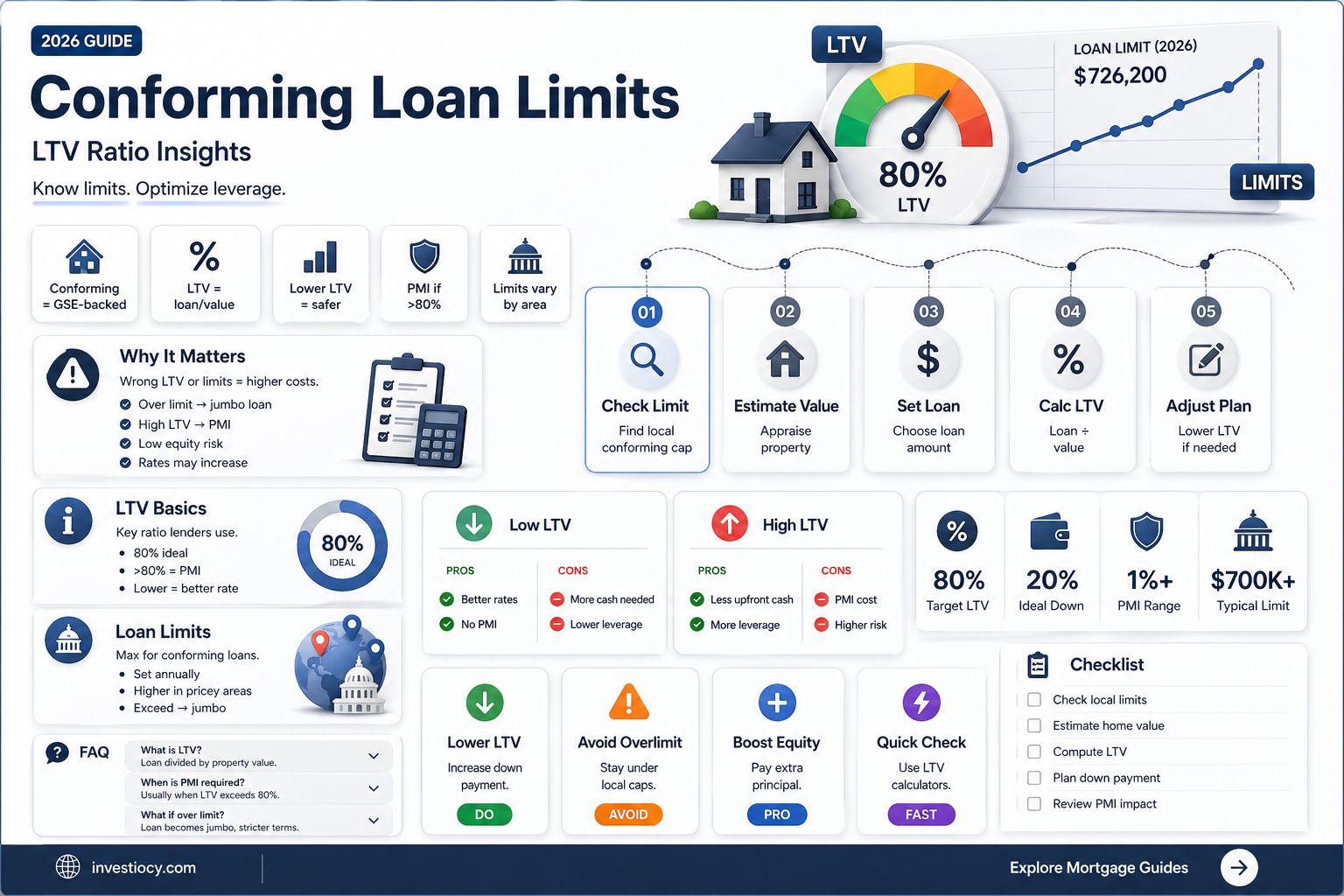

Conforming loan limits do indeed vary by loan-to-value (LTV) ratio. The LTV ratio is a critical factor in determining the amount of mortgage a borrower can obtain. It is calculated by dividing the loan amount by the property's purchase price or appraised value, whichever is lower. For instance, if a property is valued at $500,000 and the borrower seeks a loan of $400,000, the LTV ratio would be 80%. Conforming loans, which adhere to the guidelines set by Fannie Mae and Freddie Mac, typically have different limits for different LTV ratios. Borrowers with lower LTV ratios often have access to higher loan limits because they represent less risk to lenders. Conversely, higher LTV ratios usually correspond to lower loan limits due to the increased risk associated with lending a larger proportion of the property's value.

Explore related products

What You'll Learn

- Definition of Conforming Loans: Conforming loans adhere to specific guidelines set by government-sponsored enterprises like Fannie Mae and Freddie Mac

- LTV Ratio Explained: Loan-to-Value (LTV) ratio compares the loan amount to the property's purchase price or appraised value

- Conforming Loan Limits: These limits vary by county and are adjusted annually based on home price changes

- Impact of LTV on Loan Limits: Higher LTV ratios may reduce the conforming loan limit available to a borrower

- Exceptions and Variations: Certain circumstances, like multi-unit properties or high-cost areas, may have different conforming loan limit rules

![]()

Definition of Conforming Loans: Conforming loans adhere to specific guidelines set by government-sponsored enterprises like Fannie Mae and Freddie Mac

Conforming loans are mortgages that meet the specific underwriting guidelines set by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. These guidelines dictate various aspects of the loan, including the maximum loan amount, which is commonly referred to as the conforming loan limit. This limit is adjusted annually based on changes in the housing market and is designed to ensure that the loans are manageable and sustainable for both lenders and borrowers.

One of the key factors that influence the conforming loan limit is the loan-to-value (LTV) ratio. The LTV ratio is a measure of the loan amount relative to the value of the property being purchased. For example, if a borrower is purchasing a home valued at $500,000 and is seeking a loan of $400,000, the LTV ratio would be 80%. Conforming loans typically have lower LTV ratios compared to other types of loans, such as FHA or VA loans, which can offer higher LTV ratios to borrowers with lower credit scores or other mitigating factors.

The conforming loan limit does indeed vary by LTV ratio, with higher LTV ratios generally corresponding to lower loan limits. This is because higher LTV ratios represent a greater risk to lenders, as the borrower has less equity in the property. To mitigate this risk, lenders often require borrowers with higher LTV ratios to pay higher interest rates or to purchase mortgage insurance, which can increase the overall cost of the loan.

In addition to the LTV ratio, other factors that can influence the conforming loan limit include the borrower's credit score, income, and debt-to-income ratio. Borrowers with higher credit scores and lower debt-to-income ratios are typically eligible for higher loan limits, as they represent a lower risk to lenders. Furthermore, the conforming loan limit can also vary depending on the type of property being purchased, with higher limits often available for multi-unit properties or homes located in high-cost areas.

Overall, the conforming loan limit is a critical aspect of the mortgage underwriting process, as it helps to ensure that loans are made in a responsible and sustainable manner. By adhering to the guidelines set by Fannie Mae and Freddie Mac, lenders can offer borrowers competitive interest rates and terms while minimizing the risk of default.

Explore related products

![]()

LTV Ratio Explained: Loan-to-Value (LTV) ratio compares the loan amount to the property's purchase price or appraised value

The Loan-to-Value (LTV) ratio is a critical metric in the world of mortgage lending. It compares the amount of the loan to the property's purchase price or appraised value. This ratio helps lenders assess the risk associated with a mortgage loan. A higher LTV ratio indicates a higher risk for the lender, as the borrower has less equity in the property. Conversely, a lower LTV ratio suggests a lower risk, as the borrower has more equity.

When it comes to conforming loans, which are loans that meet the guidelines set by Fannie Mae and Freddie Mac, the LTV ratio plays a significant role. Conforming loans typically have a maximum LTV ratio of 97%, meaning that the loan amount can be up to 97% of the property's purchase price or appraised value. However, this limit can vary depending on the specific loan program and the borrower's creditworthiness.

For instance, some conforming loan programs may offer higher LTV ratios for certain types of borrowers, such as first-time homebuyers or those with excellent credit scores. Additionally, the LTV ratio may be lower for investment properties or second homes. It's important to note that while the LTV ratio is a key factor in determining the conforming loan limit, it is not the only factor. Other considerations, such as the borrower's income, debt-to-income ratio, and credit history, also play a crucial role.

In conclusion, the LTV ratio is a vital component in the mortgage lending process, particularly for conforming loans. It helps lenders evaluate the risk associated with a loan and determine the maximum loan amount. While the conforming loan limit can vary based on the LTV ratio, it is also influenced by other factors related to the borrower's financial situation and the property being purchased.

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)

![]()

Conforming Loan Limits: These limits vary by county and are adjusted annually based on home price changes

Conforming loan limits are a critical aspect of mortgage financing, dictating the maximum loan amount a lender can offer for a property purchase. These limits are not static; they vary significantly by county and are subject to annual adjustments based on fluctuations in home prices. This dynamic nature ensures that loan limits remain aligned with the current market conditions, providing borrowers with access to financing that reflects the true value of the property.

The variation in conforming loan limits by county is due to the diverse housing markets across the United States. In high-cost areas, such as California or New York, loan limits are higher to accommodate the elevated home prices. Conversely, in more affordable regions, the loan limits are lower. This geographical disparity allows lenders to offer financing that is tailored to the specific needs of each local market, ensuring that borrowers can access the funds necessary to purchase a home.

Annual adjustments to conforming loan limits are based on data from the Federal Housing Finance Agency (FHFA), which tracks changes in home prices nationwide. If home prices increase, the loan limits are raised to reflect the higher property values. This adjustment is crucial for maintaining the accessibility of mortgage financing, as it prevents borrowers from being priced out of the market due to rising home costs.

For borrowers, understanding the conforming loan limits in their specific county is essential for planning their home purchase. It allows them to determine the maximum loan amount they can qualify for and helps them set a realistic budget for their new home. Additionally, being aware of the annual adjustments can aid borrowers in making informed decisions about when to enter the housing market, as changes in loan limits can impact their purchasing power.

In conclusion, conforming loan limits play a vital role in the mortgage financing process, providing a framework for lenders to offer loans that are commensurate with the value of the property. The variation in limits by county and the annual adjustments based on home price changes ensure that the financing options remain relevant and accessible to borrowers in diverse housing markets.

Explore related products

![]()

Impact of LTV on Loan Limits: Higher LTV ratios may reduce the conforming loan limit available to a borrower

The Loan-to-Value (LTV) ratio is a critical factor in determining the conforming loan limit for a borrower. A higher LTV ratio indicates that the borrower is seeking a loan amount that is closer to the value of the property being purchased. This can reduce the conforming loan limit available to the borrower, as lenders may perceive a higher LTV ratio as a greater risk.

For instance, if a borrower is purchasing a property valued at $500,000 and is seeking a loan amount of $400,000, their LTV ratio would be 80%. In this scenario, the borrower may be eligible for a conforming loan limit of up to $400,000. However, if the borrower increases their loan amount to $450,000, their LTV ratio would rise to 90%, and their conforming loan limit may be reduced to $400,000 or less.

This reduction in conforming loan limit is a result of the increased risk associated with higher LTV ratios. Lenders are more likely to approve loans with lower LTV ratios, as they represent a lower risk of default. Therefore, borrowers with higher LTV ratios may need to consider alternative loan options, such as jumbo loans, which are not subject to the same conforming loan limit restrictions.

It is essential for borrowers to understand the impact of LTV ratios on conforming loan limits when planning their home purchase. By carefully managing their LTV ratio, borrowers can maximize their chances of securing a conforming loan with favorable terms. This may involve making a larger down payment, selecting a property with a lower purchase price, or exploring alternative loan options that better suit their financial situation.

In conclusion, the impact of LTV on loan limits is a crucial consideration for borrowers seeking a conforming loan. Higher LTV ratios can reduce the conforming loan limit available, making it essential for borrowers to carefully manage their LTV ratio and explore alternative loan options if necessary. By doing so, borrowers can increase their chances of securing a loan that meets their financial needs and goals.

Explore related products

![]()

Exceptions and Variations: Certain circumstances, like multi-unit properties or high-cost areas, may have different conforming loan limit rules

In the realm of mortgage financing, conforming loan limits are not always as straightforward as they may seem. While the general conforming loan limit applies to most single-family homes, there are notable exceptions and variations that borrowers should be aware of. One such exception is multi-unit properties, which often have higher conforming loan limits compared to single-family homes. This is because multi-unit properties can generate more income through rental, thus justifying a higher loan amount.

Another significant variation is in high-cost areas, where the conforming loan limit can be substantially higher than in other regions. This is to accommodate the elevated property values typically found in these areas. For instance, in certain metropolitan areas like San Francisco or New York City, the conforming loan limit may be increased to reflect the higher cost of living and housing prices.

It's also important to note that conforming loan limits can vary by loan type. For example, FHA loans and VA loans may have different conforming loan limits compared to conventional loans. Additionally, some lenders may offer non-conforming loans, also known as jumbo loans, which exceed the conforming loan limits set by Fannie Mae and Freddie Mac.

Borrowers should also be mindful of the loan-to-value (LTV) ratio, which is the percentage of the property's value that the loan amount represents. While the conforming loan limit does not directly vary by LTV, a higher LTV ratio may require a higher credit score or more stringent underwriting criteria to qualify for a conforming loan.

In conclusion, understanding the exceptions and variations to conforming loan limits is crucial for borrowers looking to secure a mortgage. By being aware of these nuances, borrowers can better navigate the mortgage application process and find a loan that best suits their needs.

Frequently asked questions

No, the conforming loan limit does not vary by LTV ratio. It is a fixed amount set annually by Fannie Mae and Freddie Mac, which in 2023 is $726,200 for most areas in the United States.

The conforming loan limit is significant because it determines the maximum loan amount that Fannie Mae and Freddie Mac can purchase or guarantee. Loans below this limit are considered conforming loans and typically have lower interest rates and more favorable terms.

The LTV ratio impacts mortgage loans by determining the amount of equity a borrower has in the property. A lower LTV ratio means the borrower has more equity, which can result in better loan terms, such as lower interest rates and lower mortgage insurance premiums.

If a loan exceeds the conforming loan limit, it is considered a jumbo loan. Jumbo loans typically have higher interest rates and stricter underwriting guidelines than conforming loans. Borrowers may also be required to make a larger down payment.

Yes, there are exceptions to the conforming loan limit. For example, in high-cost areas, the conforming loan limit may be higher. Additionally, there are conforming high-balance loans, which allow for loan amounts up to $1,089,300 in certain areas.

![NMLS Study Guide 2026–2027: 10 Full-Length Practice Tests for the SAFE Mortgage Loan Originator (MLO) Exam Prep: [3rd Edition]](https://m.media-amazon.com/images/I/61s4wNIlEcL._AC_UL320_.jpg)