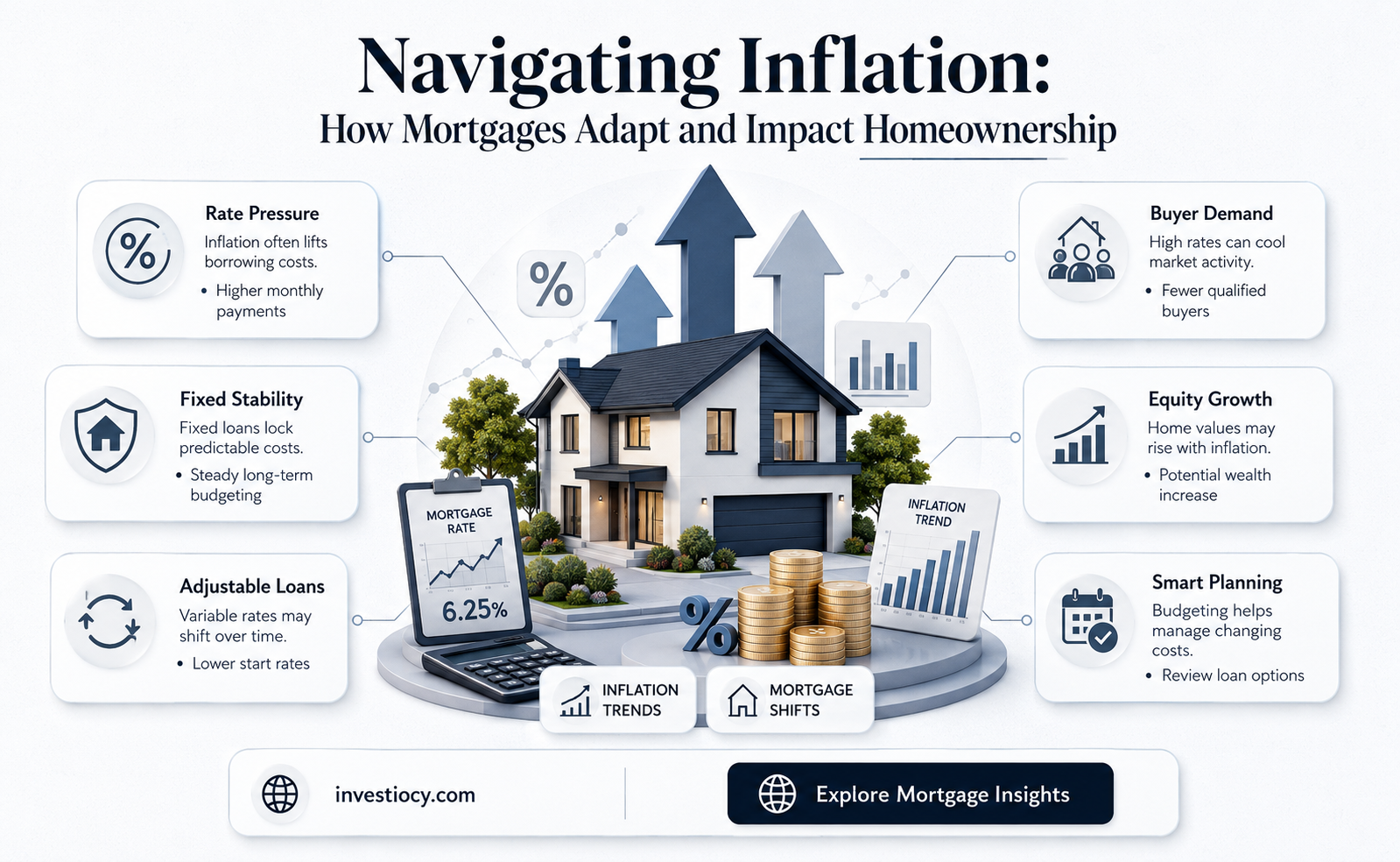

Mortgages and inflation are intricately linked, with changes in inflation rates having a direct impact on mortgage interest rates and the overall cost of borrowing. When inflation rises, central banks often respond by increasing interest rates to curb inflationary pressures. This, in turn, leads to higher mortgage rates, making borrowing more expensive for homebuyers and increasing the monthly payments for those with variable-rate mortgages. Conversely, during periods of low inflation or deflation, interest rates may be lowered to stimulate economic growth, resulting in more affordable mortgage options. Understanding this relationship is crucial for both current and prospective homeowners, as it can significantly influence their financial decisions and long-term economic stability.

| Characteristics | Values |

|---|---|

| Definition | A mortgage is a loan secured by real estate, typically used to purchase a home. Inflation is the rate at which the general level of prices for goods and services rises and subsequently erodes purchasing power. |

| Impact of Inflation on Mortgages | Inflation can affect mortgages in several ways, including increasing the cost of borrowing, reducing the purchasing power of the loan amount, and influencing interest rates. |

| Fixed-Rate Mortgages | With fixed-rate mortgages, the interest rate remains constant for the life of the loan. This means that inflation does not directly affect the monthly payment amount. However, if inflation rises, the purchasing power of the loan amount decreases. |

| Variable-Rate Mortgages | Variable-rate mortgages, also known as adjustable-rate mortgages (ARMs), have interest rates that fluctuate with market conditions. If inflation increases, interest rates may also rise, leading to higher monthly payments. |

| Effect on Loan Amount | As inflation increases, the value of money decreases. This means that the loan amount you receive today will have less purchasing power in the future. For example, a $300,000 loan today may only be worth $250,000 in 10 years if inflation averages 3% per year. |

| Impact on Monthly Payments | For fixed-rate mortgages, monthly payments remain the same regardless of inflation. However, for variable-rate mortgages, monthly payments can increase if interest rates rise due to inflation. |

| Inflation-Indexed Mortgages | Some mortgages, known as inflation-indexed mortgages, have payments and interest rates that adjust based on inflation. This can help protect borrowers from the effects of rising inflation. |

| Historical Context | Historically, periods of high inflation have led to increased interest rates, which can make borrowing more expensive. For example, in the 1980s, high inflation rates led to double-digit interest rates on mortgages. |

| Current Trends | As of the latest data available, inflation rates have been relatively low, which has kept mortgage interest rates at historic lows. However, there are concerns that rising inflation could lead to higher interest rates in the future. |

| Borrower Strategies | Borrowers can protect themselves from the effects of inflation by choosing a fixed-rate mortgage, considering an inflation-indexed mortgage, or making extra payments to pay off the loan faster. |

| Lender Considerations | Lenders must also consider the effects of inflation when setting interest rates and loan terms. They may adjust rates and terms to account for expected inflation rates. |

| Economic Indicators | Key economic indicators that can influence mortgage rates and inflation include the Consumer Price Index (CPI), the Federal Reserve’s inflation target, and the yield on Treasury bonds. |

| Government Policies | Government policies, such as monetary policy set by the Federal Reserve, can also impact inflation and mortgage rates. For example, the Fed may raise interest rates to combat inflation. |

| Global Factors | Global factors, such as changes in oil prices, trade policies, and economic conditions in other countries, can also influence inflation and mortgage rates. |

| Future Projections | Economists and financial experts often make projections about future inflation rates and how they will impact mortgage rates. These projections can help borrowers and lenders make informed decisions. |

Explore related products

What You'll Learn

- Impact of inflation on mortgage rates: Inflation can lead to higher mortgage rates as lenders seek to maintain purchasing power

- Adjustable-rate mortgages (ARMs) and inflation: ARMs may adjust more frequently or by larger amounts in response to inflation, affecting borrowers' payments

- Fixed-rate mortgages and inflation risk: Fixed-rate mortgages may become less attractive during high inflation periods as their real value decreases

- Inflation and mortgage affordability: Rising inflation can reduce borrowers' purchasing power, making it harder to afford a mortgage

- Government policies and mortgage inflation protection: Some governments may implement policies to protect borrowers from the effects of inflation on mortgages

![]()

Impact of inflation on mortgage rates: Inflation can lead to higher mortgage rates as lenders seek to maintain purchasing power

Inflation can have a significant impact on mortgage rates, as lenders seek to maintain their purchasing power in a rising cost environment. When inflation increases, the value of money decreases, which can lead to higher interest rates as lenders try to keep up with the rising cost of goods and services. This, in turn, can make borrowing more expensive for homebuyers, potentially pricing some out of the market or forcing them to take on more debt.

One way to understand the relationship between inflation and mortgage rates is to look at the historical data. Over the past several decades, there has been a strong correlation between inflation and mortgage rates. When inflation has been high, mortgage rates have also tended to be high, and vice versa. This is because lenders need to charge higher interest rates to compensate for the loss of purchasing power that comes with inflation.

Another factor to consider is the role of the central bank in managing inflation and mortgage rates. Central banks, such as the Federal Reserve in the United States, have the ability to influence interest rates through monetary policy. When inflation is high, central banks may raise interest rates to try to slow down economic growth and reduce inflationary pressures. This can lead to higher mortgage rates, as lenders pass on the increased cost of borrowing to homebuyers.

It's also important to consider the impact of inflation on the housing market more broadly. When inflation is high, the cost of building and maintaining homes increases, which can lead to higher home prices. This, in turn, can make it more difficult for people to afford homes, potentially leading to a decrease in demand and a slowdown in the housing market.

Finally, it's worth noting that there are some strategies that homebuyers can use to mitigate the impact of inflation on mortgage rates. For example, some borrowers may choose to take out adjustable-rate mortgages, which can offer lower initial interest rates than fixed-rate mortgages. However, these mortgages also carry the risk of rate increases in the future, so borrowers need to carefully consider their options and financial situation before making a decision.

Decoding Primary Residence: How Mortgages Influence Your Main Home

You may want to see also

Explore related products

![]()

Adjustable-rate mortgages (ARMs) and inflation: ARMs may adjust more frequently or by larger amounts in response to inflation, affecting borrowers' payments

Adjustable-rate mortgages (ARMs) are a type of home loan where the interest rate can change over time, typically in response to broader economic conditions such as inflation. Unlike fixed-rate mortgages, where the interest rate remains constant for the life of the loan, ARMs can adjust more frequently or by larger amounts, which can significantly impact borrowers' payments.

The frequency and magnitude of these adjustments depend on the specific terms of the ARM, which are outlined in the loan agreement. Some ARMs may adjust annually, while others might do so more or less frequently. The adjustment amount is usually tied to a specific economic index, such as the Consumer Price Index (CPI) or the London Interbank Offered Rate (LIBOR). When inflation rises, the interest rate on an ARM may increase, leading to higher monthly payments for the borrower.

For example, consider a borrower with a 5/1 ARM, which means the interest rate is fixed for the first five years and then adjusts annually thereafter. If the initial interest rate is 3% and the loan amount is $300,000, the borrower's monthly payment would be approximately $1,299 for the first five years. However, if the interest rate adjusts upward by 1% in the sixth year due to inflation, the monthly payment would increase to around $1,433. This increase can be a significant financial burden for borrowers who are not prepared for the change.

To mitigate the risks associated with ARMs, borrowers should carefully review the terms of the loan agreement and consider factors such as the potential for future interest rate increases, their ability to afford higher payments, and the length of time they plan to stay in the home. Additionally, borrowers may want to consider refinancing options or converting to a fixed-rate mortgage if they are concerned about the impact of inflation on their ARM payments.

In summary, adjustable-rate mortgages can be a viable option for some borrowers, but they come with the risk of increasing payments in response to inflation. It is essential for borrowers to understand the terms of their ARM and to plan accordingly to ensure they can manage potential payment increases.

From Main Street to Wall Street: The Mortgage Journey Explained

You may want to see also

Explore related products

![]()

Fixed-rate mortgages and inflation risk: Fixed-rate mortgages may become less attractive during high inflation periods as their real value decreases

During periods of high inflation, fixed-rate mortgages can become less attractive to borrowers. This is because the real value of the mortgage payments decreases over time, making it more difficult for lenders to recoup their costs. As a result, lenders may increase the interest rates on fixed-rate mortgages to compensate for the expected inflation, making them less competitive compared to other types of mortgages.

One unique angle to consider is the impact of inflation on the amortization schedule of a fixed-rate mortgage. As inflation rises, the purchasing power of each mortgage payment decreases, meaning that a larger portion of the payment goes towards interest rather than principal. This can lead to a situation where the borrower is paying more in interest over the life of the loan, even though the nominal interest rate remains the same.

To mitigate this risk, some borrowers may opt for an adjustable-rate mortgage (ARM), which allows the interest rate to fluctuate with inflation. However, ARMs can also be risky, as they may result in higher payments if inflation rises significantly. Another option is to consider a hybrid mortgage, which combines the stability of a fixed-rate mortgage with the flexibility of an ARM.

In addition to the impact on borrowers, inflation can also affect the profitability of mortgage lenders. As the real value of mortgage payments decreases, lenders may need to increase their interest rates to maintain their profit margins. This can lead to a decrease in demand for mortgages, as borrowers may be deterred by the higher rates.

Overall, the relationship between fixed-rate mortgages and inflation risk is complex and multifaceted. Borrowers and lenders alike need to carefully consider the potential impacts of inflation on their mortgage decisions, and may need to adjust their strategies accordingly to mitigate risk and maximize financial stability.

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)

![]()

Inflation and mortgage affordability: Rising inflation can reduce borrowers' purchasing power, making it harder to afford a mortgage

Rising inflation can significantly impact mortgage affordability, making it more challenging for borrowers to secure a home loan. As inflation increases, the purchasing power of borrowers decreases, meaning they can afford less with the same amount of money. This reduction in purchasing power can lead to a decrease in the number of homes that borrowers can afford, as well as an increase in the amount of money they need to save for a down payment.

One of the primary ways that inflation affects mortgage affordability is through its impact on interest rates. As inflation rises, lenders may increase interest rates to keep pace with the rising cost of living. This increase in interest rates can lead to higher monthly mortgage payments, making it more difficult for borrowers to afford a home loan. Additionally, higher interest rates can also lead to a decrease in the amount of money that borrowers can borrow, further reducing their purchasing power.

Another way that inflation can impact mortgage affordability is through its effect on home prices. As inflation increases, the cost of building and maintaining a home also increases, which can lead to higher home prices. This increase in home prices can make it more difficult for borrowers to afford a home, as they need to save more money for a down payment and may need to take out a larger loan.

To mitigate the impact of inflation on mortgage affordability, borrowers can take several steps. One option is to lock in a fixed-rate mortgage, which can provide stability and predictability in terms of monthly payments. Another option is to consider an adjustable-rate mortgage, which may offer lower interest rates in the short term, but may also increase over time as inflation rises. Borrowers can also focus on improving their credit score, which can help them qualify for lower interest rates and better loan terms.

In conclusion, rising inflation can have a significant impact on mortgage affordability, making it more challenging for borrowers to secure a home loan. By understanding the ways that inflation affects mortgage affordability and taking steps to mitigate its impact, borrowers can increase their chances of successfully securing a home loan.

Explore related products

![]()

Government policies and mortgage inflation protection: Some governments may implement policies to protect borrowers from the effects of inflation on mortgages

Governments may implement various policies to shield borrowers from the impact of inflation on mortgages. One such policy is the introduction of inflation-indexed mortgages, where the principal and interest payments are adjusted in line with inflation rates. This ensures that the real value of the debt remains constant over time, protecting borrowers from the erosion of their purchasing power.

Another approach is to offer subsidies or tax incentives to borrowers who take out mortgages with variable interest rates. This can help offset the increased costs associated with rising inflation and make it more affordable for people to own homes. Governments may also impose regulations on lenders to ensure that they offer fair and transparent mortgage terms, preventing them from taking advantage of borrowers during periods of high inflation.

In some cases, governments may choose to intervene directly in the housing market by purchasing or guaranteeing mortgages. This can help stabilize the market and prevent a surge in foreclosures, which can have a negative impact on the economy as a whole. Additionally, governments may work to increase the supply of affordable housing, which can help reduce the demand for mortgages and alleviate some of the pressure caused by inflation.

It is important to note that the effectiveness of these policies can vary depending on the specific economic conditions and the design of the policies themselves. For example, inflation-indexed mortgages may not be as effective in a deflationary environment, and subsidies may not be sustainable in the long term if they are not properly funded. Therefore, it is crucial for governments to carefully consider the potential consequences of their policies and to monitor their impact on the housing market and the broader economy.

Frequently asked questions

Mortgage rates often increase in response to inflation. This is because lenders need to ensure that the interest they charge keeps pace with the rising cost of living, thereby maintaining the purchasing power of the loan repayments.

Adjustable-rate mortgages (ARMs) are directly impacted by inflation. As inflation rises, the interest rate on an ARM may increase, leading to higher monthly payments for the borrower. This is because ARMs are tied to a specific index, such as the Consumer Price Index (CPI), which adjusts the interest rate periodically based on inflation.

Inflation does not directly affect the principal amount of a mortgage. However, it can influence the value of the property securing the mortgage. In a high-inflation environment, property values may rise, potentially increasing the equity in the home. Conversely, during deflation, property values may decrease, reducing the equity and possibly leading to underwater mortgages.