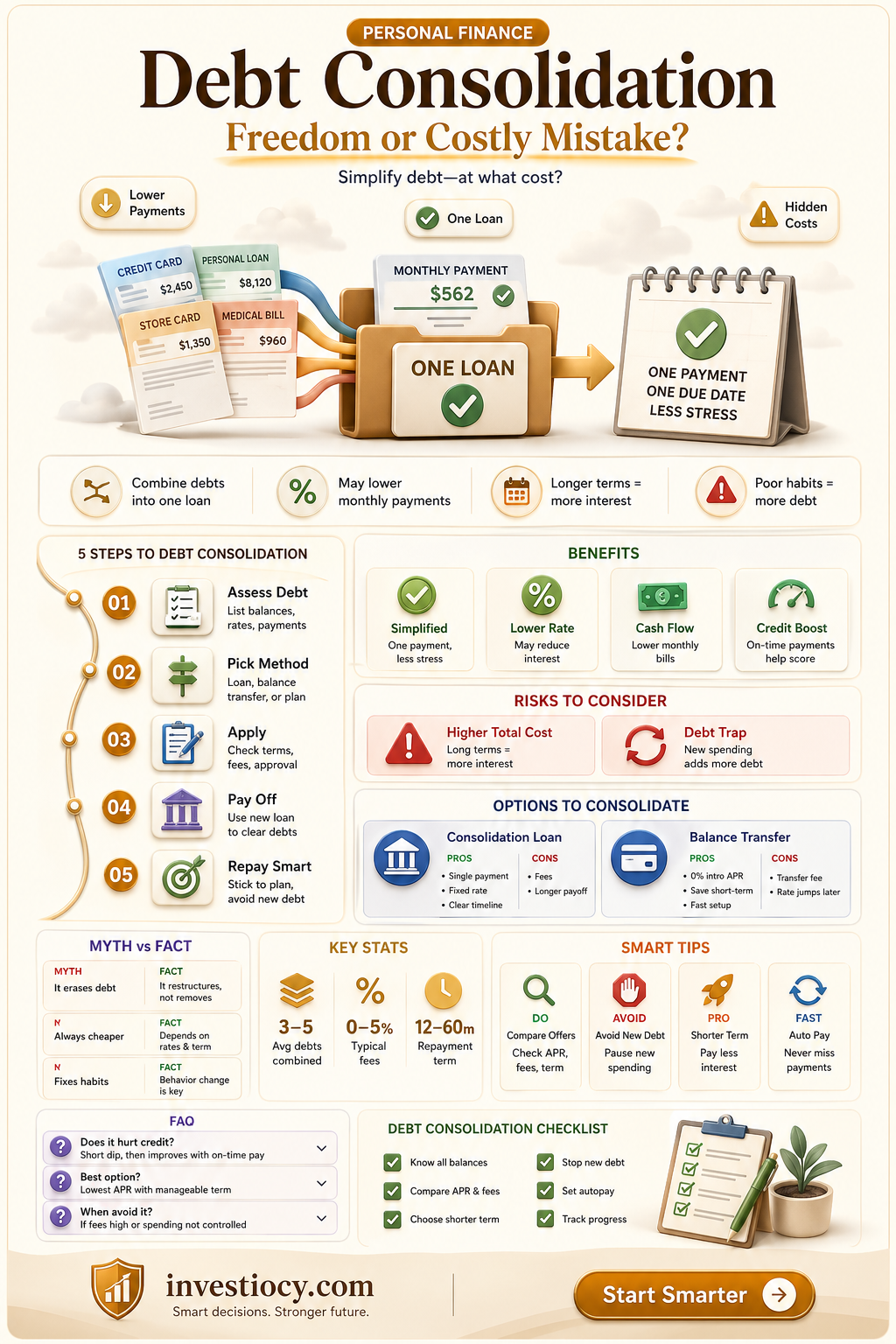

Consolidating loans can be a helpful strategy for managing multiple debts. It involves combining several loans into a single loan, often with a lower interest rate and a longer repayment term. This can simplify the repayment process, reduce the total monthly payment, and potentially save money on interest over time. However, it's important to consider the specific circumstances and types of loans involved, as consolidation may not always be the best option. For instance, consolidating federal student loans could result in the loss of certain benefits and protections. It's crucial to weigh the pros and cons and consult with a financial advisor before making a decision.

Explore related products

What You'll Learn

- Simplifies Finances: Consolidating loans can streamline multiple payments into one, making financial management easier and less overwhelming

- Potential Cost Savings: By securing a lower interest rate, loan consolidation can reduce the total cost of borrowing over time

- Credit Score Impact: Consolidation may initially lower credit scores due to new credit inquiries and changes in credit utilization ratios

- Risk of Over-Borrowing: Consolidating loans can free up credit limits, which may tempt individuals to accumulate more debt if not managed responsibly

- Loss of Benefits: Some loans, like federal student loans, offer specific benefits that may be lost when consolidated into a private loan

![]()

Simplifies Finances: Consolidating loans can streamline multiple payments into one, making financial management easier and less overwhelming

Consolidating loans can significantly simplify financial management by reducing the number of payments one needs to keep track of each month. This process involves combining multiple debts into a single loan, which can make it easier to budget and plan for repayments. For individuals juggling several high-interest loans or credit card debts, consolidation can provide a clear path forward, reducing the likelihood of missed payments and late fees.

One of the primary benefits of loan consolidation is the potential for a lower monthly payment. By extending the repayment term or securing a lower interest rate, borrowers can reduce their monthly financial burden. This can be particularly helpful for those who are struggling to make ends meet or who have experienced a reduction in income. Additionally, consolidating loans can improve one's credit score over time, as making consistent, on-time payments demonstrates financial responsibility to credit reporting agencies.

However, it's important to approach loan consolidation with caution. While it can simplify finances, it may also lead to a longer repayment period, potentially resulting in more interest paid over the life of the loan. Borrowers should carefully consider the terms and conditions of any consolidation loan, ensuring that it aligns with their long-term financial goals. It's also crucial to address the underlying spending habits that led to the initial debt accumulation, as consolidation alone will not prevent future financial challenges.

In conclusion, consolidating loans can be a valuable tool for simplifying financial management and reducing monthly payments. However, it's essential to weigh the potential benefits against the drawbacks and to develop a comprehensive plan for achieving financial stability. By doing so, individuals can make informed decisions about whether loan consolidation is the right strategy for their unique financial situation.

Simplify Your Finances: The Truth About Loan Consolidation Costs

You may want to see also

Explore related products

![]()

Potential Cost Savings: By securing a lower interest rate, loan consolidation can reduce the total cost of borrowing over time

Securing a lower interest rate through loan consolidation can significantly reduce the total cost of borrowing over time. This is because the interest rate directly impacts the amount of money paid in interest over the life of the loan. By consolidating loans into a single loan with a lower interest rate, borrowers can save money on interest charges, which can add up to substantial savings over time.

For example, consider a borrower with two loans: one with a balance of $10,000 at an interest rate of 8% and another with a balance of $5,000 at an interest rate of 12%. By consolidating these loans into a single loan with a balance of $15,000 at an interest rate of 6%, the borrower can save money on interest charges. Over a 5-year repayment period, the borrower would pay $4,000 in interest on the consolidated loan, compared to $6,000 in interest on the original loans. This represents a savings of $2,000 over the life of the loan.

In addition to saving money on interest charges, loan consolidation can also simplify the repayment process. By consolidating multiple loans into a single loan, borrowers only need to make one monthly payment, which can make it easier to manage their finances and avoid missed payments. This can also help improve their credit score, as missed payments can negatively impact credit scores.

However, it's important to note that loan consolidation may not always be the best option. Borrowers should carefully consider the terms and conditions of the consolidated loan, including the interest rate, repayment period, and any fees associated with the consolidation process. They should also consider their financial situation and goals, and determine whether loan consolidation aligns with their overall financial strategy.

In conclusion, securing a lower interest rate through loan consolidation can lead to significant cost savings over time. By reducing the amount of money paid in interest, borrowers can save money and simplify their repayment process. However, it's important to carefully consider the terms and conditions of the consolidated loan and determine whether loan consolidation is the best option for their financial situation.

Understanding Conforming Loan Limits: LTV Ratio Insights

You may want to see also

Explore related products

![]()

Credit Score Impact: Consolidation may initially lower credit scores due to new credit inquiries and changes in credit utilization ratios

Consolidating loans can have a significant impact on an individual's credit score, particularly in the short term. When a person applies for a new loan to consolidate their existing debts, the lender will conduct a hard credit inquiry to assess their creditworthiness. This inquiry can result in a temporary drop in the individual's credit score, typically ranging from 5 to 10 points. Additionally, the changes in credit utilization ratios that occur when consolidating loans can also affect credit scores.

Credit utilization ratios are calculated by dividing the total amount of debt a person owes by their total available credit. When consolidating loans, an individual may close some of their existing credit accounts, which can reduce their overall available credit. This reduction in available credit can lead to an increase in credit utilization ratios, even if the person's total debt remains the same. Higher credit utilization ratios are often associated with higher credit risk, which can result in a lower credit score.

However, it's important to note that the impact of consolidation on credit scores is typically short-lived. Over time, as the individual makes regular payments on their consolidated loan and demonstrates responsible credit behavior, their credit score can recover and even improve. In fact, consolidating loans can sometimes lead to a more manageable debt repayment plan, which can help individuals avoid late payments and other negative credit behaviors that can harm their credit scores.

To minimize the potential negative impact of consolidation on credit scores, individuals should consider several factors before applying for a consolidation loan. These factors include the interest rate and terms of the new loan, the fees associated with consolidating, and the potential impact on their credit utilization ratios. By carefully weighing these factors and choosing a consolidation option that aligns with their financial goals and credit profile, individuals can mitigate the short-term effects of consolidation on their credit scores and set themselves up for long-term financial success.

![]()

Risk of Over-Borrowing: Consolidating loans can free up credit limits, which may tempt individuals to accumulate more debt if not managed responsibly

Consolidating loans can indeed help individuals manage their debt more effectively by combining multiple payments into one, often with a lower interest rate. However, this financial strategy comes with a caveat: it can free up credit limits, which may tempt individuals to accumulate more debt if not managed responsibly. This risk of over-borrowing is a significant concern, as it can lead to a vicious cycle of debt that is difficult to escape.

When individuals consolidate their loans, they often see an immediate improvement in their credit score due to the reduction in the number of outstanding debts. This, in turn, can lead to an increase in their credit limit, as lenders view them as less of a risk. While this can be beneficial for those who need to make large purchases or investments, it can also be a slippery slope for those who are not disciplined in their spending habits.

To mitigate the risk of over-borrowing, it is essential for individuals to have a solid understanding of their financial situation and to develop a budget that they can stick to. This includes setting realistic goals for debt repayment and avoiding unnecessary expenses. Additionally, it is crucial to monitor credit limits and to avoid maxing out credit cards, as this can lead to a decrease in credit score and an increase in interest rates.

Individuals who are considering consolidating their loans should also be aware of the potential impact on their credit utilization ratio. This ratio, which is calculated by dividing the total amount of debt by the total credit limit, is a key factor in determining credit score. While consolidating loans can help to reduce the number of outstanding debts, it can also lead to an increase in the credit utilization ratio if the individual continues to accumulate debt.

In conclusion, while consolidating loans can be a helpful financial strategy, it is important to be aware of the potential risks associated with over-borrowing. By developing a solid financial plan, monitoring credit limits, and avoiding unnecessary expenses, individuals can minimize these risks and use loan consolidation as a tool to achieve financial stability.

![]()

Loss of Benefits: Some loans, like federal student loans, offer specific benefits that may be lost when consolidated into a private loan

Consolidating loans can often be a strategic financial move, but it's crucial to understand the potential downsides, particularly when it comes to federal student loans. These loans come with a range of benefits that may be forfeited if consolidated into a private loan. For instance, federal student loans offer income-driven repayment plans, which can significantly lower monthly payments for those with lower incomes. Additionally, they provide loan forgiveness options after a certain number of years of repayment, a benefit that is rarely available with private loans.

Another key benefit of federal student loans is the fixed interest rate, which remains constant over the life of the loan. This predictability can be advantageous for budgeting and long-term financial planning. In contrast, private loans often have variable interest rates, which can fluctuate based on market conditions, potentially increasing the total cost of the loan over time.

Furthermore, federal student loans offer deferment and forbearance options, allowing borrowers to temporarily postpone or reduce their payments if they are experiencing financial hardship. Private loans typically do not offer these same protections, which can make managing financial difficulties more challenging.

It's also important to consider the loss of federal loan benefits such as the Public Service Loan Forgiveness (PSLF) program, which forgives the remaining balance of federal student loans for those who work in public service and make qualifying payments. Consolidating into a private loan would eliminate eligibility for this program.

In summary, while consolidating loans can have its advantages, such as simplifying repayment and potentially securing a lower interest rate, it's essential to weigh these benefits against the potential loss of federal loan benefits. Borrowers should carefully consider their individual financial situation and long-term goals before deciding to consolidate federal student loans into a private loan.

Frequently asked questions

Consolidating loans can potentially help improve credit scores by simplifying debt management and reducing the likelihood of missed payments. However, it's essential to make consistent, on-time payments on the consolidated loan to see a positive impact on credit scores.

Consolidating loans does not reduce the total amount of debt owed; it merely combines multiple debts into a single loan with a single monthly payment. The total debt remains the same, but managing it becomes more streamlined.

Consolidating loans may lower interest rates, especially if the borrower has good credit and qualifies for a lower rate than what they were previously paying on their individual debts. This can lead to savings on interest charges over the life of the loan.

Consolidating loans generally does not directly affect employment or income. However, if a borrower's debt-to-income ratio is significantly reduced through consolidation, it may improve their overall financial stability and make them a more attractive candidate for certain job opportunities or loans in the future.