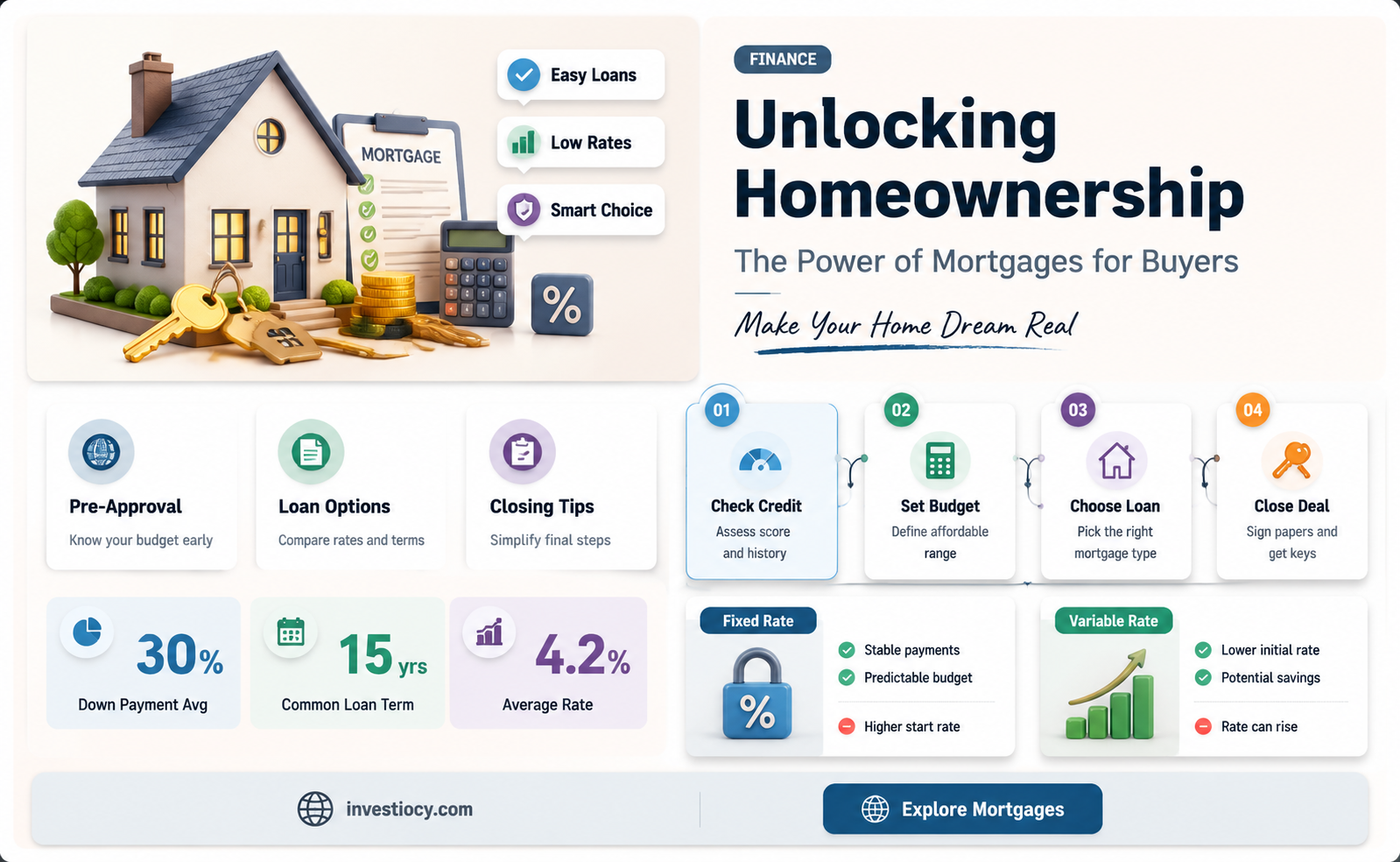

A mortgage is a powerful financial tool that enables individuals to purchase homes without requiring the full amount upfront. By providing a structured repayment plan, mortgages make homeownership accessible to a wider range of buyers. This financial arrangement allows borrowers to spread the cost of their home over several years, typically 15 to 30, making monthly payments more manageable. Mortgages also offer the advantage of building equity over time, as each payment contributes to the borrower's ownership stake in the property. Additionally, mortgages can provide tax benefits, as interest payments are often deductible. Overall, mortgages play a crucial role in facilitating the dream of homeownership for many people.

Explore related products

What You'll Learn

- Financial Leverage: Mortgages allow buyers to purchase homes with a smaller down payment, leveraging borrowed funds

- Tax Benefits: Mortgage interest and property taxes are often tax-deductible, reducing the buyer's taxable income

- Building Equity: As buyers pay down their mortgage, they build equity in their home, which can be a valuable asset

- Predictable Payments: Fixed-rate mortgages offer stable monthly payments, making budgeting easier for homeowners

- Access to Credit: Mortgages provide access to large sums of money that might not be available through other means

![]()

Financial Leverage: Mortgages allow buyers to purchase homes with a smaller down payment, leveraging borrowed funds

Mortgages provide a powerful tool for homebuyers through financial leverage, enabling them to purchase properties with a smaller upfront investment. This leverage is achieved by borrowing a significant portion of the home's value, which allows buyers to enter the real estate market with less capital than would otherwise be required. For instance, with a 20% down payment, a buyer can secure a mortgage for the remaining 80% of the home's purchase price, effectively controlling a substantial asset with a relatively modest sum.

The ability to leverage borrowed funds in this manner offers several advantages. Firstly, it makes homeownership more accessible to a wider range of individuals and families who may not have the means to save for a large down payment. This democratization of the housing market can contribute to increased economic stability and growth, as more people are able to invest in property and build equity.

Moreover, financial leverage through mortgages can amplify the potential returns on investment in real estate. When property values appreciate, the gains are realized on the entire value of the home, not just the portion financed by the down payment. This means that even a small increase in property value can result in a significant return on the buyer's initial investment. For example, if a home purchased with a 20% down payment appreciates by 10%, the buyer's equity in the property would increase by 50% of the original down payment, illustrating the potent effect of leverage.

However, it is important to note that financial leverage also introduces risks. The higher the level of borrowing, the greater the potential for financial strain if interest rates rise or property values decline. Buyers must carefully consider their ability to manage these risks and ensure that they are not overextending themselves financially. Additionally, the use of leverage can increase the total cost of homeownership over time, as interest payments on the mortgage can add up significantly.

In conclusion, mortgages offer a valuable mechanism for homebuyers to leverage borrowed funds, making it possible to purchase homes with a smaller down payment. This financial leverage can enhance accessibility to the housing market and potentially increase investment returns, but it also necessitates a careful assessment of the associated risks and costs. By understanding and managing these factors, buyers can effectively utilize mortgages to achieve their homeownership goals.

Navigating the Intersection of Mortgages and 1031 Exchanges

You may want to see also

Explore related products

![]()

Tax Benefits: Mortgage interest and property taxes are often tax-deductible, reducing the buyer's taxable income

One of the most significant advantages of owning a home with a mortgage is the potential for tax deductions. Mortgage interest and property taxes are often tax-deductible, which can substantially reduce a homeowner's taxable income. This means that a portion of the money paid towards interest and taxes can be reclaimed when filing annual tax returns, effectively lowering the overall cost of homeownership.

To understand how this works, it's important to know that the interest portion of a mortgage payment is typically the largest component in the early years of a loan. As the loan amortizes, the interest paid decreases over time. Property taxes, on the other hand, are usually paid annually and can vary based on the property's value and the local tax rate. By deducting these amounts from taxable income, homeowners can potentially save thousands of dollars each year.

For example, if a homeowner pays $10,000 in mortgage interest and $2,000 in property taxes in a given year, they could potentially deduct $12,000 from their taxable income. This would result in a lower tax bill, depending on their tax bracket. It's important to note that there are limits to these deductions, and homeowners should consult with a tax professional to understand how these benefits apply to their specific situation.

Additionally, there are other tax benefits associated with homeownership, such as the ability to deduct points paid at closing and the potential for capital gains exclusions when selling a primary residence. These benefits can further enhance the financial advantages of owning a home with a mortgage.

In summary, the tax benefits of mortgage interest and property tax deductions can significantly reduce the cost of homeownership. By understanding these benefits and how they apply, homeowners can make informed decisions about their finances and potentially save money on their annual tax returns.

Decoding Modern Mortgages: Insights from Jared Vennett

You may want to see also

Explore related products

![]()

Building Equity: As buyers pay down their mortgage, they build equity in their home, which can be a valuable asset

As homeowners make their monthly mortgage payments, they gradually build equity in their property. This equity represents the portion of the home's value that the owner has paid for and can be a significant financial asset over time. For instance, if a buyer purchases a home for $300,000 with a 20% down payment and a mortgage for the remaining $240,000, they immediately have $60,000 in equity. As they pay down the mortgage, this equity increases. After 10 years of payments, assuming a standard 30-year mortgage at a 4% interest rate, the buyer would have paid off approximately $80,000 of the principal, increasing their equity to around $140,000.

Building equity is particularly valuable because it can provide a cushion against market fluctuations. If property values decline, as they did during the 2008 financial crisis, homeowners with substantial equity are less likely to find themselves underwater on their mortgage, where the outstanding loan balance exceeds the property's value. Additionally, equity can be leveraged for other financial goals. Homeowners can take out a home equity loan or line of credit to fund renovations, education, or other major expenses, often at lower interest rates than unsecured loans or credit cards.

However, it's important to note that building equity is not automatic and requires consistent payments and potentially additional contributions towards the principal. Homeowners should be aware of their loan terms and make extra payments whenever possible to accelerate equity growth. Furthermore, while equity can be a valuable asset, it is illiquid, meaning it cannot be easily converted to cash without selling the property or taking out a loan. As such, it should be considered a long-term investment rather than a short-term financial strategy.

In summary, building equity through mortgage payments is a key benefit of homeownership, providing financial security and potential access to funds for other needs. By understanding how equity works and making informed decisions about their mortgage, homeowners can maximize this asset and achieve their financial goals.

Smart Financial Moves: Paying Off Debt with Mortgage Proceeds

You may want to see also

Explore related products

![]()

Predictable Payments: Fixed-rate mortgages offer stable monthly payments, making budgeting easier for homeowners

Fixed-rate mortgages provide homeowners with a significant advantage in terms of financial predictability. Unlike variable-rate mortgages, which can fluctuate based on market conditions, fixed-rate mortgages lock in an interest rate for the duration of the loan term. This means that borrowers can expect the same monthly payment amount throughout the life of their mortgage, making it easier to plan and budget for the future.

One of the primary benefits of predictable payments is the ability to create a stable financial foundation. Homeowners can allocate a consistent portion of their income towards their mortgage each month, knowing that this expense will not change unexpectedly. This stability can be particularly helpful for those who are managing tight budgets or who have other significant financial commitments, such as student loans or credit card debt.

Furthermore, fixed-rate mortgages can help borrowers avoid the pitfalls of payment shock, which can occur when the interest rate on a variable-rate mortgage increases suddenly. Payment shock can lead to financial strain and even default, as borrowers struggle to adjust to the new, higher monthly payments. By contrast, fixed-rate mortgages eliminate this risk, providing borrowers with a clear understanding of their financial obligations from the outset.

In addition to the financial benefits, predictable payments can also offer psychological advantages. Knowing that their mortgage payments will remain stable can reduce stress and anxiety for homeowners, allowing them to focus on other aspects of their lives. This peace of mind can be particularly valuable during times of economic uncertainty, when variable-rate mortgages may be subject to significant fluctuations.

Overall, the predictable payments offered by fixed-rate mortgages can provide homeowners with a sense of security and control over their finances. By locking in a stable monthly payment, borrowers can better manage their budgets, avoid the risks associated with variable-rate mortgages, and enjoy greater peace of mind.

Streamlining Mortgage Processes: CRM and LOS Integration Explained

You may want to see also

Explore related products

![]()

Access to Credit: Mortgages provide access to large sums of money that might not be available through other means

Mortgages serve as a critical financial tool, enabling individuals to access substantial funds that may be out of reach through other financing avenues. This access to credit is particularly significant in the context of purchasing real estate, where the sums involved are typically large. Without mortgages, many prospective homebuyers would face considerable challenges in accumulating the necessary capital to make a purchase.

One of the primary benefits of mortgages is their ability to leverage the value of the property being purchased. By using the property as collateral, lenders are more willing to extend credit, often at more favorable interest rates compared to unsecured loans. This arrangement allows buyers to finance a significant portion of their home purchase, thereby reducing the upfront cash requirements.

Furthermore, mortgages can provide flexibility in terms of repayment structures. Various types of mortgages, such as fixed-rate, adjustable-rate, and interest-only mortgages, cater to different financial situations and preferences. This flexibility enables borrowers to choose a repayment plan that aligns with their current financial capabilities and future expectations, making homeownership more attainable for a broader range of individuals.

In addition to facilitating home purchases, mortgages can also play a role in wealth accumulation. As homeowners pay down their mortgages, they build equity in their properties, which can appreciate over time. This equity can then be leveraged for other financial goals, such as funding education, starting a business, or supplementing retirement income. Thus, mortgages not only provide access to credit for purchasing homes but also contribute to long-term financial stability and growth.

However, it is essential for potential homebuyers to approach mortgages with caution and a thorough understanding of the associated responsibilities. Mortgages are long-term commitments that require regular payments, and failure to meet these obligations can result in serious consequences, including foreclosure. Therefore, borrowers must carefully assess their financial situation, consider their long-term goals, and select a mortgage that suits their needs while ensuring they can manage the repayments comfortably.

In conclusion, mortgages are a vital means of accessing credit for home purchases, offering benefits such as leveraging property value, flexible repayment options, and potential for wealth accumulation. Nonetheless, it is crucial for borrowers to exercise prudence and fully comprehend the implications of taking on a mortgage to avoid potential financial pitfalls.

Understanding Inflation's Effect on Your Mortgage Costs

You may want to see also

Frequently asked questions

A mortgage provides buyers with the necessary funds to purchase a home, allowing them to make a significant investment without having to pay the full price upfront. This financial assistance enables buyers to enter the housing market and achieve homeownership.

Using a mortgage to buy a home offers several benefits, including the ability to purchase a property without saving for the entire purchase price, potentially lower monthly payments compared to renting, and the opportunity to build equity over time as the home appreciates in value.

A mortgage works by requiring the borrower to make regular payments, typically monthly, to repay the loan amount plus interest. The payments are structured to cover both the principal balance and the interest accrued over the loan term, with the goal of fully paying off the mortgage by the end of the term.

The interest rate on a mortgage is influenced by various factors, including the borrower's credit score, the loan-to-value ratio, the loan term, and current market conditions. Borrowers with higher credit scores and lower loan-to-value ratios generally qualify for lower interest rates.

A mortgage can help buyers build credit by demonstrating their ability to make consistent and timely payments on a significant loan. As borrowers make their mortgage payments on time, their credit scores may improve, which can lead to better financial opportunities in the future.

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)