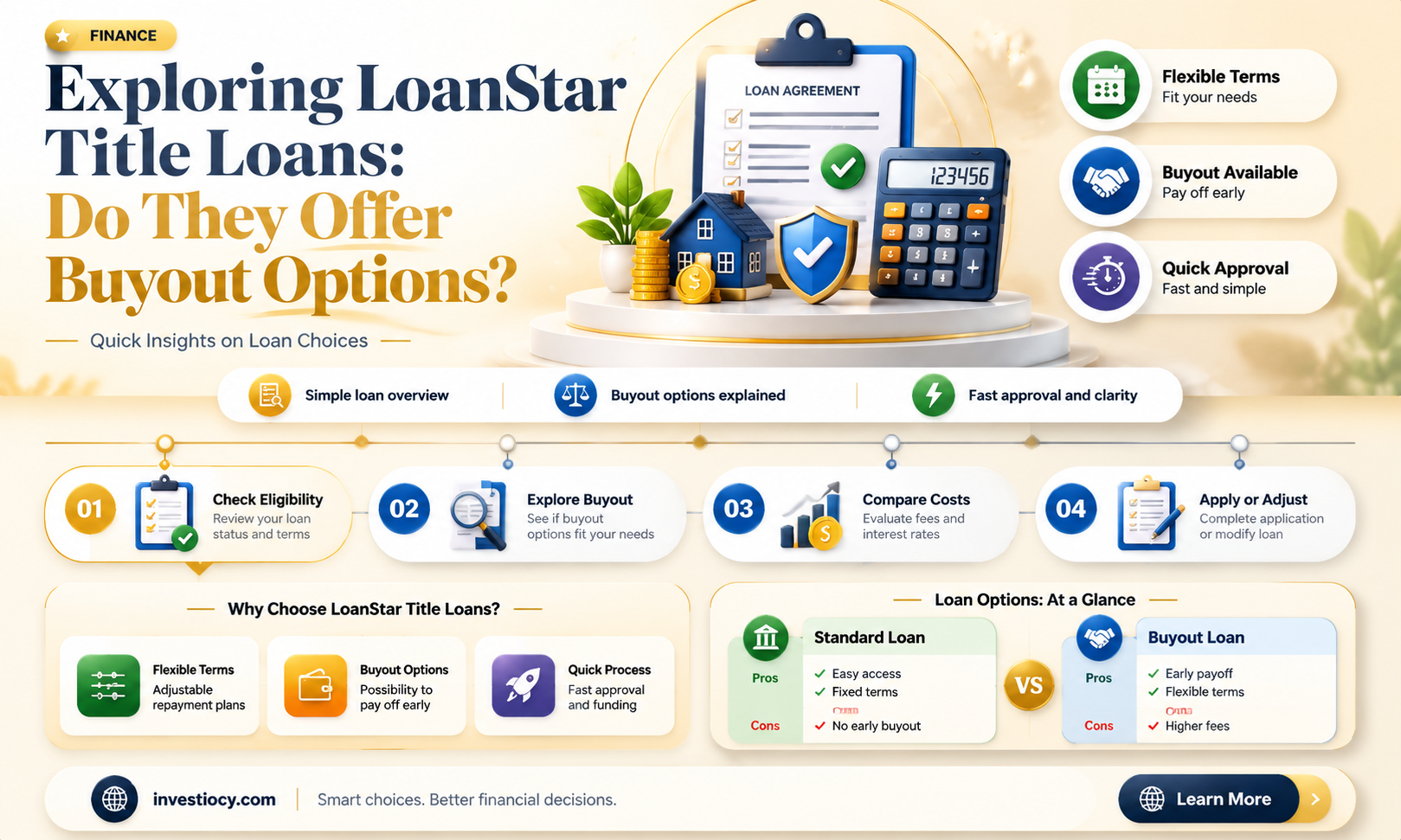

LoanStar Title Loans is a financial services company that specializes in providing title loans to individuals in need of quick cash. Title loans are a type of secured loan where the borrower's vehicle title is used as collateral. One common question that potential customers may have is whether LoanStar Title Loans offers buyout options for existing title loans from other lenders. A buyout, in this context, would mean that LoanStar Title Loans pays off the remaining balance of a title loan from another company and takes over the loan, potentially offering better terms or lower interest rates to the borrower. Understanding whether LoanStar Title Loans provides this service can be crucial for individuals looking to refinance their existing title loans or consolidate their debt.

Explore related products

$69.49 $110

What You'll Learn

- LoanStar Title Loans: Overview and services offered, including buyout options for existing loans

- Buyout Process: Steps and requirements for LoanStar to buy out a title loan from another lender

- Benefits of Buyouts: Advantages of transferring a title loan to LoanStar, such as lower rates or better terms

- Eligibility Criteria: Conditions that must be met for LoanStar to consider a buyout of a title loan

- Customer Reviews: Experiences and testimonials from clients who have used LoanStar's buyout services for title loans

![]()

LoanStar Title Loans: Overview and services offered, including buyout options for existing loans

LoanStar Title Loans is a financial services company that specializes in providing title loans to individuals who need quick access to cash. Title loans are a type of secured loan where the borrower's vehicle title is used as collateral. LoanStar Title Loans offers a variety of services, including the option to buy out existing title loans from other lenders.

One of the unique features of LoanStar Title Loans is their buyout program, which allows customers to refinance their existing title loans with LoanStar. This can be beneficial for borrowers who are looking for better interest rates, longer repayment terms, or simply want to consolidate their debt with a single lender. The buyout process typically involves LoanStar paying off the remaining balance of the borrower's existing loan and then issuing a new loan with different terms.

To qualify for a buyout with LoanStar Title Loans, borrowers must meet certain criteria, such as having a clear title to their vehicle and sufficient equity in the vehicle to secure the new loan. The amount of money that can be borrowed through a buyout will depend on the value of the vehicle and the borrower's ability to repay the loan.

LoanStar Title Loans also offers other services, such as new title loans for those who do not already have a loan, as well as loan extensions and payment plans for existing customers. The company prides itself on providing fast and friendly service, with many locations across the United States.

In summary, LoanStar Title Loans is a financial services company that offers a range of services related to title loans, including the option to buy out existing loans from other lenders. This can be a useful tool for borrowers who are looking to refinance their debt or consolidate multiple loans into a single payment.

Understanding Loan Reporting During Forbearance Periods: A Guide

You may want to see also

Explore related products

![]()

Buyout Process: Steps and requirements for LoanStar to buy out a title loan from another lender

LoanStar Title Loans offers a buyout process for individuals looking to transfer their existing title loan from another lender. This service can be beneficial for those seeking better interest rates, more favorable loan terms, or simply wanting to consolidate their debts. The buyout process involves several key steps and requirements that must be met to ensure a smooth transition.

Firstly, the borrower must initiate contact with LoanStar Title Loans and express their interest in a buyout. During this initial consultation, the borrower will need to provide basic information about their current loan, including the lender's name, the outstanding balance, and the terms of the loan. LoanStar will then conduct a preliminary review to determine if the buyout is feasible and beneficial for both parties.

If the preliminary review is positive, LoanStar will require the borrower to submit a formal application for the buyout. This application will include detailed information about the borrower's financial situation, the vehicle being used as collateral, and the existing loan. LoanStar may also request additional documentation, such as proof of income, vehicle registration, and insurance.

Once the application is submitted, LoanStar will perform a thorough evaluation of the borrower's creditworthiness and the value of the vehicle. This evaluation will help LoanStar determine the terms of the new loan, including the interest rate, repayment schedule, and any additional fees. If the evaluation is satisfactory, LoanStar will extend an offer to the borrower, outlining the terms of the buyout and the new loan.

Upon accepting the offer, the borrower will need to sign the necessary paperwork to finalize the buyout. LoanStar will then handle the process of paying off the existing loan and transferring the title to the new loan. The borrower will receive a new loan agreement and will begin making payments to LoanStar according to the terms outlined in the offer.

Throughout the buyout process, it is essential for the borrower to be transparent and provide accurate information. Any discrepancies or omissions could delay the process or result in a denial of the buyout. Additionally, the borrower should carefully review the terms of the new loan to ensure that it meets their financial needs and that they are able to make the required payments.

In conclusion, LoanStar Title Loans' buyout process can be a valuable option for individuals looking to refinance their existing title loan. By following the necessary steps and meeting the requirements, borrowers can potentially secure better loan terms and improve their financial situation. However, it is crucial for borrowers to approach the process with caution and to fully understand the implications of entering into a new loan agreement.

State-by-State Variations in Loan Regulations: What You Need to Know

You may want to see also

Explore related products

![]()

Benefits of Buyouts: Advantages of transferring a title loan to LoanStar, such as lower rates or better terms

Transferring a title loan to LoanStar can offer several distinct advantages, particularly in terms of financial savings and improved loan conditions. One of the primary benefits is the potential for lower interest rates. By refinancing with LoanStar, borrowers may be able to secure a more competitive rate, which can significantly reduce the overall cost of the loan over its lifetime. This is especially beneficial for those who initially took out a title loan at a high interest rate and are looking to save money.

Another advantage of transferring a title loan to LoanStar is the possibility of better loan terms. LoanStar may offer more flexible repayment options, longer loan durations, or lower monthly payments, which can make managing the loan more manageable for borrowers. Additionally, LoanStar might provide more transparent and straightforward communication, helping borrowers to better understand their loan obligations and avoid unexpected fees or penalties.

Furthermore, LoanStar's buyout process can be relatively quick and easy, allowing borrowers to transition from their current lender with minimal hassle. This can be particularly appealing to those who are dissatisfied with their current lender's service or are looking to consolidate multiple loans into a single, more manageable payment.

It's also worth noting that LoanStar may offer additional services or benefits that can further enhance the value of transferring a title loan. For example, they might provide financial counseling or resources to help borrowers improve their financial literacy and make better decisions about their loans.

In summary, transferring a title loan to LoanStar can offer a range of benefits, including lower interest rates, better loan terms, a more streamlined process, and potentially additional services to support borrowers. These advantages can make LoanStar a more attractive option for those looking to refinance their title loan and improve their financial situation.

Exploring LoanStar College's TRS Options: A Comprehensive Guide

You may want to see also

![]()

Eligibility Criteria: Conditions that must be met for LoanStar to consider a buyout of a title loan

To be eligible for a title loan buyout by LoanStar, several key conditions must be met. Firstly, the vehicle in question must have a clear title, free from any liens or encumbrances. This ensures that LoanStar can legally take possession of the vehicle if necessary. Additionally, the vehicle must be in good working condition and have a certain minimum value to be considered for a buyout. LoanStar will typically require an appraisal to determine the vehicle's value and condition.

Another important criterion is the borrower's credit history. LoanStar will likely perform a credit check to assess the borrower's ability to repay the loan. A good credit score can improve the chances of eligibility, while a poor credit score may result in a higher interest rate or even denial of the buyout. It's also essential for the borrower to have a steady source of income, as this demonstrates their ability to make regular payments on the loan.

LoanStar may also have specific requirements regarding the age and mileage of the vehicle. Typically, vehicles that are too old or have excessively high mileage may not be eligible for a buyout. Furthermore, the borrower must be at least 18 years old and a U.S. citizen or permanent resident to qualify for a title loan buyout.

In some cases, LoanStar may require additional documentation, such as proof of insurance or a vehicle inspection report. It's crucial for borrowers to provide all necessary information and documentation promptly to expedite the eligibility process. Meeting these criteria does not guarantee approval, but it does increase the likelihood that LoanStar will consider a buyout of the title loan.

Does Loan Rejection Affect CIBIL Score: Understanding the Impact

You may want to see also

![]()

Customer Reviews: Experiences and testimonials from clients who have used LoanStar's buyout services for title loans

LoanStars has been a game-changer for many individuals struggling with title loans from predatory lenders. One client, Sarah, shared her experience of how LoanStars helped her escape a cycle of debt. She had taken out a title loan to cover an unexpected medical expense but found herself unable to keep up with the high interest rates and fees. LoanStars stepped in, buying out her loan and offering her a more manageable repayment plan. Sarah was able to regain control of her finances and even improve her credit score over time.

Another client, John, was facing a similar situation but with multiple title loans from different lenders. LoanStars worked with him to consolidate his debt into a single, more affordable loan. John was impressed by the professionalism and empathy of the LoanStars team, who took the time to understand his unique circumstances and tailor a solution that fit his needs. Thanks to LoanStars, John was able to avoid the threat of repossession and get back on track financially.

These success stories are not isolated incidents. LoanStars has a proven track record of helping clients like Sarah and John take control of their title loans and improve their financial well-being. Their buyout services have earned them a reputation as a trusted and reliable partner for those seeking relief from predatory lending practices.

Exploring the Loan Signing System: Exam Requirements Uncovered

You may want to see also

Frequently asked questions

Yes, LoanStar Title Loans does offer buyout services. They can assist you in buying out your existing title loan from another lender.

The process typically involves contacting LoanStar Title Loans, providing details about your current title loan, and working with them to determine the buyout amount and terms. They will then handle the necessary paperwork and transactions to transfer the loan to their company.

Some potential benefits include lower interest rates, more flexible repayment terms, or better customer service compared to your current lender. However, it's important to carefully review the terms and conditions of the new loan to ensure it's the right choice for your financial situation.