Facing foreclosure from a second mortgage can be a daunting experience, but it's not an insurmountable challenge. Many homeowners have successfully navigated this situation by employing various strategies and seeking professional guidance. In this guide, we'll explore practical steps and expert advice on how to beat foreclosure from a second mortgage. From understanding your rights and options to negotiating with lenders and exploring government assistance programs, we'll provide you with the tools and knowledge needed to protect your home and financial well-being.

Explore related products

$12.95

What You'll Learn

- Understanding Foreclosure Process: Learn the legal steps and timeline of foreclosure to better navigate your situation

- Communication with Lenders: Tips on how to effectively communicate with your lenders to negotiate better terms or a repayment plan

- Exploring Loan Modification Options: Discover different types of loan modifications that could help make your mortgage payments more manageable

- Seeking Professional Help: Guidance on when and how to seek assistance from a housing counselor or attorney specializing in foreclosure

- Rebuilding Credit Post-Foreclosure: Strategies for rebuilding your credit score after a foreclosure to improve future financial opportunities

![]()

Understanding Foreclosure Process: Learn the legal steps and timeline of foreclosure to better navigate your situation

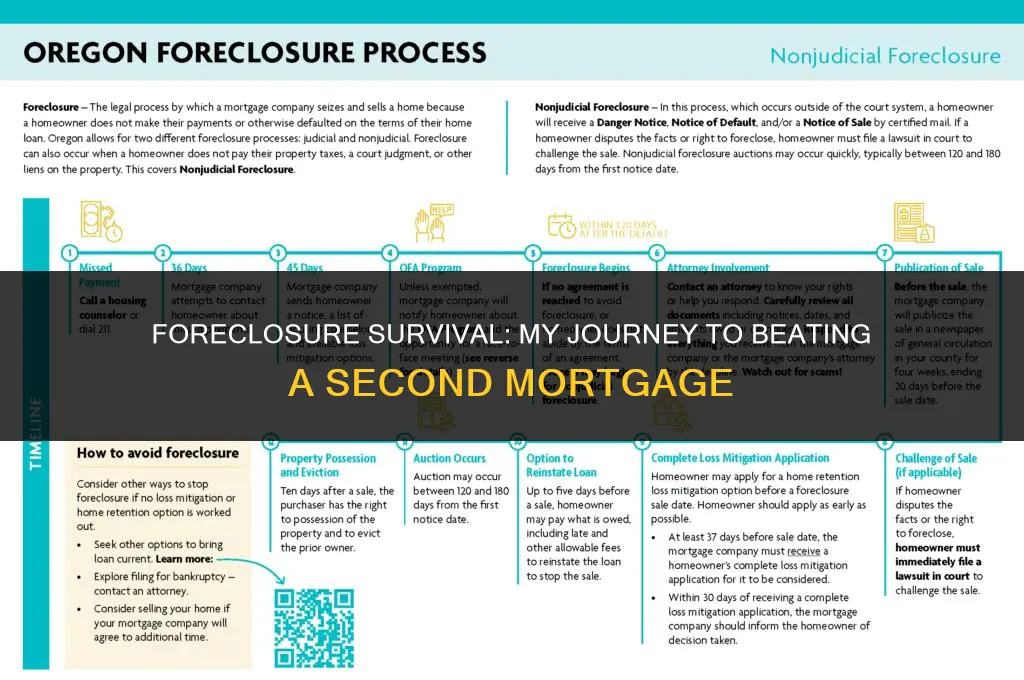

The foreclosure process can be complex and intimidating, but understanding the legal steps and timeline is crucial for anyone facing the possibility of losing their home. The process typically begins when a homeowner fails to make mortgage payments, triggering a series of events that can lead to the sale of the property. It's important to note that foreclosure laws vary by state, so it's essential to familiarize yourself with the specific regulations in your area.

The first step in the foreclosure process is usually a notice of default, which is sent to the homeowner by the lender. This notice informs the homeowner that they have failed to make payments and provides a timeframe for them to cure the default. If the homeowner is unable to make the required payments within this timeframe, the lender may file a notice of sale, which sets a date for the property to be auctioned off.

One of the most critical aspects of the foreclosure process is understanding the timeline. The time it takes for a foreclosure to be completed can vary significantly depending on the state and the specific circumstances of the case. In some states, the entire process can take several months, while in others it may take years. Homeowners should be aware of the timeline in their state and use this information to their advantage when trying to avoid foreclosure.

There are several ways to potentially beat foreclosure from a second mortgage, but each strategy has its own risks and benefits. One common approach is to negotiate with the lender to modify the terms of the loan or to obtain a forbearance agreement. Another option is to file for bankruptcy, which can temporarily halt the foreclosure process and give the homeowner more time to work out a solution.

It's important to remember that the foreclosure process is not inevitable, and there are resources available to help homeowners navigate this difficult situation. By understanding the legal steps and timeline of foreclosure, homeowners can make informed decisions about how to proceed and potentially avoid losing their home.

Exploring the Heights: Average Mortgage Costs for Mansions Unveiled

You may want to see also

Explore related products

![]()

Communication with Lenders: Tips on how to effectively communicate with your lenders to negotiate better terms or a repayment plan

Effective communication with lenders is crucial when facing foreclosure, especially when dealing with a second mortgage. Here are some tips to help you navigate these conversations and potentially negotiate better terms or a repayment plan:

- Be Proactive: Don't wait until you're behind on payments to reach out to your lender. As soon as you realize you might have trouble making your payments, contact them to discuss your options. This shows that you're taking responsibility for your situation and are willing to work with them to find a solution.

- Know Your Rights: Familiarize yourself with your rights as a borrower and the laws that protect you. This knowledge will give you confidence during negotiations and help you understand what terms you can realistically expect.

- Prepare Your Documentation: Gather all relevant financial documents, including your income statements, expenses, and any other debts you have. This information will help your lender assess your situation and determine what kind of assistance they can offer.

- Be Honest and Transparent: When discussing your financial situation with your lender, be completely honest about your circumstances. Transparency builds trust and helps your lender understand your needs.

- Explore All Options: Ask your lender about all possible solutions, such as loan modifications, forbearance agreements, or repayment plans. Be open to different options and work with your lender to find the best solution for your situation.

- Follow Up: After your initial conversation, follow up with your lender regularly to ensure that any agreements or plans are being processed. This shows that you're committed to resolving your situation and helps keep the lines of communication open.

By following these tips, you can improve your chances of successfully communicating with your lenders and negotiating a plan that helps you avoid foreclosure on your second mortgage. Remember, the key is to be proactive, prepared, and persistent in your efforts to find a solution.

Decoding the Ideal FICO Score for Your Mortgage Journey

You may want to see also

Explore related products

![]()

Exploring Loan Modification Options: Discover different types of loan modifications that could help make your mortgage payments more manageable

One effective strategy to prevent foreclosure on a second mortgage is to explore various loan modification options. These modifications can help make your mortgage payments more manageable by adjusting the terms of your loan. For instance, a lender may agree to lower your interest rate, extend the repayment period, or even forgive a portion of the principal balance. It's crucial to understand the different types of loan modifications available and how they can impact your financial situation.

To begin exploring loan modification options, it's essential to review your current loan terms and identify areas where adjustments could provide relief. Consider factors such as your interest rate, monthly payment amount, and the remaining balance on your loan. You may want to consult with a financial advisor or a housing counselor to help you navigate the process and determine which modification options are most suitable for your circumstances.

Some common types of loan modifications include:

- Interest Rate Reduction: This modification involves lowering the interest rate on your loan, which can significantly reduce your monthly payment amount.

- Payment Deferral: With this option, you may be able to postpone making payments for a certain period, allowing you to catch up on other expenses.

- Principal Reduction: In some cases, lenders may agree to forgive a portion of the principal balance, reducing the overall amount you owe.

- Loan Term Extension: Extending the repayment period can lower your monthly payments by spreading the remaining balance over a longer timeframe.

When exploring loan modification options, it's important to be aware of potential drawbacks and risks. For example, modifying your loan terms may result in higher overall interest payments or extend the time it takes to pay off your mortgage. Additionally, some modifications may have tax implications or affect your credit score.

To successfully navigate the loan modification process, it's crucial to be proactive and communicate openly with your lender. Be prepared to provide documentation of your financial situation and demonstrate your ability to make modified payments. Remember that each lender has its own policies and procedures regarding loan modifications, so it's essential to research and understand the specific requirements and options available to you.

Navigating Homeowners Claims Without a Mortgage: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Seeking Professional Help: Guidance on when and how to seek assistance from a housing counselor or attorney specializing in foreclosure

Navigating the complexities of foreclosure, especially when it involves a second mortgage, can be overwhelming. Knowing when to seek professional help is crucial in this process. A housing counselor or attorney specializing in foreclosure can provide invaluable guidance, but it's essential to understand the right time to consult them and how to make the most of their assistance.

One of the key indicators that it's time to seek professional help is when you're struggling to understand the legal notices or documents related to your foreclosure. These documents often contain complex legal jargon and clauses that can be difficult to decipher without expert knowledge. A housing counselor or attorney can help you understand these documents, explain your rights and options, and guide you through the legal process.

Another critical situation where professional help is necessary is when you're facing a potential foreclosure due to missed payments. A housing counselor can help you explore options such as loan modification, refinancing, or repayment plans. They can also assist in negotiating with your lender to find a solution that works for both parties. If your situation is more complex, an attorney specializing in foreclosure can provide legal representation and help you navigate the court system if necessary.

It's also important to seek professional help if you suspect fraud or illegal practices related to your foreclosure. An attorney can investigate these claims and take legal action if needed. They can also help you understand the laws and regulations that protect you from predatory lending practices and ensure that your rights are upheld throughout the foreclosure process.

When seeking professional help, it's crucial to do your research and find a reputable housing counselor or attorney. Look for professionals who are certified or licensed in their field and have experience dealing with foreclosure cases. You can ask for referrals from friends, family, or local community organizations. It's also a good idea to check online reviews and consult with multiple professionals before making a decision.

In conclusion, seeking professional help when dealing with foreclosure from a second mortgage can make a significant difference in the outcome of your situation. By understanding when to seek assistance and how to find a qualified professional, you can navigate the foreclosure process with more confidence and potentially avoid losing your home.

Exploring Mortgage Costs: A Comprehensive Guide to Your Dream Home

You may want to see also

Explore related products

![]()

Rebuilding Credit Post-Foreclosure: Strategies for rebuilding your credit score after a foreclosure to improve future financial opportunities

After a foreclosure, rebuilding your credit score is crucial for improving future financial opportunities. One effective strategy is to obtain a secured credit card, which requires a security deposit that becomes your credit limit. This helps lenders see that you're committed to responsible credit use. Another option is to become an authorized user on someone else's credit card, piggybacking on their good credit habits to boost your score.

It's also important to pay all bills on time, every time. This includes not just credit cards, but also utilities, rent, and any other recurring payments. Setting up automatic payments can help ensure you never miss a due date. Additionally, keeping your credit utilization ratio low – ideally below 30% – can significantly improve your score. This means not maxing out your credit cards and paying off balances in full each month if possible.

Disputing errors on your credit report can also help raise your score. Obtain a free copy of your report from each of the three major credit bureaus and review it carefully for any inaccuracies. If you find errors, dispute them through the bureau's website or by mail. Be prepared to provide documentation to support your claim.

Finally, consider working with a credit counselor or financial advisor who specializes in post-foreclosure credit repair. They can provide personalized guidance and help you develop a comprehensive plan for rebuilding your credit. Remember, rebuilding your credit score takes time and patience, but with consistent effort and smart strategies, you can improve your financial standing and increase your chances of securing loans and credit in the future.

Decoding the Mortgage: How Much House Can $1,800 a Month Buy?

You may want to see also

Frequently asked questions

The primary strategies include negotiating with the lender, filing for bankruptcy, selling the property, or refinancing the mortgage. Each strategy has its own set of requirements and potential outcomes, and it's essential to understand the implications of each before proceeding.

Yes, negotiating with the lender is often a viable option. You can propose a loan modification, a short sale, or a deed in lieu of foreclosure. It's crucial to demonstrate financial hardship and provide documentation to support your request.

Filing for bankruptcy can help by automatically staying the foreclosure process. This gives you time to reorganize your finances and potentially negotiate a more favorable mortgage agreement. However, bankruptcy should be considered a last resort, as it has long-term consequences on your credit score and financial standing.

A short sale can help you avoid foreclosure, but it may also result in a deficiency judgment from the lender for the difference between the sale price and the outstanding mortgage balance. Additionally, a short sale can negatively impact your credit score, although typically less than a foreclosure.