When homeowners refinance their mortgage, they often aim to tap into their home's equity or secure a lower interest rate. Cashing out on a refinance mortgage involves borrowing more than the outstanding balance of the original mortgage and receiving the difference in cash. This strategy can provide funds for various purposes, such as home improvements, debt consolidation, or major expenses. However, it's essential to understand the implications, including potential changes in monthly payments, interest rates, and the overall financial impact. Homeowners should carefully evaluate their financial goals and consult with a mortgage professional to determine if a cash-out refinance is the right choice for their situation.

| Characteristics | Values |

|---|---|

| Definition | A refinance mortgage is a new mortgage taken out to pay off an existing mortgage, often to secure a lower interest rate or to access equity in the property. |

| Purpose | People refinance mortgages to reduce monthly payments, shorten the loan term, switch from an adjustable-rate to a fixed-rate mortgage, or to take out cash against the equity in their home. |

| Process | The process involves applying for a new mortgage, providing financial documentation, undergoing a credit check, and closing the loan. The new lender pays off the old mortgage, and the borrower begins making payments on the new loan. |

| Eligibility | Eligibility for refinancing depends on factors such as credit score, loan-to-value ratio, debt-to-income ratio, and the amount of equity in the property. |

| Types | Common types of refinance mortgages include rate-and-term refinances, cash-out refinances, and streamline refinances. |

| Benefits | Benefits of refinancing include lower interest rates, reduced monthly payments, the ability to take out cash, and the potential to pay off the mortgage faster. |

| Drawbacks | Drawbacks may include closing costs, potential prepayment penalties, and the risk of extending the loan term, which could result in paying more interest over time. |

| Market Trends | Refinance rates often fluctuate based on economic conditions, interest rate movements, and housing market trends. |

| Impact on Credit Score | Applying for a refinance mortgage may result in a temporary dip in credit score due to the hard credit inquiry, but consistent payments can help rebuild and improve credit over time. |

| Tax Implications | In some cases, the interest paid on a refinance mortgage may be tax-deductible, but it's essential to consult with a tax professional to understand the specific implications. |

| Popular Lenders | Some popular lenders for refinance mortgages include banks, credit unions, and online mortgage companies. |

| Alternatives | Alternatives to refinancing include home equity loans, home equity lines of credit (HELOCs), and reverse mortgages. |

| Common Mistakes | Common mistakes when refinancing include not shopping around for the best rate, not considering the long-term impact of extending the loan term, and overlooking closing costs. |

| Tips for Success | Tips for a successful refinance include improving credit score before applying, comparing rates from multiple lenders, and carefully considering the loan terms and conditions. |

Explore related products

What You'll Learn

- Understanding Refinance Cash-Out: Basics of cash-out refinancing, how it differs from rate-and-term refinancing

- Eligibility Criteria: Requirements for homeowners to qualify, including credit score, equity, and income verification

- Calculation of Cash-Out Amount: Determining how much cash can be taken out based on home value and existing mortgage

- Closing Costs and Fees: Overview of costs associated with refinancing, such as appraisal fees, title insurance, and origination fees

- Impact on Monthly Payments: How cash-out refinancing affects monthly mortgage payments, including potential increases due to higher loan amounts

![]()

Understanding Refinance Cash-Out: Basics of cash-out refinancing, how it differs from rate-and-term refinancing

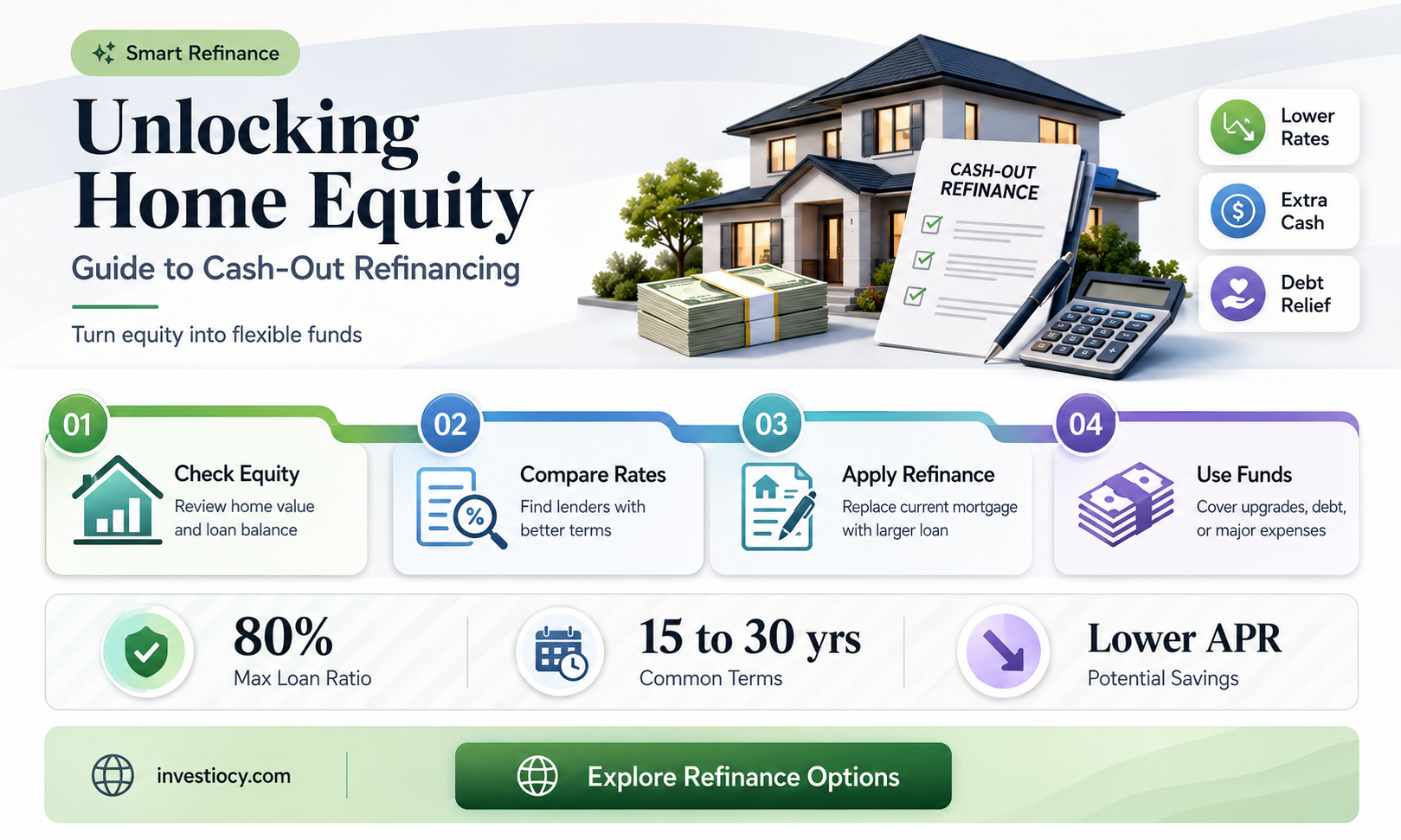

Cash-out refinancing is a powerful financial tool that allows homeowners to tap into their home's equity by refinancing their existing mortgage for a higher amount than they currently owe. This type of refinancing provides borrowers with a lump sum of cash at closing, which can be used for a variety of purposes, such as home improvements, debt consolidation, or investment opportunities. In contrast, rate-and-term refinancing focuses solely on adjusting the interest rate and/or the loan term without providing any cash back to the borrower.

One of the key differences between cash-out and rate-and-term refinancing lies in the loan-to-value (LTV) ratio. Cash-out refinancing typically allows for a higher LTV ratio, meaning borrowers can access a larger portion of their home's equity. However, this also means that cash-out refinancing may come with stricter underwriting requirements and potentially higher interest rates compared to rate-and-term refinancing.

When considering cash-out refinancing, it's essential for borrowers to understand the potential risks and rewards. On the one hand, cash-out refinancing can provide a significant amount of cash that can be used to improve one's financial situation. On the other hand, it can also increase the borrower's monthly mortgage payment and potentially put their home at risk if they're unable to make the new, higher payments.

To successfully navigate the cash-out refinancing process, borrowers should carefully evaluate their financial goals and needs, as well as their ability to repay the new loan. It's also crucial to shop around for the best interest rates and terms, and to work with a reputable lender who can guide borrowers through the complexities of cash-out refinancing.

In conclusion, cash-out refinancing can be a valuable financial strategy for homeowners looking to access their home's equity. However, it's important to approach this type of refinancing with caution and to fully understand the potential risks and benefits before making a decision. By doing so, borrowers can make informed choices that align with their long-term financial goals.

Exploring Navy Federal Mortgages: A Comprehensive Comparison Guide

You may want to see also

Explore related products

![]()

Eligibility Criteria: Requirements for homeowners to qualify, including credit score, equity, and income verification

To qualify for a cash-out refinance mortgage, homeowners must meet specific eligibility criteria set by lenders. These requirements are designed to ensure that borrowers have the financial stability and creditworthiness to manage the new loan terms. One of the primary factors considered is the homeowner's credit score. Typically, lenders require a minimum credit score of 620 to 680, depending on the loan program and the amount of equity in the property. A higher credit score not only increases the chances of approval but may also result in more favorable interest rates.

In addition to credit score, lenders assess the amount of equity the homeowner has built up in the property. Equity is calculated by subtracting the outstanding mortgage balance from the current market value of the home. For a cash-out refinance, lenders usually require that the homeowner retains at least 20% equity in the property after the refinance. This ensures that the borrower has a sufficient stake in the home and reduces the risk of default.

Income verification is another crucial component of the eligibility criteria. Lenders need to confirm that the homeowner has a stable and sufficient income to cover the monthly mortgage payments. This typically involves reviewing pay stubs, tax returns, and bank statements. The debt-to-income ratio (DTI) is also evaluated, which compares the total monthly debt payments to the gross monthly income. A lower DTI indicates a better ability to manage debt, and lenders generally prefer a DTI of 36% or less for a cash-out refinance.

Furthermore, lenders may consider other factors such as employment history, assets, and the purpose of the cash-out refinance. Borrowers with a consistent employment record and substantial assets may be viewed more favorably. The intended use of the cash-out proceeds can also influence the lender's decision, as some uses may be considered more beneficial or less risky than others.

Meeting these eligibility criteria is essential for homeowners seeking to cash out on a refinance mortgage. By understanding and preparing for these requirements, borrowers can increase their chances of approval and secure more favorable loan terms.

Navigating the Financial Landscape: Affording Two Mortgages

You may want to see also

Explore related products

![]()

Calculation of Cash-Out Amount: Determining how much cash can be taken out based on home value and existing mortgage

To calculate the cash-out amount on a refinance mortgage, you need to understand the relationship between your home's value, the amount you owe on your existing mortgage, and the loan-to-value (LTV) ratio. The LTV ratio is a critical factor that lenders use to determine how much money they're willing to lend you. It's calculated by dividing the loan amount by the appraised value of the property. For example, if your home is appraised at $300,000 and you want to refinance for $200,000, your LTV ratio would be approximately 66.67%.

The first step in determining your cash-out amount is to get an accurate appraisal of your home's value. This will give you a clear understanding of how much equity you have built up in your property. Once you have the appraisal, you can subtract the amount you owe on your existing mortgage from the appraised value to find out how much equity you have available for a cash-out refinance.

Let's say your home is appraised at $300,000, and you currently owe $150,000 on your mortgage. This means you have $150,000 in equity. However, you won't be able to access all of this equity through a cash-out refinance. Lenders typically have maximum LTV ratios for cash-out refinances, which are often lower than those for rate-and-term refinances. For instance, a lender might allow a maximum LTV ratio of 80% for a cash-out refinance.

Using the 80% LTV ratio example, you would be able to refinance for up to $240,000 ($300,000 x 0.80). Since you owe $150,000 on your existing mortgage, you would be able to take out up to $90,000 in cash ($240,000 - $150,000). This cash can be used for various purposes, such as home improvements, debt consolidation, or other financial needs.

It's important to note that the cash-out amount you're eligible for may also be affected by other factors, such as your credit score, income, and debt-to-income ratio. Lenders will consider these factors when determining how much they're willing to lend you and at what interest rate. Additionally, you should be aware of the potential risks associated with cash-out refinances, such as increasing your mortgage debt and potentially facing higher interest rates or fees.

In conclusion, calculating the cash-out amount on a refinance mortgage involves understanding your home's value, your existing mortgage balance, and the LTV ratio. By following these steps and considering the factors that affect your eligibility, you can determine how much cash you can take out through a refinance mortgage.

Understanding Mortgages: A Comprehensive Guide to Home Financing

You may want to see also

Explore related products

![]()

Closing Costs and Fees: Overview of costs associated with refinancing, such as appraisal fees, title insurance, and origination fees

Closing costs and fees are an essential aspect of refinancing a mortgage, and understanding these expenses is crucial for homeowners looking to cash out on their refinance. One of the primary costs associated with refinancing is the appraisal fee, which typically ranges from $300 to $500. This fee covers the cost of a professional appraiser evaluating the property to determine its current market value, a necessary step in the refinancing process.

Another significant cost is title insurance, which protects the lender against any potential issues with the property's title. The cost of title insurance varies depending on the property's value and location but can range from $500 to $2,000. Origination fees, charged by the lender for processing the refinance application, are another common expense. These fees can range from 0.5% to 1% of the loan amount, which can add up to several thousand dollars for larger mortgages.

In addition to these primary costs, homeowners may also encounter other fees such as credit report fees, flood certification fees, and recording fees. It's essential to factor in these costs when considering a refinance, as they can significantly impact the overall financial benefit of the transaction. Homeowners should carefully review the Loan Estimate provided by their lender, which outlines all the costs associated with the refinance, to ensure they understand the full financial implications.

To minimize closing costs, homeowners can shop around for lenders that offer competitive rates and fees. They may also consider negotiating with the lender to reduce or waive certain fees. Additionally, homeowners can opt for a no-closing-cost refinance, where the lender covers the closing costs in exchange for a higher interest rate. However, this option may not always be the best choice, as the higher interest rate can result in increased long-term costs.

Ultimately, understanding and managing closing costs and fees is a critical component of the refinancing process. By carefully considering these expenses and exploring options to reduce them, homeowners can maximize the financial benefits of their refinance and achieve their financial goals.

Navigating Inflation: How Mortgages Adapt and Impact Homeownership

You may want to see also

Explore related products

![]()

Impact on Monthly Payments: How cash-out refinancing affects monthly mortgage payments, including potential increases due to higher loan amounts

Cash-out refinancing can significantly impact monthly mortgage payments, often leading to an increase due to the higher loan amount. This financial strategy involves refinancing an existing mortgage for more than the outstanding balance and receiving the difference in cash. While it can provide homeowners with access to funds for various purposes, such as home improvements or debt consolidation, it's crucial to understand the implications on monthly payments.

The primary factor influencing the change in monthly payments is the new loan amount. Since cash-out refinancing increases the principal balance, the monthly payments will likely rise to reflect the larger debt. Additionally, the interest rate on the new loan can affect the payment amount. If the rate is higher than the original mortgage, the increase in monthly payments will be more pronounced. Homeowners should carefully consider these factors and assess their financial situation before deciding on cash-out refinancing.

Another aspect to consider is the loan term. If the new loan has a shorter term than the original mortgage, the monthly payments may increase due to the accelerated repayment schedule. Conversely, a longer loan term could result in lower monthly payments, but it may also mean paying more interest over the life of the loan. Homeowners should weigh the pros and cons of different loan terms and their impact on monthly payments and overall financial goals.

Furthermore, cash-out refinancing may involve additional costs, such as closing costs and fees, which can further increase the monthly payment burden. It's essential to factor in these expenses when evaluating the feasibility of this financial strategy. Homeowners should also be aware of potential risks, such as the possibility of owing more on the mortgage than the home's value, which could complicate future refinancing or selling options.

In conclusion, while cash-out refinancing can provide homeowners with access to funds, it's crucial to carefully consider the impact on monthly mortgage payments. The increase in loan amount, interest rate, loan term, and additional costs all play a role in determining the new payment amount. Homeowners should thoroughly assess their financial situation and goals before deciding on this strategy to ensure it aligns with their long-term financial well-being.

From Main Street to Wall Street: The Mortgage Journey Explained

You may want to see also

Frequently asked questions

A cash-out refinance mortgage is a type of refinancing where the homeowner takes out a new mortgage for more than the amount they owe on their current mortgage, allowing them to receive cash from the difference.

The cash-out process involves applying for a new mortgage with a higher loan amount than the existing mortgage. Once approved, the new lender pays off the old mortgage and gives the homeowner the difference in cash.

The benefits of a cash-out refinance mortgage include receiving cash to use for various purposes such as home improvements, debt consolidation, or investments. It can also provide a lower interest rate or more favorable loan terms compared to the original mortgage.

Potential drawbacks of a cash-out refinance mortgage include increasing the total amount of debt, potentially higher interest rates or fees, and the risk of losing the home if the homeowner cannot make the new mortgage payments.