Investment interest refers to the earnings generated from investments, typically in the form of dividends, interest, or capital gains. It is a crucial component of investment returns, as it represents the compensation investors receive for putting their capital at risk. Understanding investment interest is essential for making informed financial decisions, as it can impact the overall performance of an investment portfolio.

| Characteristics | Values |

|---|---|

| Definition | Investment interest refers to the income earned from investments, such as stocks, bonds, mutual funds, or real estate. |

| Types | There are two main types of investment interest: earned interest (from bonds and savings accounts) and capital gains (from stocks and other securities). |

| Taxation | Investment interest is generally taxable, but the rate and type of tax can vary depending on the investment and the investor's tax bracket. |

| Compound Interest | Investment interest can be compounded, meaning the interest earned can be reinvested to generate additional interest. |

| Risk | The level of risk associated with investment interest varies depending on the type of investment. Stocks, for example, carry more risk than bonds or savings accounts. |

| Liquidity | The liquidity of investment interest also varies. Some investments, like stocks, can be easily converted to cash, while others, like real estate, may take longer. |

| Purpose | Investment interest can serve multiple purposes, including generating additional income, funding retirement, or achieving specific financial goals. |

| Market Impact | The performance of the overall market can significantly impact investment interest. Bull markets tend to generate higher returns, while bear markets can lead to losses. |

| Diversification | Diversifying investments can help mitigate risk and potentially increase returns by spreading investment interest across different asset classes. |

| Time Horizon | The time horizon of an investment can affect the amount of interest earned. Longer-term investments generally have the potential for higher returns. |

| Fees and Expenses | Fees and expenses associated with investments can eat into the interest earned. It's important to consider these costs when evaluating investment options. |

| Regulatory Environment | The regulatory environment can impact investment interest. Changes in laws and regulations can affect the taxation, risk, and returns of investments. |

| Economic Conditions | Economic conditions, such as inflation and interest rates, can also influence investment interest. High inflation can erode the purchasing power of returns, while changes in interest rates can affect the yield of bonds and savings accounts. |

| Investor Knowledge | An investor's knowledge and experience can play a crucial role in the success of their investments and the interest they earn. Educated investors tend to make more informed decisions. |

| Emotional Factors | Emotional factors, such as fear and greed, can impact investment decisions and, consequently, the interest earned. Maintaining a disciplined approach is key to successful investing. |

Explore related products

What You'll Learn

- Definition: Investment interest refers to the income earned from investments, such as stocks, bonds, or mutual funds

- Types: There are various types of investment interest, including dividends, capital gains, and interest income from bonds

- Calculation: Investment interest is typically calculated as a percentage of the principal amount invested, using formulas specific to each investment type

- Taxation: In many jurisdictions, investment interest is subject to taxation, with rates varying depending on the type of investment and the investor's tax bracket

- Strategies: Investors may use various strategies to maximize investment interest, such as diversifying their portfolio or reinvesting dividends to compound returns

![]()

Definition: Investment interest refers to the income earned from investments, such as stocks, bonds, or mutual funds

Investment interest is a crucial concept in the realm of finance, representing the income generated from various investment vehicles such as stocks, bonds, and mutual funds. This interest is typically earned through the appreciation of the investment's value over time, as well as through regular dividend payments or interest distributions. Understanding investment interest is essential for investors seeking to grow their wealth and achieve their financial goals.

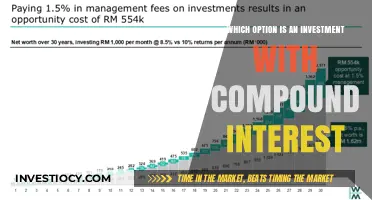

One key aspect of investment interest is its compounding nature. When interest is reinvested back into the principal investment, it can generate additional interest, leading to exponential growth over time. This compounding effect can significantly enhance an investor's returns, making it a powerful tool for long-term wealth accumulation.

The calculation of investment interest can vary depending on the type of investment. For example, stocks may pay dividends, which are a portion of the company's profits distributed to shareholders. Bonds, on the other hand, typically pay interest in the form of regular coupon payments. Mutual funds may distribute interest income from the underlying securities they hold, as well as capital gains from the sale of those securities.

Investors should also be aware of the tax implications of investment interest. In many jurisdictions, investment interest is subject to taxation, which can impact the overall returns on an investment. Understanding the tax laws and regulations surrounding investment interest can help investors make informed decisions and maximize their after-tax returns.

In conclusion, investment interest is a fundamental concept in investing, representing the income earned from various investment vehicles. Its compounding nature, the methods of calculation, and the tax implications are all important factors for investors to consider when seeking to grow their wealth and achieve their financial objectives.

Unlocking Financial Growth: The Power of Compound Interest in Investment

You may want to see also

Explore related products

$15.94 $29.99

![]()

Types: There are various types of investment interest, including dividends, capital gains, and interest income from bonds

Dividends are a type of investment interest that represents a portion of a company's profits distributed to its shareholders. They are typically paid quarterly and can be reinvested to purchase additional shares or received as cash. Dividends are often associated with established companies that have a consistent track record of profitability.

Capital gains, on the other hand, are the profits realized from the sale of an investment, such as stocks, bonds, or real estate. They are calculated by subtracting the original purchase price from the selling price. Capital gains can be short-term, if the investment is held for less than a year, or long-term, if it is held for more than a year. Short-term capital gains are typically taxed at a higher rate than long-term gains.

Interest income from bonds is another form of investment interest. Bonds are debt securities issued by governments or corporations to raise capital. When an investor purchases a bond, they are essentially lending money to the issuer. In return, the issuer pays interest on the bond's face value, which is the amount that will be repaid when the bond matures. The interest rate and maturity date are specified at the time the bond is issued.

Each type of investment interest has its own unique characteristics and benefits. Dividends provide a regular income stream and can be a good indicator of a company's financial health. Capital gains offer the potential for higher returns but are more volatile and subject to market fluctuations. Interest income from bonds is generally more stable and predictable but may offer lower returns compared to stocks.

Investors often diversify their portfolios by including a mix of these investment types to balance risk and return. For example, a conservative investor may prefer bonds and dividend-paying stocks, while a more aggressive investor may focus on growth stocks with the potential for higher capital gains.

In conclusion, understanding the different types of investment interest is crucial for building a well-rounded investment strategy. By considering the unique features and risks associated with dividends, capital gains, and interest income from bonds, investors can make informed decisions that align with their financial goals and risk tolerance.

Decoding the Impact: How Interest Rates Shape Investment Strategies

You may want to see also

Explore related products

![]()

Calculation: Investment interest is typically calculated as a percentage of the principal amount invested, using formulas specific to each investment type

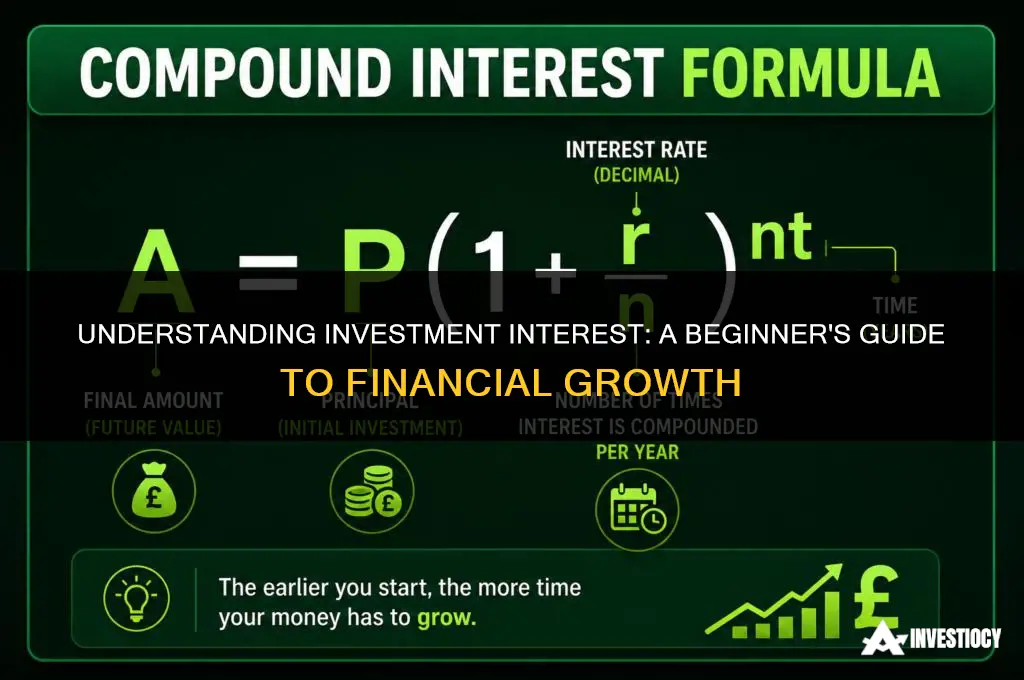

Investment interest calculation is a critical aspect of understanding the returns on your investments. It's typically calculated as a percentage of the principal amount invested, using formulas that are specific to each type of investment. For instance, the interest on a savings account is usually calculated using a simple interest formula, which multiplies the principal amount by the interest rate and the time period the money is invested.

In contrast, investments like bonds and certificates of deposit (CDs) often use a compound interest formula, which calculates interest on both the principal and any accumulated interest. This can significantly increase the total return on investment over time. Stocks and mutual funds, on the other hand, generate returns through capital gains and dividends, which are not typically referred to as 'interest' but are calculated differently.

The frequency of interest calculation also varies by investment type. Some investments, like high-yield savings accounts, calculate interest daily and compound it monthly, while others, like CDs, may compound interest quarterly or annually. Understanding how and when interest is calculated can help you make more informed decisions about where to invest your money.

It's also important to note that the interest rates offered by different financial institutions can vary widely, so it's crucial to shop around and compare rates before making an investment. Additionally, some investments may have penalties for early withdrawal, which can eat into your interest earnings, so it's important to consider the terms and conditions of each investment carefully.

In summary, investment interest is a key factor in determining the return on your investments. By understanding how it's calculated for different types of investments, you can make more informed decisions about where to put your money and maximize your returns.

Smart Investment Strategies for Rising Interest Rate Environments

You may want to see also

Explore related products

![]()

Taxation: In many jurisdictions, investment interest is subject to taxation, with rates varying depending on the type of investment and the investor's tax bracket

Investment interest, while a vital component of financial growth, comes with its own set of tax implications. In many jurisdictions, the interest earned from investments is subject to taxation, with rates varying depending on the type of investment and the investor's tax bracket. This means that understanding the tax landscape is crucial for investors looking to maximize their returns.

For instance, in the United States, interest income is generally taxed as ordinary income, with rates ranging from 10% to 37% depending on the investor's income level. However, there are exceptions and nuances to this rule. For example, interest from municipal bonds is typically exempt from federal income tax, and some types of savings accounts, like 401(k)s and IRAs, offer tax-deferred growth.

Moreover, the tax treatment of investment interest can vary significantly from one country to another. In some countries, like Canada, interest income is taxed at the same rate as other types of income, while in others, like the United Kingdom, there may be allowances or reliefs that reduce the tax burden on interest income.

Investors must also consider the impact of taxes on their investment strategies. For example, they may choose to invest in tax-efficient vehicles like index funds or exchange-traded funds (ETFs), which tend to have lower turnover rates and thus generate less taxable income. Alternatively, they may opt for tax-loss harvesting, a strategy that involves selling investments at a loss to offset taxable gains from other investments.

In conclusion, while investment interest can be a powerful tool for building wealth, it is essential for investors to understand and navigate the complex tax implications associated with it. By doing so, they can make informed decisions that help them achieve their financial goals while minimizing their tax burden.

Smart Investing: How to Live Off Interest and Build Wealth

You may want to see also

Explore related products

![]()

Strategies: Investors may use various strategies to maximize investment interest, such as diversifying their portfolio or reinvesting dividends to compound returns

Investors seeking to maximize their investment interest often employ a range of sophisticated strategies. One such approach is portfolio diversification, which involves spreading investments across various asset classes, sectors, and geographic regions. This tactic helps mitigate risk by reducing exposure to any single market or investment type. For instance, an investor might allocate 60% of their portfolio to stocks, 30% to bonds, and 10% to real estate or commodities. Within each asset class, further diversification can occur by selecting different industries or countries, thereby creating a robust and resilient investment portfolio.

Another effective strategy is the reinvestment of dividends. When companies distribute profits to shareholders in the form of dividends, investors can choose to reinvest these payments into additional shares of the same or other securities. This practice, known as dividend reinvestment, allows investors to compound their returns over time. By continually reinvesting dividends, the total value of the investment grows exponentially, as the dividends themselves earn interest and generate further dividends. This strategy is particularly powerful when combined with a long-term investment horizon, as it can significantly enhance overall returns.

Investors may also consider employing a dollar-cost averaging (DCA) strategy. DCA involves investing a fixed amount of money at regular intervals, regardless of the market's performance. This approach helps smooth out the impact of market volatility and reduces the risk of making large investments at inopportune times. For example, an investor might commit to investing $500 every month in a particular stock or mutual fund. Over time, this consistent investment pattern can lead to a lower average cost per share and improved long-term returns.

Additionally, some investors utilize a strategy known as sector rotation. This involves shifting investments between different sectors of the economy based on market conditions and economic indicators. By identifying sectors that are likely to outperform others, investors can potentially capitalize on emerging trends and opportunities. For instance, during periods of economic growth, sectors such as technology and consumer discretionary goods may perform well, while during downturns, more defensive sectors like healthcare and utilities might be favored.

Finally, investors should not overlook the importance of tax-efficient investing strategies. By structuring their investments in a tax-advantaged manner, investors can minimize their tax liabilities and maximize their after-tax returns. This might involve utilizing tax-deferred retirement accounts, such as 401(k)s or IRAs, or investing in municipal bonds, which are exempt from federal income tax. Additionally, investors can employ strategies like tax-loss harvesting, where they sell securities that have experienced losses to offset gains from other investments, thereby reducing their overall tax burden.

In conclusion, investors have a variety of strategies at their disposal to maximize investment interest. By diversifying their portfolios, reinvesting dividends, employing dollar-cost averaging, engaging in sector rotation, and implementing tax-efficient investing strategies, investors can enhance their returns and achieve their financial goals more effectively.

Navigating Investments: Strategies for a Falling Interest Rate Environment

You may want to see also

Frequently asked questions

Investment interest refers to the income earned from investments, such as stocks, bonds, or mutual funds, in the form of dividends, interest, or capital gains.

Investment interest is calculated based on the principal amount invested, the interest rate or dividend yield, and the time period for which the investment is held. For example, if you invest $1,000 in a stock with a 5% dividend yield, you would earn $50 in investment interest per year.

Yes, investment interest is generally taxable as ordinary income. However, there are some exceptions, such as tax-exempt bonds or investments held in tax-advantaged accounts like IRAs or 401(k)s.

To maximize investment interest, investors can consider strategies such as:

- Investing in high-yield stocks or bonds

- Reinvesting dividends to compound returns

- Diversifying investments to reduce risk and increase potential returns

- Taking advantage of tax-efficient investment vehicles

- Regularly reviewing and adjusting investment portfolios to align with changing market conditions and personal financial goals