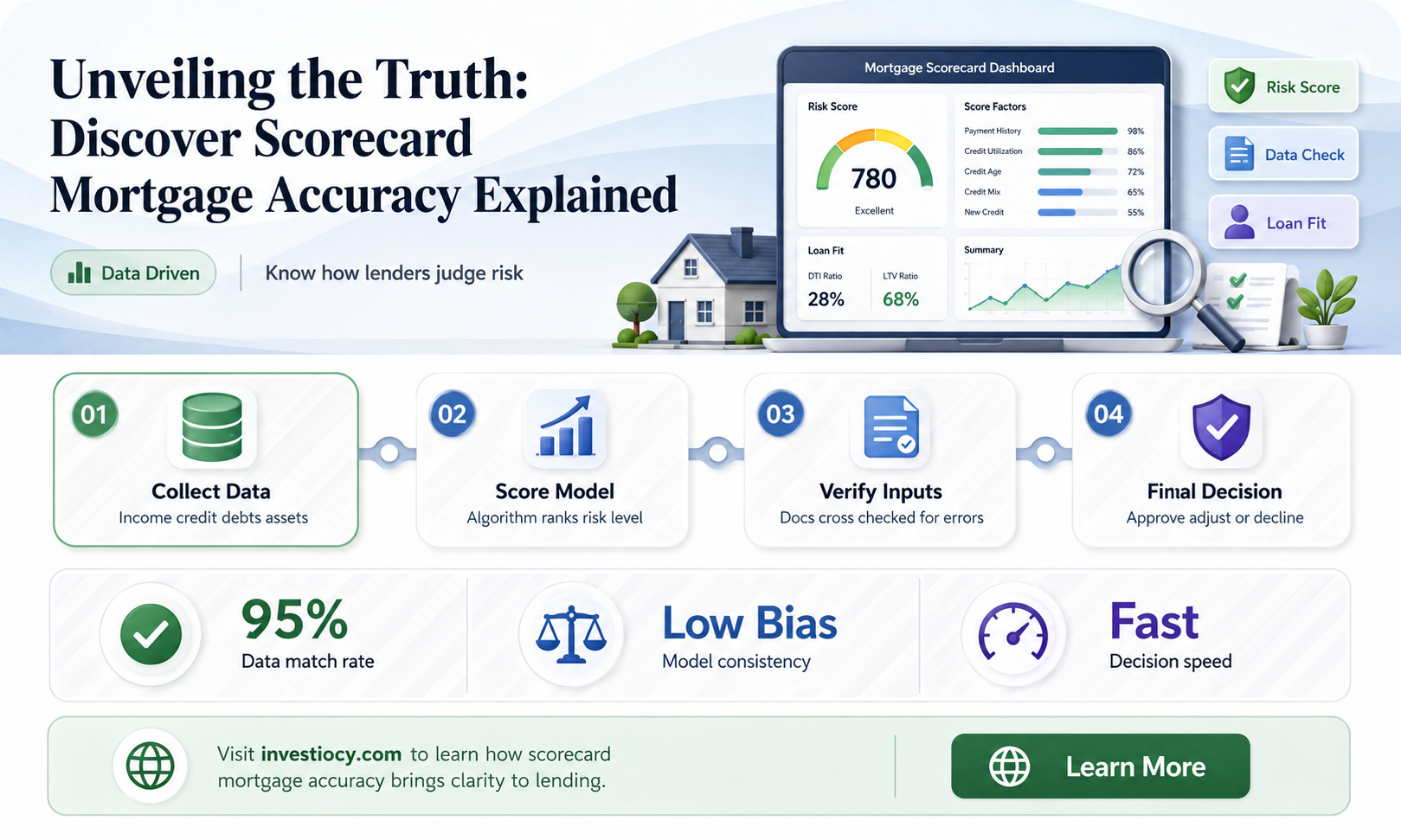

The Discover Scorecard Mortgage is a financial tool designed to help potential homebuyers assess their readiness for purchasing a home. It takes into account various factors such as credit score, income, debt, and savings to provide a comprehensive evaluation. But how accurate is this tool in predicting mortgage eligibility and affordability? This question is crucial for individuals relying on the Discover Scorecard to make informed decisions about their homeownership journey.

Explore related products

What You'll Learn

- Understanding Discover Scorecard: Overview of the mortgage scoring model used by Discover Financial Services

- Factors Influencing Accuracy: Examination of key variables that affect the precision of mortgage predictions

- Data Quality and Sources: Assessment of the reliability and origin of data used in the mortgage scorecard

- Model Validation Techniques: Methods employed to verify the accuracy and robustness of the mortgage scoring model

- Real-World Application and Outcomes: Practical implications and results of using the Discover Scorecard in mortgage lending decisions

![]()

Understanding Discover Scorecard: Overview of the mortgage scoring model used by Discover Financial Services

Discover Scorecard is a proprietary mortgage scoring model developed by Discover Financial Services to assess the creditworthiness of potential borrowers. Unlike traditional credit scores, which primarily focus on payment history and debt levels, Discover Scorecard incorporates a broader range of factors to evaluate an individual's ability to repay a mortgage. This includes analyzing income stability, employment history, and other financial obligations, providing a more comprehensive view of the borrower's financial health.

One of the key advantages of Discover Scorecard is its ability to consider non-traditional credit data, such as rent payments and utility bills, which can be particularly beneficial for individuals with limited credit history. By leveraging alternative data sources, Discover Scorecard aims to provide a more accurate and nuanced assessment of a borrower's creditworthiness, potentially expanding access to mortgage financing for underserved populations.

The model also employs advanced machine learning algorithms to continuously refine its predictive capabilities, adapting to changes in the economic environment and borrower behavior. This ensures that Discover Scorecard remains a reliable and effective tool for mortgage lenders, helping them make informed decisions about loan approvals and interest rates.

However, it's important to note that while Discover Scorecard offers several benefits, it is not without its limitations. Critics argue that the model's reliance on alternative data sources may introduce biases, particularly if these sources are not representative of the broader population. Additionally, the complexity of the model can make it challenging for borrowers to understand how their score is calculated, potentially leading to confusion and mistrust.

In conclusion, Discover Scorecard represents a significant innovation in mortgage scoring, offering a more holistic approach to evaluating creditworthiness. While it has the potential to improve access to mortgage financing and reduce lending risks, it is crucial to address concerns about bias and transparency to ensure that the model is fair and effective for all borrowers.

Unveiling the Truth: How Accurate Are Mortgage Surveys?

You may want to see also

Explore related products

![]()

Factors Influencing Accuracy: Examination of key variables that affect the precision of mortgage predictions

Several factors can significantly influence the accuracy of mortgage predictions, particularly when using a scorecard approach like the one employed by Discover. One key variable is the quality and comprehensiveness of the data used to train the model. Accurate predictions rely on a robust dataset that includes a wide range of relevant variables, such as credit scores, income levels, debt-to-income ratios, and loan-to-value ratios. If the training data is incomplete or contains errors, the resulting model may not be able to make precise predictions.

Another important factor is the choice of variables included in the scorecard. Not all variables have the same impact on mortgage outcomes, and selecting the most relevant ones is crucial for accuracy. For instance, while credit score is a significant predictor of mortgage default, other factors like employment history and asset reserves can also play important roles. A well-designed scorecard should incorporate a mix of these variables to capture the full spectrum of risk factors.

The weighting of variables within the scorecard is also critical. Each variable should be assigned a weight that reflects its relative importance in predicting mortgage outcomes. If the weights are not calibrated correctly, the model may overemphasize certain factors while underestimating others, leading to inaccurate predictions. Regular review and adjustment of these weights are necessary to ensure that the scorecard remains effective over time.

Additionally, the accuracy of mortgage predictions can be affected by external factors such as economic conditions and changes in lending regulations. A model trained during a period of economic stability may not perform as well during a recession or when new regulations are introduced. To mitigate this risk, it's essential to regularly update the model with new data and to incorporate macroeconomic indicators that can help capture the impact of broader economic trends.

Finally, the implementation and use of the scorecard within the lending process can also influence its accuracy. If lenders do not use the scorecard consistently or if they override its recommendations without proper justification, the effectiveness of the model can be compromised. Ensuring that the scorecard is integrated seamlessly into the lending workflow and that its outputs are respected can help maintain its predictive power.

In conclusion, the accuracy of mortgage predictions using a scorecard approach like Discover's depends on a variety of factors, including data quality, variable selection, weighting, external economic conditions, and implementation practices. By carefully managing these factors, lenders can improve the precision of their mortgage predictions and make more informed lending decisions.

Decoding Mortgage Estimates: How Accurate Are They Really?

You may want to see also

Explore related products

![]()

Data Quality and Sources: Assessment of the reliability and origin of data used in the mortgage scorecard

The reliability of a mortgage scorecard hinges significantly on the quality and origin of the data used to construct it. Assessing data quality involves examining several key aspects: accuracy, completeness, consistency, and timeliness. Data sources can range from internal databases to external credit bureaus and financial institutions. Each source must be evaluated for its credibility and the relevance of the data it provides to the mortgage scoring process.

One critical aspect of data quality assessment is verifying the accuracy of the data. This involves cross-checking information against multiple sources to ensure that it is correct and up-to-date. For instance, credit scores, employment history, and financial records should be validated to prevent errors that could lead to inaccurate mortgage scoring. Completeness is another vital factor, as missing data can skew the results of the scorecard. Lenders must ensure that all necessary data fields are populated and that the information is comprehensive enough to make informed decisions.

Consistency in data is also crucial. The same data point should yield the same result regardless of when or how it is accessed. This requires robust data management systems and processes to maintain data integrity. Timeliness is particularly important in the mortgage industry, where market conditions and borrower circumstances can change rapidly. Using outdated data can lead to poor decision-making and increased risk.

When evaluating data sources, lenders should consider the reputation and reliability of the provider. Established credit bureaus and financial institutions typically have rigorous data collection and verification processes, making them more trustworthy sources. However, even reputable sources can have biases or limitations, so it is essential to understand the methodology behind the data collection and scoring.

In addition to assessing the quality of the data, lenders should also consider the diversity of the data sources. Relying on a single source can lead to a narrow perspective and potential biases. By incorporating data from multiple sources, lenders can gain a more comprehensive understanding of a borrower's financial situation and make more accurate predictions about their creditworthiness.

Ultimately, the accuracy of a mortgage scorecard is directly linked to the quality and reliability of the data used to create it. By conducting thorough data quality assessments and diversifying their data sources, lenders can improve the accuracy of their mortgage scoring models and make better-informed lending decisions.

Decoding Trulia's Mortgage Estimates: How Accurate Are They Really?

You may want to see also

Explore related products

![]()

Model Validation Techniques: Methods employed to verify the accuracy and robustness of the mortgage scoring model

To validate the accuracy and robustness of the mortgage scoring model, several techniques are employed. One primary method is the use of holdout samples. This involves setting aside a portion of the dataset during the model development phase and using it to test the model's predictions against actual outcomes. By comparing the predicted scores with the true default rates, the model's accuracy can be assessed.

Another technique is cross-validation, where the dataset is divided into multiple segments, and the model is trained and tested on each segment iteratively. This helps to ensure that the model is not overfitting to any particular subset of the data and provides a more comprehensive evaluation of its performance.

Additionally, stress testing is conducted to assess the model's robustness under extreme conditions. This involves simulating scenarios with significantly higher or lower default rates than those observed in the historical data. By analyzing how the model performs under these stressed conditions, potential vulnerabilities can be identified and addressed.

Furthermore, the model is regularly updated and re-validated to account for changes in the economic environment and borrower behavior. This ongoing validation process helps to maintain the model's accuracy and relevance over time.

In summary, the mortgage scoring model is subjected to rigorous validation techniques, including holdout samples, cross-validation, stress testing, and regular updates, to ensure its accuracy and robustness in predicting mortgage default risk.

Explore related products

![]()

Real-World Application and Outcomes: Practical implications and results of using the Discover Scorecard in mortgage lending decisions

The Discover Scorecard has been implemented by several mortgage lenders to streamline their underwriting processes and improve the accuracy of their lending decisions. One of the key benefits of using this scorecard is its ability to provide a more comprehensive assessment of a borrower's creditworthiness by considering a wider range of factors beyond just their credit score. This has led to a more nuanced understanding of each borrower's financial situation, allowing lenders to make more informed decisions about whether to approve a mortgage application.

In practice, the use of the Discover Scorecard has resulted in a significant reduction in the number of defaults and foreclosures among borrowers who were approved for mortgages. This is because the scorecard helps lenders to identify potential risks and red flags that might not be immediately apparent from a traditional credit report. For example, the scorecard takes into account factors such as the borrower's income stability, their level of debt, and their history of making on-time payments. By considering these additional factors, lenders are better able to assess the likelihood that a borrower will be able to repay their mortgage in full.

Furthermore, the Discover Scorecard has also helped lenders to improve their customer service and satisfaction rates. By providing a more personalized and detailed assessment of each borrower's financial situation, lenders are able to offer more tailored advice and guidance to their customers. This can help borrowers to better understand their financial options and make more informed decisions about their mortgage applications. Additionally, the use of the scorecard has enabled lenders to process mortgage applications more quickly and efficiently, which can be a significant advantage in a competitive market.

Overall, the real-world application of the Discover Scorecard in mortgage lending decisions has demonstrated its value as a powerful tool for improving the accuracy and efficiency of the underwriting process. By providing a more comprehensive and nuanced assessment of each borrower's creditworthiness, the scorecard has helped lenders to make better decisions, reduce their risk exposure, and improve their customer service. As a result, the Discover Scorecard has become an increasingly popular choice among mortgage lenders looking to enhance their underwriting capabilities and stay competitive in the market.

Frequently asked questions

The Discover Scorecard is a proprietary credit scoring model used by Discover Financial Services. While it's designed to provide a comprehensive assessment of an individual's creditworthiness, its accuracy for mortgage predictions can vary. Factors such as the inclusion of non-traditional credit data and the specific algorithms used can influence its predictive power. It's generally considered to be a reliable tool, but like any credit scoring model, it's not infallible and should be used in conjunction with other financial assessments.

Several factors can impact the accuracy of the Discover Scorecard in mortgage lending. These include the quality and completeness of the data used to generate the score, the relevance of the score to the specific mortgage product being applied for, and the economic conditions at the time of application. Additionally, individual circumstances such as a history of late payments, high debt levels, or a lack of credit history can also affect the score's accuracy in predicting mortgage default risk.

The Discover Scorecard is one of several credit scoring models used in mortgage lending. Compared to other models like FICO or VantageScore, the Discover Scorecard may place different weights on various credit factors or use unique algorithms to calculate the score. While there isn't a one-size-fits-all answer to which model is the most accurate, the Discover Scorecard is generally considered to be a competitive option in the market. Lenders may choose to use it based on their specific underwriting criteria and the types of borrowers they typically serve.

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)