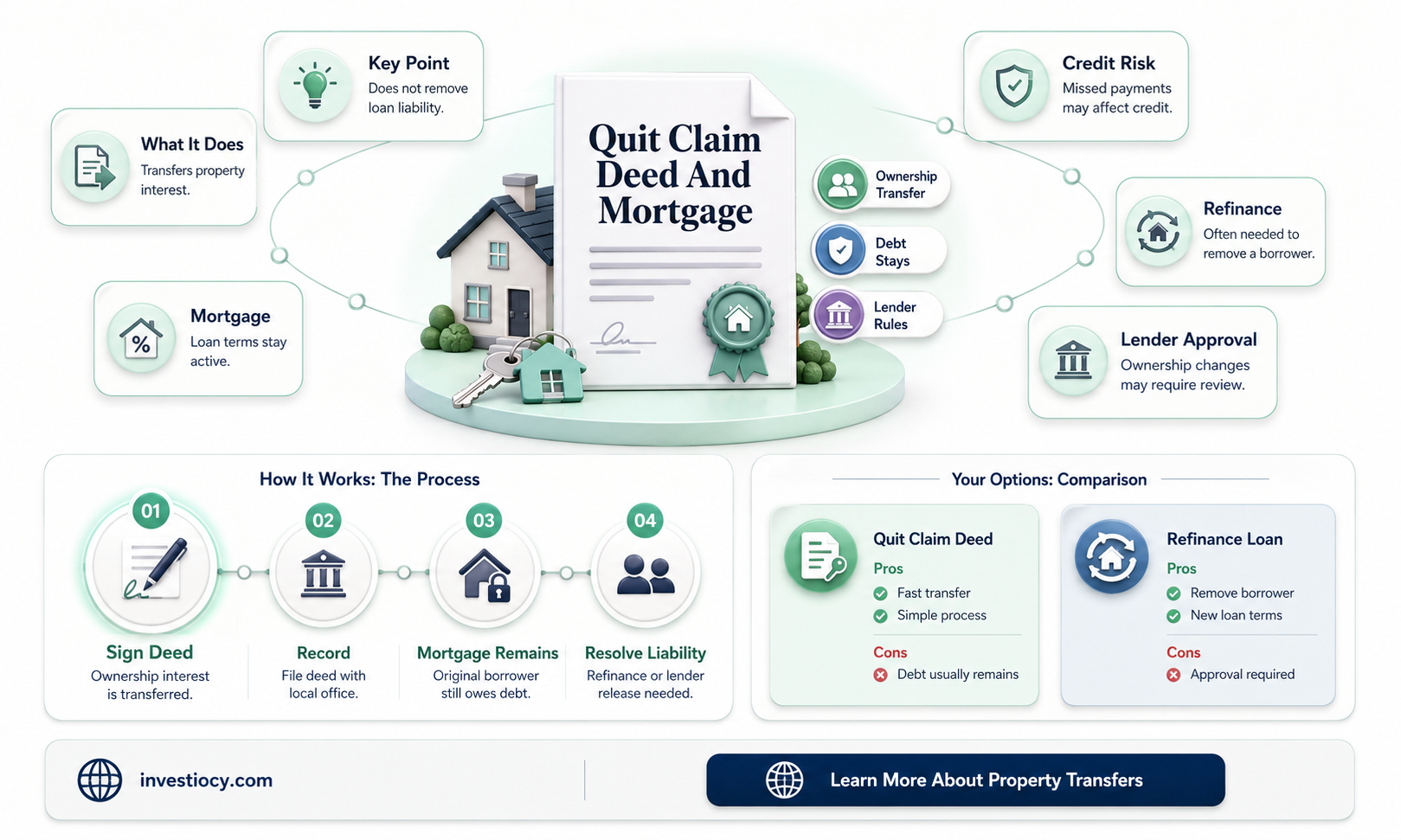

A quitclaim deed is a legal document that transfers ownership of a property from one party to another, often without any warranties or guarantees about the property's title. However, it's important to note that a quitclaim deed does not inherently remove you from the mortgage associated with the property. The mortgage is a separate financial agreement between you and the lender, and transferring ownership through a quitclaim deed does not automatically release you from your obligations under the mortgage. To be removed from the mortgage, you would typically need to refinance the property in the new owner's name or have the lender agree to release you from the mortgage liability. It's crucial to consult with a real estate attorney or financial advisor to understand the specific implications of a quitclaim deed on your mortgage obligations.

| Characteristics | Values |

|---|---|

| Definition | A quitclaim deed is a legal document that transfers ownership of a property from one party to another, without any warranties or guarantees about the property's title. |

| Purpose | The primary purpose of a quitclaim deed is to transfer ownership of a property quickly and easily, often used in situations where a full title search is not necessary or desirable. |

| Mortgage Removal | A quitclaim deed does not inherently remove a person from a mortgage. The mortgage remains in place unless specifically addressed in the deed or through a separate legal process. |

| Liability | By signing a quitclaim deed, the grantor (person transferring ownership) is not liable for any future issues with the property, including any outstanding mortgages or liens. |

| Warranty | Unlike a warranty deed, a quitclaim deed does not provide any guarantees about the property's title, meaning the grantee (person receiving ownership) assumes all risks associated with the property. |

| Common Use | Quitclaim deeds are commonly used in situations such as transferring property between family members, clearing up title issues, or in tax sales. |

| Recording | A quitclaim deed must be recorded with the appropriate government office (usually the county recorder) to be legally valid and to provide public notice of the ownership transfer. |

| Cost | The cost of a quitclaim deed varies by location and complexity, but it is generally less expensive than a warranty deed due to the lack of title guarantees. |

| Timeframe | The process of transferring ownership through a quitclaim deed can be relatively quick, often taking only a few days to a few weeks, depending on the jurisdiction and the parties involved. |

| Legal Advice | It is advisable for both the grantor and grantee to seek legal advice before signing a quitclaim deed to ensure they fully understand the implications and potential risks associated with the transfer. |

Explore related products

What You'll Learn

- Understanding Quit Claim Deeds: A quit claim deed transfers property ownership without guaranteeing the property is free of liens

- Impact on Mortgage Liability: Quit claim deeds do not typically remove you from the mortgage; they only transfer property ownership

- Legal Responsibilities: You may still be liable for the mortgage even after transferring the property with a quit claim deed

- Credit Reporting: A quit claim deed might affect your credit report and score, especially if the mortgage remains unpaid

- Consulting Professionals: It's crucial to consult with a real estate attorney to understand the full implications of using a quit claim deed

![]()

Understanding Quit Claim Deeds: A quit claim deed transfers property ownership without guaranteeing the property is free of liens

A quit claim deed is a legal document that transfers ownership of a property from one party to another. However, it's important to note that this type of deed does not guarantee that the property is free of liens or other encumbrances. This means that if there are any outstanding mortgages, taxes, or other debts associated with the property, the new owner may still be responsible for these obligations.

One common misconception about quit claim deeds is that they remove the previous owner from the mortgage. This is not necessarily the case. While the quit claim deed transfers ownership of the property, it does not automatically remove the previous owner's name from the mortgage. In order to do this, the new owner would need to refinance the mortgage in their own name or work with the lender to assume the existing mortgage.

It's also worth noting that quit claim deeds are often used in situations where there is little or no equity in the property. This is because the seller is essentially giving up any claim to the property without guaranteeing that it is free of liens. As a result, quit claim deeds are often used in short sales, foreclosures, or other situations where the property's value is less than the amount owed on the mortgage.

In summary, while a quit claim deed can be a useful tool for transferring property ownership, it's important to understand its limitations. A quit claim deed does not guarantee that the property is free of liens, and it does not automatically remove the previous owner from the mortgage. If you're considering using a quit claim deed, it's important to consult with a real estate attorney or other qualified professional to ensure that you understand the potential risks and consequences.

Understanding Navy Federal Mortgage Pre-Qualification: Does It Go to Underwriting?

You may want to see also

Explore related products

![]()

Impact on Mortgage Liability: Quit claim deeds do not typically remove you from the mortgage; they only transfer property ownership

A quit claim deed is a legal document that transfers ownership of a property from one party to another. However, it's important to note that this type of deed does not typically remove the original owner from the mortgage liability. In other words, even though the property ownership has been transferred, the original owner may still be responsible for the mortgage payments.

This can have significant implications for both the buyer and the seller. For the buyer, it means that they may not be able to obtain financing for the property if the seller is not removed from the mortgage. For the seller, it means that they may be at risk of defaulting on the mortgage if the buyer fails to make payments.

There are some exceptions to this rule, such as when the lender agrees to release the original owner from the mortgage liability. However, this is not always the case, and it's important to check with the lender before entering into a quit claim deed agreement.

In some cases, a quit claim deed may be used as part of a short sale or a foreclosure prevention strategy. In these situations, the original owner may be willing to transfer ownership of the property to a buyer in exchange for a reduced payoff on the mortgage. However, this can have tax implications for both parties, and it's important to consult with a tax professional before entering into such an agreement.

Overall, it's important to understand the implications of a quit claim deed on mortgage liability before entering into any agreements. While this type of deed can be a useful tool for transferring property ownership, it's important to be aware of the potential risks and responsibilities involved.

Exploring Property Mortgages: A Comprehensive Guide for Homebuyers

You may want to see also

Explore related products

![]()

Legal Responsibilities: You may still be liable for the mortgage even after transferring the property with a quit claim deed

A quit claim deed is a legal document that transfers ownership of a property from one party to another. However, it's a common misconception that signing a quit claim deed automatically removes you from the mortgage liability. In reality, the legal responsibilities associated with the mortgage can persist even after the property has been transferred.

The primary reason for this is that a quit claim deed only transfers the title of the property, not the mortgage itself. The mortgage is a separate legal obligation that is tied to the property, not the owner. Therefore, unless the mortgage is specifically addressed in the quit claim deed or through a separate legal process, the original mortgagor (the person who took out the mortgage) remains liable for the debt.

This can have significant implications for individuals who are looking to transfer property while avoiding mortgage responsibilities. For instance, if the new owner defaults on the mortgage payments, the original mortgagor could be held responsible for the outstanding debt. This is why it's crucial to understand the legal ramifications of a quit claim deed and to consult with a legal professional before entering into such an agreement.

In some cases, it may be possible to negotiate with the lender to have the mortgage transferred to the new owner. This process, known as a mortgage assumption, requires the new owner to qualify for the mortgage and the lender to agree to the transfer. If successful, this can effectively remove the original mortgagor from the mortgage liability.

However, mortgage assumptions can be complex and are not always possible. Lenders may have specific requirements and restrictions, and the process can be time-consuming and costly. Therefore, it's important to carefully consider all options and to seek professional advice before making any decisions regarding property transfers and mortgage liabilities.

Understanding Mortgage Notes: The Role of a Notary Public Explained

You may want to see also

Explore related products

![Transfer on Death Deed Form: TOD Document with Step-by-Step Instructions, Legal Guide, and Customizable Fields | Valid in [Your State] | 60 Forms.](https://m.media-amazon.com/images/I/61thFMUgn8L._AC_UL320_.jpg)

![]()

Credit Reporting: A quit claim deed might affect your credit report and score, especially if the mortgage remains unpaid

A quit claim deed can have significant implications for your credit report and score, particularly if the mortgage associated with the property remains unpaid. This is because a quit claim deed transfers ownership of the property without necessarily relieving the original owner of their financial obligations. As a result, if the mortgage payments are not made, the lender may report the delinquency to the credit bureaus, which can negatively impact the credit score of the individual who executed the quit claim deed.

It's important to note that the impact on your credit report and score will depend on the specific circumstances surrounding the quit claim deed. For instance, if the mortgage is current and the quit claim deed is executed as part of a divorce settlement or other legal arrangement, there may be no negative impact on your credit. However, if the mortgage is in arrears or the quit claim deed is executed in an attempt to avoid foreclosure, it is likely that your credit report and score will be affected.

In some cases, a quit claim deed can actually improve your credit score if it results in the removal of a delinquent account from your credit report. This can happen if the new owner of the property assumes responsibility for the mortgage and makes timely payments, thereby improving the overall creditworthiness of the account. However, this is not always the case, and it's important to carefully consider the potential consequences of executing a quit claim deed before making a decision.

If you're considering executing a quit claim deed, it's essential to consult with a qualified attorney or financial advisor who can help you understand the potential impact on your credit report and score. They can also provide guidance on alternative options that may be available to you, such as a short sale or a loan modification, which could have different implications for your credit.

In conclusion, while a quit claim deed can be a useful tool for transferring ownership of a property, it's important to be aware of the potential impact on your credit report and score, especially if the mortgage remains unpaid. By carefully considering the circumstances surrounding the quit claim deed and seeking professional advice, you can make an informed decision that minimizes any negative consequences for your credit.

Understanding Multiple Indebtedness Mortgages: Maturity Insights

You may want to see also

Explore related products

$8.99

![]()

Consulting Professionals: It's crucial to consult with a real estate attorney to understand the full implications of using a quit claim deed

Consulting with a real estate attorney is essential when considering the use of a quit claim deed. This legal document has significant implications that can affect your financial and legal standing, particularly in relation to a mortgage. A quit claim deed is a formal document that transfers ownership of a property from one party to another, but it does not guarantee that the property is free of liens or mortgages. Therefore, it is crucial to seek professional advice to fully understand the consequences of using this type of deed.

One of the primary reasons to consult an attorney is to ensure that you are aware of all the potential risks and liabilities associated with a quit claim deed. For instance, if you are transferring property with an existing mortgage, the quit claim deed may not remove your name from the mortgage, leaving you responsible for the debt. An attorney can review the specific details of your situation and advise you on the best course of action to protect your interests.

Additionally, a real estate attorney can help you navigate the complex legal process involved in transferring property. They can assist with drafting the quit claim deed, ensuring that it is properly executed and recorded, and addressing any issues that may arise during the transfer. This can include negotiating with lenders, resolving disputes, and complying with local laws and regulations.

Furthermore, consulting an attorney can provide you with valuable insights into alternative options that may be more suitable for your situation. For example, if you are looking to transfer property while avoiding the risks associated with a quit claim deed, an attorney may recommend using a warranty deed or exploring other legal avenues.

In conclusion, seeking professional advice from a real estate attorney is a critical step when considering the use of a quit claim deed. They can help you understand the full implications of this legal document, guide you through the transfer process, and offer alternative solutions to protect your financial and legal interests.

Navigating Bankruptcy: Can You Wipe Out Mortgage Debt?

You may want to see also

Frequently asked questions

A quit claim deed transfers your ownership interest in the property to another party, but it does not remove you from the mortgage. You remain liable for the mortgage payments unless the lender agrees to release you from the loan.

The primary purpose of a quit claim deed is to transfer ownership of a property from one party to another, often without any warranties or guarantees about the property's title. It is commonly used in situations where the property is being given as a gift or transferred between family members.

A quit claim deed itself does not directly affect your credit score. However, if you are transferring the property to someone else and they are assuming the mortgage, your credit score may be impacted by the change in your debt-to-income ratio and the removal of the mortgage from your credit report.

One potential risk of using a quit claim deed is that it transfers ownership of the property without any warranties or guarantees about the property's title. This means that the new owner may be unaware of any existing liens, encumbrances, or defects in the title, which could lead to legal issues or financial losses. Additionally, if the property is transferred to someone else and they are assuming the mortgage, you may still be liable for the mortgage payments if the new owner defaults on the loan.