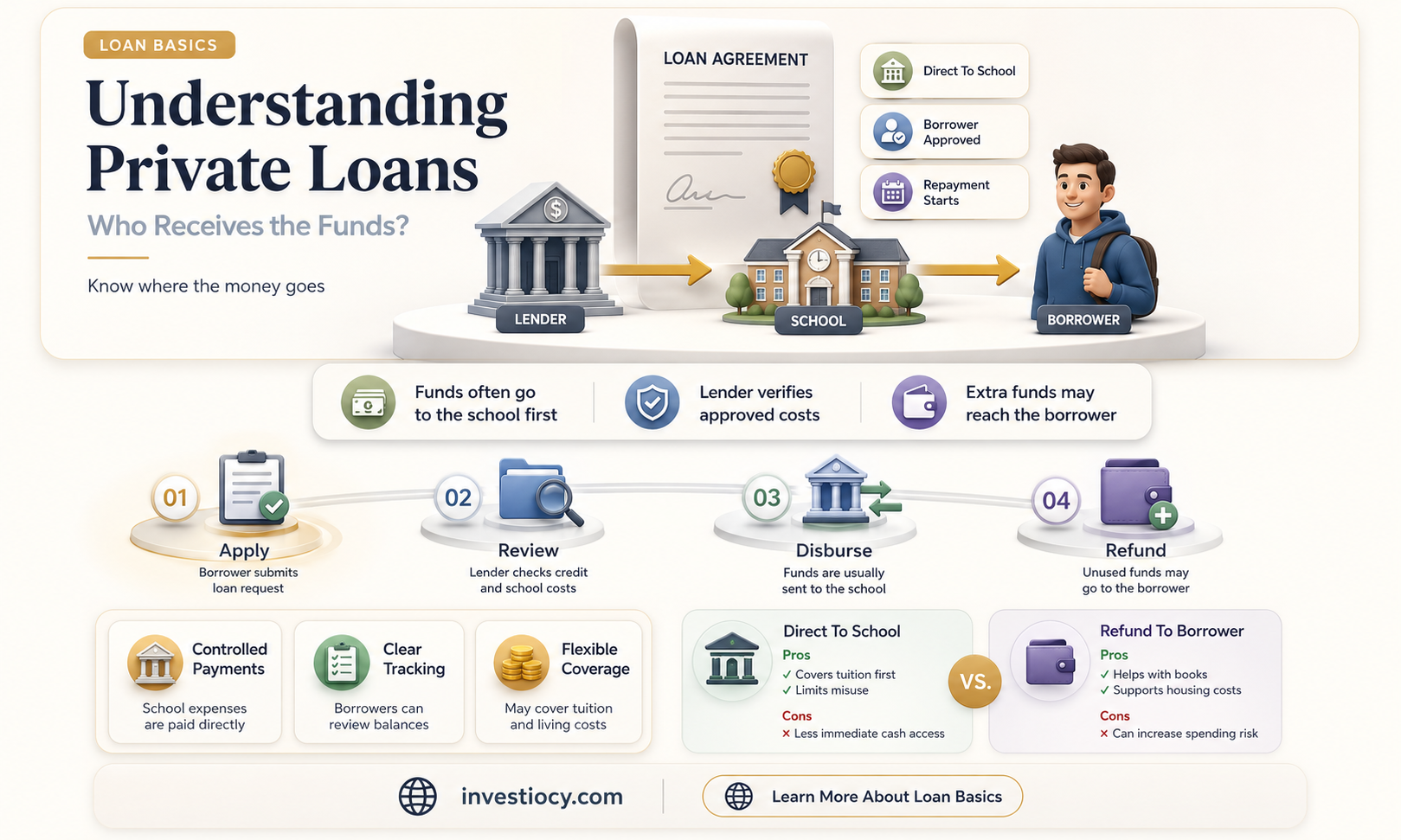

When considering a private loan, it's essential to understand how the funds are disbursed. Typically, the loan amount is not given directly to the borrower in cash. Instead, the lender transfers the funds to the borrower's bank account, which can then be used for the intended purpose, such as paying for tuition, books, or other educational expenses. This process ensures that the money is used for its intended purpose and provides a clear record of the transaction for both the lender and the borrower.

Explore related products

$8.99 $19.95

What You'll Learn

- Loan Disbursement: How private loan funds are transferred to the borrower

- Repayment Terms: Conditions and schedule for repaying the private loan

- Interest Rates: The cost of borrowing expressed as a percentage

- Collateral Requirements: Assets pledged to secure the private loan

- Credit Checks: Evaluation of the borrower's creditworthiness before loan approval

![]()

Loan Disbursement: How private loan funds are transferred to the borrower

The process of loan disbursement involves the actual transfer of funds from the lender to the borrower. In the case of private loans, this process can vary depending on the lender's policies and the specific terms of the loan agreement. Generally, the disbursement of private loan funds follows a series of steps that ensure the borrower receives the money in a timely and secure manner.

First, the lender will typically require the borrower to complete and submit a loan application, which includes providing personal and financial information. Once the application is approved, the lender will send the borrower a loan agreement outlining the terms of the loan, including the interest rate, repayment schedule, and any fees associated with the loan. The borrower must review and sign the loan agreement before the funds can be disbursed.

After the loan agreement is signed, the lender will initiate the transfer of funds. This can be done through various methods, such as a direct deposit into the borrower's bank account, a check mailed to the borrower, or a wire transfer. The time it takes for the funds to be transferred can vary depending on the lender and the method of transfer chosen.

In some cases, the lender may require additional documentation or verification before disbursing the funds. This could include proof of income, employment verification, or collateral documentation if the loan is secured. The borrower should be prepared to provide any necessary documentation promptly to avoid delays in the disbursement process.

Once the funds are transferred, the borrower should carefully review the loan disbursement statement to ensure that the amount received matches the loan amount agreed upon and that there are no discrepancies or errors. If there are any issues, the borrower should contact the lender immediately to resolve the problem.

In conclusion, the disbursement of private loan funds is a critical step in the loan process, and it is essential for borrowers to understand the steps involved and any potential requirements or delays. By being prepared and proactive, borrowers can ensure a smooth and efficient disbursement process.

Exploring EIDL Loans in the Latest Stimulus Package: What You Need to Know

You may want to see also

Explore related products

![]()

Repayment Terms: Conditions and schedule for repaying the private loan

The repayment terms of a private loan are critical to understanding the full scope of your financial commitment. These terms outline not only the schedule for repaying the principal amount but also any interest accrued, fees, and penalties for late payments. It's essential to review these conditions carefully to ensure you can meet the lender's requirements and avoid any potential financial pitfalls.

One key aspect of repayment terms is the amortization schedule, which details how each payment is applied to the principal and interest over the life of the loan. This schedule will show you how much of each payment goes towards reducing the principal balance and how much covers the interest. Understanding this breakdown can help you make informed decisions about your repayment strategy, such as whether to make extra payments to reduce the principal more quickly or to stick to the minimum payment schedule.

Another important factor to consider is the interest rate and how it is calculated. Private loans may have fixed or variable interest rates, and the method of calculation can vary. For example, some loans may use a simple interest formula, while others might use compound interest. Knowing how your interest is calculated can help you anticipate the total cost of the loan over its term and plan your repayment accordingly.

Additionally, repayment terms may include stipulations about prepayment penalties, late fees, and grace periods. Prepayment penalties can apply if you pay off the loan early, potentially saving you money on interest but costing you a fee. Late fees can add up quickly if you miss payments, so it's crucial to understand the lender's policy on late payments. Grace periods, on the other hand, may offer a temporary reprieve from payments, which can be helpful in times of financial hardship.

To ensure you're comfortable with the repayment terms, it's advisable to ask the lender about any aspects you don't understand. This could include requesting a detailed breakdown of the amortization schedule, clarification on how interest is calculated, or information about any potential fees and penalties. By doing so, you can make an informed decision about whether the loan is right for you and develop a repayment plan that aligns with your financial goals.

Unraveling the Mystery: Missing Documents and Their Impact on Nelnet Loans

You may want to see also

Explore related products

![]()

Interest Rates: The cost of borrowing expressed as a percentage

Interest rates are a critical component of any loan agreement, representing the cost of borrowing money expressed as a percentage of the principal amount. In the context of private loans, understanding interest rates is essential for both lenders and borrowers to ensure a fair and mutually beneficial transaction.

One unique aspect of private loans is that interest rates can be highly variable, often depending on the creditworthiness of the borrower, the collateral provided (if any), and the specific terms negotiated between the parties involved. Unlike commercial loans, which may have standardized interest rates based on market benchmarks, private loans allow for more flexibility and customization.

For borrowers, it's important to carefully consider the interest rate being offered, as it will directly impact the total cost of the loan over its lifetime. A higher interest rate may result in significantly increased payments, potentially making the loan unaffordable or leading to financial strain. Borrowers should also be aware of any potential penalties or fees associated with early repayment, as these can further affect the overall cost of the loan.

Lenders, on the other hand, must balance the need to earn a return on their investment with the risk of lending to a private individual. Interest rates serve as a mechanism to compensate lenders for the risk they assume, as well as to encourage timely repayment. In some cases, lenders may opt for variable interest rates that fluctuate based on market conditions, providing a degree of protection against inflation or changes in the economic environment.

When evaluating a private loan, both parties should carefully review the interest rate terms and consider seeking professional advice if necessary. By understanding the implications of interest rates and negotiating fair terms, borrowers and lenders can work together to create a loan agreement that meets their respective needs and objectives.

Understanding Paycheck Protection Loans: Repayment Requirements Explained

You may want to see also

Explore related products

![]()

Collateral Requirements: Assets pledged to secure the private loan

In the realm of private lending, collateral plays a pivotal role in securing the loan. Assets pledged as collateral serve as a safety net for the lender, ensuring that they have a means of recovering the loaned amount if the borrower defaults. This practice is common in both personal and business loans, where the borrower's creditworthiness alone may not be sufficient to guarantee repayment.

The types of assets that can be used as collateral vary widely. Real estate, such as homes or commercial properties, is a common form of collateral due to its tangible value and the relative ease with which it can be appraised and liquidated if necessary. Vehicles, particularly those that are fully owned or have significant equity, can also be used. Other assets might include investments, such as stocks or bonds, business equipment, or even personal items of high value like jewelry or art collections.

The value of the collateral is typically assessed by the lender to determine the loan-to-value (LTV) ratio. This ratio is a critical factor in the loan approval process, as it helps the lender gauge the risk associated with the loan. A lower LTV ratio generally indicates a lower risk, as the collateral's value exceeds the loan amount. Conversely, a higher LTV ratio suggests greater risk, as the collateral's value is closer to or less than the loan amount.

It's important for borrowers to understand that pledging collateral can have significant implications. If they fail to repay the loan as agreed, the lender may have the right to seize and sell the collateral to recoup the outstanding debt. This can lead to the loss of valuable assets, which may have sentimental or practical importance to the borrower. Additionally, the borrower's credit score may be negatively impacted, making it more difficult to secure future loans.

In conclusion, collateral requirements are a fundamental aspect of private loans, providing lenders with a measure of security against the risk of default. Borrowers should carefully consider the implications of pledging assets as collateral and ensure they fully understand the terms and conditions of the loan agreement before proceeding.

Exploring Military Benefits: College Loan Forgiveness Options

You may want to see also

Explore related products

![]()

Credit Checks: Evaluation of the borrower's creditworthiness before loan approval

Lenders conduct credit checks to assess a borrower's creditworthiness before approving a loan. This process involves reviewing the borrower's credit history, including their payment patterns, debt levels, and any negative marks such as bankruptcies or foreclosures. The lender uses this information to determine the borrower's likelihood of repaying the loan on time and in full. A good credit score can increase the chances of loan approval and may result in more favorable interest rates and terms.

Credit checks are typically performed by credit reporting agencies, which compile and maintain credit reports for individuals. These agencies collect data from various sources, including banks, credit card companies, and other lenders. The credit report provides a comprehensive overview of the borrower's credit history, allowing the lender to make an informed decision about the loan application.

The credit check process is an essential step in the loan approval process, as it helps lenders mitigate the risk of lending to borrowers who may not be able to repay the loan. By evaluating the borrower's creditworthiness, lenders can ensure that they are making responsible lending decisions and minimizing the potential for financial losses.

In some cases, lenders may also consider alternative credit data, such as rent payments or utility bills, to supplement the information provided in the credit report. This can be particularly helpful for borrowers who have limited credit history or who have experienced credit challenges in the past.

Overall, credit checks play a critical role in the loan approval process, allowing lenders to assess the borrower's creditworthiness and make informed decisions about lending. By understanding the credit check process and maintaining a good credit score, borrowers can increase their chances of securing a loan with favorable terms and conditions.

Understanding Payroll Protection Loans: Repayment Requirements Explained

You may want to see also

Frequently asked questions

The private loan is typically disbursed directly to you, the borrower, rather than being shared with others.

Eligibility for a private loan depends on factors such as your credit score, income, and debt-to-income ratio. Lenders will review your application to determine if you meet their criteria.

Private loans can be used for a variety of purposes, including personal expenses, home improvements, or debt consolidation. The specific use may vary depending on the lender's policies.

To apply for a private loan, you'll need to fill out an application form with the lender, providing details about your income, employment, and credit history. You may also need to provide collateral or a co-signer, depending on the lender's requirements.

Repayment terms for a private loan vary depending on the lender and the specific loan agreement. Typically, you'll need to make regular payments over a fixed period, with interest accruing on the outstanding balance.