Consolidating private loans does not inherently forfeit federal loans, but it's crucial to understand the nuances involved. When individuals consolidate their student loans, they essentially combine multiple loans into a single loan with a new interest rate and repayment terms. This process can include both federal and private loans, but federal loans often come with specific protections and benefits that may be lost if consolidated with private loans. For instance, federal loans typically offer income-driven repayment plans, loan forgiveness options, and deferment or forbearance programs that private loans may not provide. Therefore, while consolidating private loans doesn't automatically forfeit federal loans, borrowers should carefully consider the potential loss of federal loan benefits before proceeding with consolidation.

Explore related products

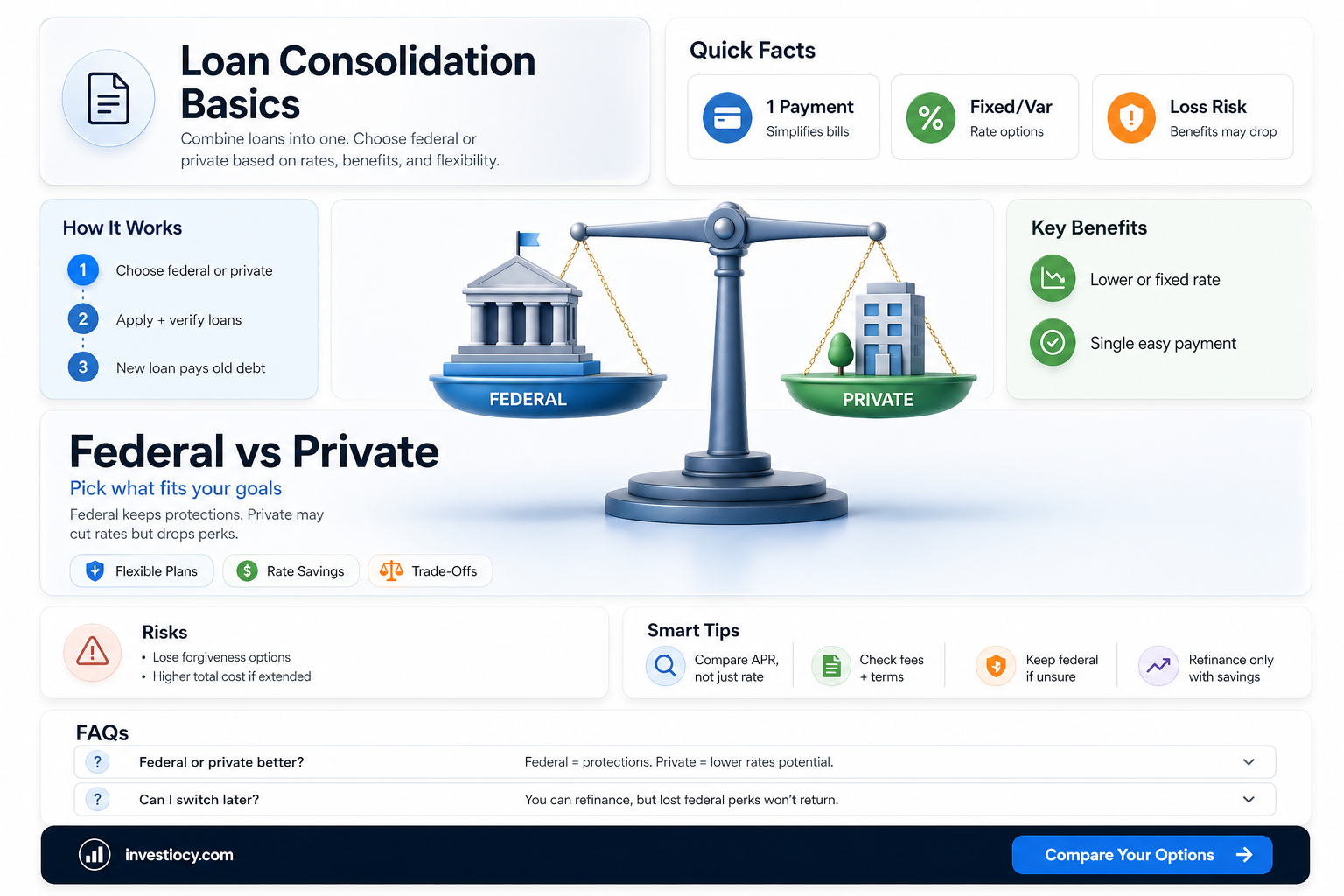

What You'll Learn

- Impact on Federal Loan Benefits: Consolidating private loans may affect eligibility for federal loan benefits

- Interest Rates: Private loan consolidation could result in higher interest rates compared to federal loans

- Repayment Terms: Terms of repayment might become less favorable when consolidating private loans

- Credit Score: The process could potentially impact the borrower's credit score

- Legal and Financial Implications: There may be significant legal and financial consequences to consider

![]()

Impact on Federal Loan Benefits: Consolidating private loans may affect eligibility for federal loan benefits

Consolidating private loans can have significant implications for borrowers who are also managing federal student loans. One of the primary concerns is the potential impact on federal loan benefits. Federal student loans often come with various benefits, such as income-driven repayment plans, loan forgiveness programs, and deferment options. However, when private loans are consolidated, it may affect the borrower's eligibility for these federal benefits.

For instance, if a borrower consolidates their private loans into a single private loan, they may lose the ability to apply for federal loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness. This is because these programs are specifically designed for federal student loans and do not apply to private loans. Additionally, consolidating private loans may also affect the borrower's ability to qualify for income-driven repayment plans, which are based on the borrower's income and family size.

Furthermore, consolidating private loans can also impact the borrower's credit score, which in turn may affect their eligibility for federal loan benefits. A lower credit score may result in higher interest rates on federal loans, reducing the overall benefits of consolidation. It is essential for borrowers to carefully consider these factors before deciding to consolidate their private loans.

In some cases, borrowers may be able to maintain their federal loan benefits by consolidating their private loans into a federal Direct Consolidation Loan. This type of consolidation allows borrowers to combine their federal and private loans into a single federal loan, which may preserve their eligibility for federal benefits. However, it is crucial to note that not all private loans are eligible for inclusion in a federal Direct Consolidation Loan, and borrowers should consult with a financial aid advisor to determine their options.

Ultimately, the decision to consolidate private loans should be made after carefully weighing the potential impact on federal loan benefits. Borrowers should consider their long-term financial goals, their current loan situation, and their eligibility for federal benefits before making a decision. By doing so, they can ensure that they are making the best choice for their financial future.

Understanding Conforming Loan Limits: LTV Ratio Insights

You may want to see also

Explore related products

![]()

Interest Rates: Private loan consolidation could result in higher interest rates compared to federal loans

Consolidating private loans can indeed lead to higher interest rates compared to federal loans. This is because private lenders often charge higher rates to compensate for the higher risk they take on when lending to students. Federal loans, on the other hand, are backed by the government, which means they can offer lower interest rates.

One unique angle to consider is the potential impact of refinancing private loans on the overall cost of borrowing. While refinancing can sometimes lower your monthly payments, it may also extend the repayment term, which could result in paying more interest over the life of the loan. This is especially true if you refinance at a higher interest rate.

Another important factor to consider is the loss of federal loan benefits when consolidating private loans. Federal loans often come with protections such as income-driven repayment plans, loan forgiveness programs, and deferment options. If you consolidate your federal loans with a private lender, you may lose access to these benefits, which could significantly impact your ability to manage your loan repayments.

In terms of practical tips, it's crucial to carefully compare the interest rates and terms offered by different lenders when considering a private loan consolidation. Look for lenders that offer competitive rates and flexible repayment terms. Additionally, consider working with a financial advisor to determine the best consolidation strategy for your specific situation.

Ultimately, while consolidating private loans can be a useful tool for managing your debt, it's important to be aware of the potential drawbacks, including higher interest rates and the loss of federal loan benefits. By carefully weighing the pros and cons and seeking professional advice, you can make an informed decision that best suits your financial goals.

Simplify Your Finances: The Truth About Loan Consolidation Costs

You may want to see also

Explore related products

![]()

Repayment Terms: Terms of repayment might become less favorable when consolidating private loans

Consolidating private loans can indeed impact the terms of repayment, often leading to less favorable conditions. This is primarily because private loans typically have variable interest rates, which can increase over time, unlike federal loans that usually have fixed rates. When consolidating, the new loan may carry a higher interest rate, which can significantly affect the total amount repaid over the life of the loan.

Moreover, private loans often lack the flexible repayment options available with federal loans, such as income-driven repayment plans or loan forgiveness programs. Consolidating private loans into a single loan might result in the loss of these benefits, leading to a more rigid repayment schedule that could be challenging for borrowers, especially those with fluctuating incomes.

Another critical aspect to consider is the potential for losing federal loan protections. Federal loans come with certain safeguards, including deferment and forbearance options, which allow borrowers to temporarily suspend or reduce their payments under specific circumstances. Private loans, on the other hand, rarely offer such protections. Therefore, consolidating private loans might mean giving up these valuable federal loan benefits, making it harder to manage repayment during financial difficulties.

In summary, while consolidating private loans might seem like a convenient way to simplify repayment, it can lead to less favorable terms, higher interest rates, and the loss of federal loan benefits. Borrowers should carefully weigh these potential drawbacks against the benefits of consolidation before making a decision.

Debt Consolidation: A Path to Financial Freedom or a Costly Mistake?

You may want to see also

Explore related products

![]()

Credit Score: The process could potentially impact the borrower's credit score

Consolidating private loans can have a significant impact on a borrower's credit score. When multiple private loans are combined into a single loan, it can affect the borrower's credit utilization ratio, which is a key factor in determining credit scores. A lower credit utilization ratio generally indicates to lenders that the borrower is using credit responsibly and not overextending themselves financially.

The process of consolidating private loans can also lead to a temporary drop in credit scores due to the inquiry made by the lender during the application process. This is known as a hard inquiry and can result in a slight decrease in credit scores for a short period. However, if the borrower continues to make timely payments and manage their credit responsibly, their score will likely recover and potentially improve over time.

It's important for borrowers to carefully consider the terms and conditions of any loan consolidation offer, as some may come with higher interest rates or longer repayment terms that could ultimately harm their credit score. Borrowers should also be aware that consolidating private loans may not always be the best option for improving credit scores, and other strategies such as paying off high-interest debt or disputing errors on credit reports may be more effective in certain situations.

In conclusion, while consolidating private loans can potentially impact a borrower's credit score, the overall effect will depend on various factors such as the borrower's credit utilization ratio, payment history, and the terms of the consolidation loan. Borrowers should carefully weigh the pros and cons of loan consolidation and consider consulting with a financial advisor to determine the best course of action for their individual situation.

Explore related products

![]()

Legal and Financial Implications: There may be significant legal and financial consequences to consider

Consolidating private loans can have significant legal and financial implications that borrowers must carefully consider. One of the primary concerns is the potential loss of federal loan benefits. Federal loans often come with protections such as income-driven repayment plans, loan forgiveness programs, and deferment options that may not be available with private loans. By consolidating private loans, borrowers risk losing these benefits, which could lead to higher monthly payments and a longer repayment term.

Another legal implication to consider is the impact on cosigners. If a private loan has a cosigner, consolidating that loan into a new private loan may require the cosigner's consent and could potentially affect their credit score. Additionally, if the borrower defaults on the consolidated loan, the cosigner may be held responsible for the entire balance, which could have serious financial consequences for them.

From a financial perspective, consolidating private loans can also result in a higher interest rate, especially if the borrower's credit score has decreased since taking out the original loans. This could lead to paying more in interest over the life of the loan. Furthermore, private loans may not offer the same level of customer service or support as federal loans, which could make it more challenging to navigate repayment options or address any issues that arise.

It's also important to note that consolidating private loans may impact the borrower's ability to qualify for future loans or credit. Lenders may view the consolidation as a sign of financial distress, which could negatively affect the borrower's creditworthiness. Additionally, if the borrower is planning to apply for a mortgage or other significant loan in the near future, consolidating private loans could potentially delay or complicate the application process.

In conclusion, while consolidating private loans may seem like an attractive option for simplifying repayment, it's crucial to carefully weigh the legal and financial implications before making a decision. Borrowers should consider consulting with a financial advisor or loan counselor to fully understand the potential consequences and explore alternative options that may better suit their financial situation.