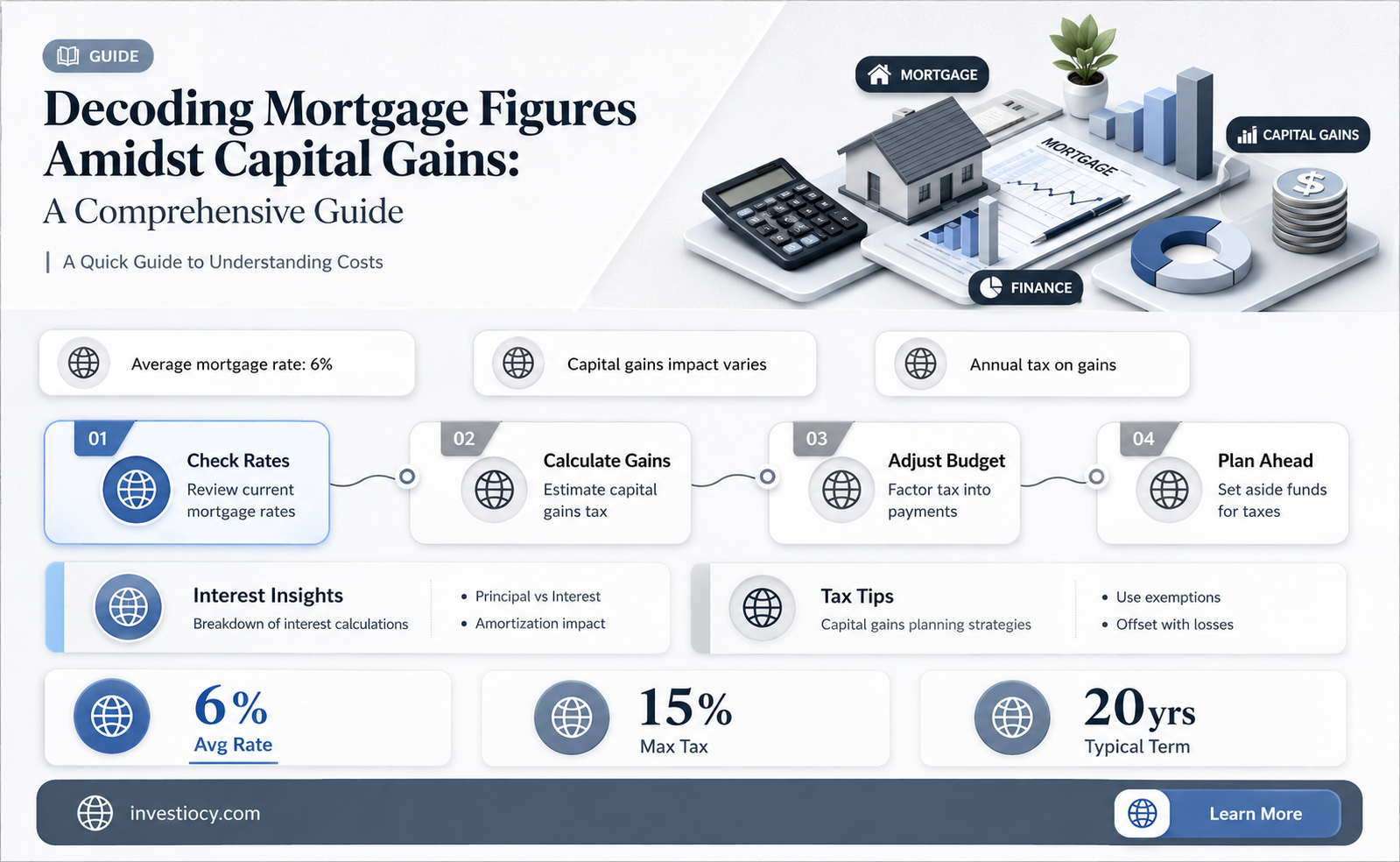

When calculating mortgage figures, it's essential to consider the impact of capital gains. Capital gains refer to the increase in value of an asset over time, and in the context of real estate, this can significantly affect mortgage calculations. As property values appreciate, homeowners may choose to refinance their mortgage or sell their property, which can result in a capital gain. This gain must be factored into the mortgage figure to ensure accurate financial planning. Additionally, capital gains can influence the loan-to-value ratio, which is a critical component in determining mortgage eligibility and interest rates. Understanding how capital gains interact with mortgage figures is crucial for both homeowners and lenders to make informed decisions in the dynamic real estate market.

Explore related products

What You'll Learn

- Mortgage Interest Deduction: How mortgage interest impacts taxable income and potential capital gains

- Capital Gains Tax: Overview of capital gains tax rates and how they apply to mortgage-related gains

- Home Equity: How mortgage payments contribute to building home equity, which can affect capital gains

- Refinancing and Capital Gains: Implications of refinancing a mortgage on capital gains tax liabilities

- Selling a Home: How mortgage figures influence the calculation of capital gains upon selling a property

![]()

Mortgage Interest Deduction: How mortgage interest impacts taxable income and potential capital gains

The mortgage interest deduction is a significant aspect of homeownership that can greatly impact an individual's taxable income and potential capital gains. When homeowners pay mortgage interest, they are essentially reducing their taxable income for the year, which can lead to a lower tax bill. This deduction is particularly beneficial for those in higher tax brackets, as it can result in substantial savings.

However, it's important to note that the mortgage interest deduction is not unlimited. There are caps on the amount of interest that can be deducted, and these limits may vary depending on the tax laws in place. Additionally, the deduction is only available for interest paid on a primary residence or a second home, and it cannot be used for investment properties.

In terms of capital gains, the mortgage interest deduction can play a crucial role in determining the overall profit from the sale of a home. By reducing taxable income, the deduction can help homeowners stay within a lower capital gains tax bracket, which can result in a smaller tax bill on the sale of their property. This is especially important for those who have owned their home for a long period of time and may be subject to higher capital gains taxes.

To maximize the benefits of the mortgage interest deduction, homeowners should ensure that they are keeping accurate records of their mortgage interest payments. This includes maintaining copies of their mortgage statements and any other relevant documentation. Additionally, it's important to consult with a tax professional to understand how the deduction may impact individual tax situations and to ensure compliance with all applicable tax laws.

In conclusion, the mortgage interest deduction can be a valuable tool for homeowners looking to reduce their taxable income and potential capital gains. By understanding the intricacies of this deduction and taking steps to maximize its benefits, homeowners can make the most of their investment in their property.

Understanding Mortgage Escrow: Why Your Balance Might Hit Zero

You may want to see also

Explore related products

![]()

Capital Gains Tax: Overview of capital gains tax rates and how they apply to mortgage-related gains

Capital gains tax is a crucial consideration when it comes to mortgage-related transactions. This tax is levied on the profit made from the sale of a property, and it can significantly impact the overall financial outcome of a mortgage deal. Understanding the capital gains tax rates and how they apply to mortgage-related gains is essential for both lenders and borrowers.

The capital gains tax rate varies depending on the taxpayer's income bracket and the length of time the property was held. For example, in the United States, the capital gains tax rate for long-term gains (held for more than one year) ranges from 0% to 20%, while the rate for short-term gains (held for one year or less) is the same as the taxpayer's ordinary income tax rate. This means that the longer a property is held, the lower the capital gains tax rate will be.

When it comes to mortgage-related gains, the capital gains tax is typically applied to the difference between the sale price of the property and the outstanding mortgage balance. For instance, if a property is sold for $500,000 and the outstanding mortgage balance is $300,000, the capital gains tax would be applied to the $200,000 profit. This is an important consideration for borrowers who are looking to sell their property, as the capital gains tax can significantly reduce the amount of money they walk away with from the sale.

Lenders also need to be aware of the capital gains tax implications when it comes to mortgage-related transactions. For example, if a lender is considering a short sale or a foreclosure, they need to understand how the capital gains tax will impact the financial outcome of the transaction. In some cases, the capital gains tax may be waived or reduced if the property is sold at a loss or if the borrower is facing financial hardship.

In conclusion, understanding the capital gains tax rates and how they apply to mortgage-related gains is essential for both lenders and borrowers. This knowledge can help taxpayers make informed decisions about their mortgage transactions and minimize their tax liability.

Streamlining Mortgage Processes: CRM and LOS Integration Explained

You may want to see also

Explore related products

![]()

Home Equity: How mortgage payments contribute to building home equity, which can affect capital gains

Each mortgage payment you make contributes to building home equity, which is the difference between your home's market value and the outstanding balance of your mortgage. As you pay down your mortgage, your equity increases, and this can have a significant impact on your capital gains when you eventually sell your home.

For example, let's say you bought a home for $300,000 with a 20% down payment and a 30-year fixed-rate mortgage at 4%. After 10 years of making payments, you would have paid off approximately $43,000 of your mortgage principal, increasing your home equity to around $143,000. If you were to sell your home at this point for $350,000, your capital gain would be $50,000, which is the difference between the sale price and your original purchase price.

However, it's important to note that the relationship between mortgage payments and capital gains is not always straightforward. For instance, if your home's value decreases over time, your equity may not increase as quickly, and your capital gains may be lower than expected. Additionally, if you refinance your mortgage or take out a home equity loan, this can affect your equity and capital gains calculations.

To maximize your capital gains, it's essential to understand how your mortgage payments contribute to building home equity and to make informed decisions about your home financing options. By doing so, you can ensure that you are in the best possible position to benefit from the appreciation of your home's value over time.

Navigating the Intersection of Mortgages and 1031 Exchanges

You may want to see also

Explore related products

![]()

Refinancing and Capital Gains: Implications of refinancing a mortgage on capital gains tax liabilities

Refinancing a mortgage can have significant implications on capital gains tax liabilities. When a homeowner refinances their mortgage, they are essentially taking out a new loan to pay off the old one. This process can trigger capital gains tax if the new loan amount exceeds the original purchase price of the property. The excess amount is considered a capital gain and is subject to taxation.

For example, let's say a homeowner purchased a property for $200,000 and has a mortgage balance of $150,000. If they refinance their mortgage for $250,000, the excess amount of $50,000 is considered a capital gain. This gain is subject to capital gains tax, which can be a significant financial burden for the homeowner.

However, there are certain exceptions and exclusions that can apply to refinancing and capital gains tax. For instance, the IRS allows homeowners to exclude up to $250,000 of capital gains from the sale of their primary residence if they have lived in the property for at least two of the five years leading up to the sale. This exclusion can also apply to refinancing if the homeowner uses the excess loan amount to improve the property or pay off other debts.

It's important for homeowners to carefully consider the implications of refinancing on their capital gains tax liabilities. They should consult with a tax professional to determine if refinancing is the right option for their situation and to ensure they are taking advantage of any available tax benefits.

In conclusion, refinancing a mortgage can have significant implications on capital gains tax liabilities. Homeowners should carefully consider the potential tax consequences of refinancing and consult with a tax professional to ensure they are making an informed decision.

Understanding the Impact of Mortgages on Your Balance Sheet

You may want to see also

Explore related products

![]()

Selling a Home: How mortgage figures influence the calculation of capital gains upon selling a property

When selling a home, understanding how mortgage figures influence the calculation of capital gains is crucial for accurate financial planning. The mortgage balance at the time of sale directly impacts the amount of equity available to the seller, which in turn affects the capital gains calculation. For instance, if a homeowner sells their property for $300,000 but still owes $150,000 on the mortgage, their equity—and thus potential capital gains—is reduced to $150,000.

Moreover, the interest rates and terms of the mortgage can also play a role in determining capital gains. If the mortgage has a high interest rate, the homeowner may have paid more in interest over the years, reducing the overall equity in the property. Conversely, a lower interest rate could mean more of the payments went towards the principal, increasing the equity and potential capital gains. Additionally, the length of time the homeowner has held the mortgage can influence the capital gains tax rate, with longer-term holdings often qualifying for more favorable tax treatment.

It's also important to consider any mortgage prepayment penalties or closing costs associated with the sale, as these can further impact the net proceeds and capital gains calculation. Homeowners should carefully review their mortgage terms and consult with a financial advisor to understand how these factors will affect their specific situation.

In summary, mortgage figures are a critical component in calculating capital gains upon selling a property. The balance, interest rate, term, and associated costs all play a role in determining the homeowner's equity and the resulting tax implications. By understanding these factors, sellers can better navigate the financial aspects of selling their home and make informed decisions.

Decoding Modern Mortgages: Insights from Jared Vennett

You may want to see also

Frequently asked questions

Mortgage interest can be deducted from your taxable income, which may reduce the amount of capital gains tax you owe. This is because the interest expense lowers your overall taxable income, potentially placing you in a lower tax bracket.

If you sell your house with a mortgage, the outstanding mortgage balance will be deducted from the sale proceeds to determine the capital gain. You will only pay capital gains tax on the difference between the sale price and the mortgage balance, minus any other allowable deductions.

You cannot deduct mortgage payments directly from your capital gains. However, you can deduct the interest portion of your mortgage payments from your taxable income, which may indirectly reduce your capital gains tax liability.

Refinancing a mortgage does not directly impact capital gains. However, if you refinance to a lower interest rate, you may save money on interest payments, which could increase your overall profit when you sell the property. This increased profit could potentially lead to a higher capital gain.

Mortgage debt can reduce the amount of capital gains tax you owe. When you sell a property, the outstanding mortgage balance is subtracted from the sale price to calculate the capital gain. Additionally, the interest paid on the mortgage can be deducted from your taxable income, further reducing your tax liability.

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)