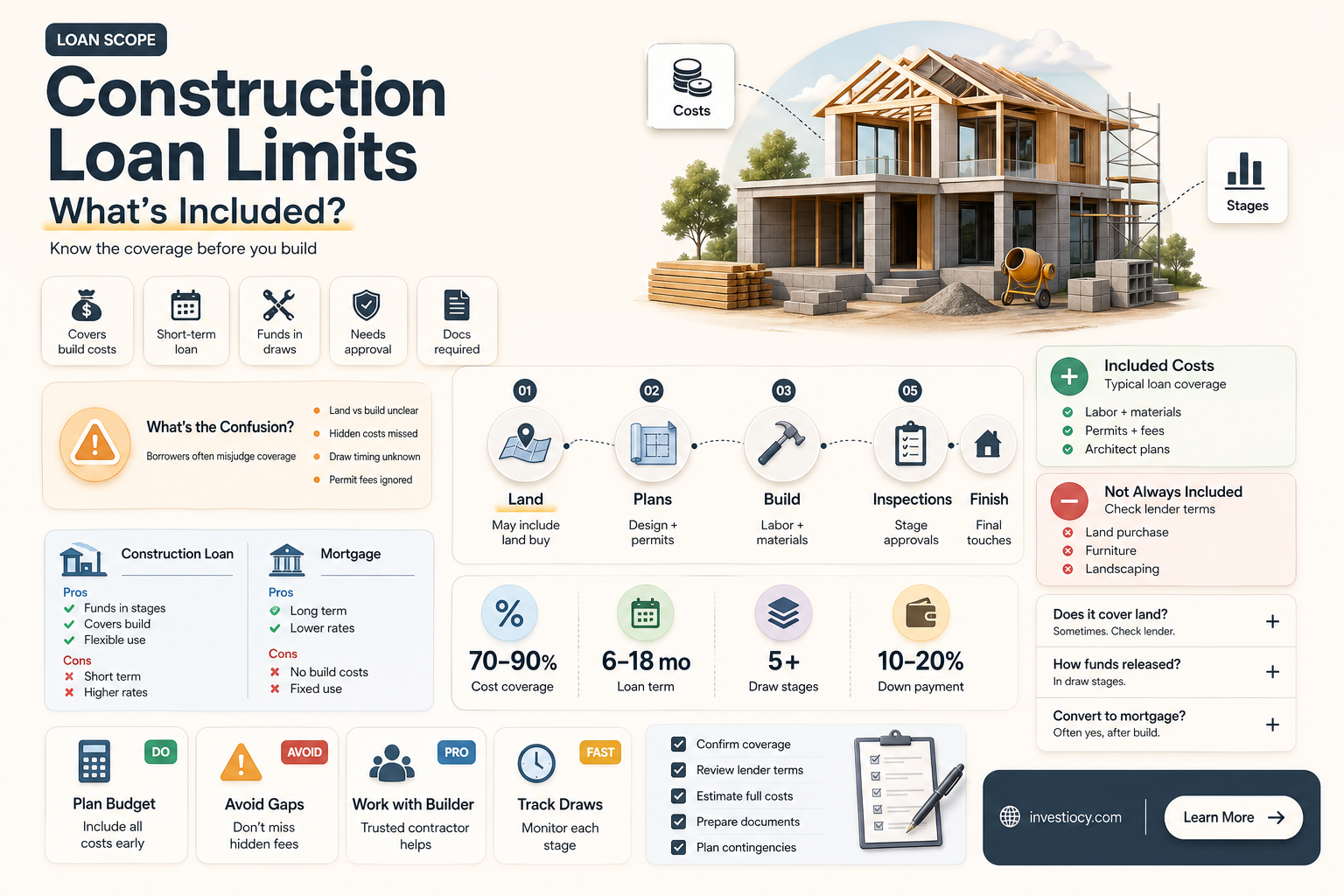

A construction loan is a specialized type of financing designed to cover the costs associated with building or renovating a property. While it can provide substantial financial support, it's important to understand that a construction loan may not cover every single expense related to a construction project. Typically, these loans are structured to fund specific aspects of the construction process, such as land acquisition, materials, labor, and certain construction-related fees. However, they might not include costs like utility hookups, landscaping, or interior finishes unless explicitly stated in the loan agreement. Additionally, construction loans often require a detailed budget and timeline, and funds are usually disbursed in stages as the project progresses. Borrowers should carefully review the terms and conditions of their construction loan to ensure they have adequate funding for all necessary aspects of their project.

Explore related products

$9.99 $19.99

What You'll Learn

- What is Covered: Construction loans typically cover building costs, materials, labor, and land acquisition?

- What is Not Covered: They often exclude furnishings, appliances, and landscaping unless specified?

- Loan Limits: There are usually limits on the total loan amount, based on the project's scope and borrower's qualifications

- Interest Rates: Construction loans may have variable or fixed rates, usually higher than traditional mortgages

- Repayment Terms: Borrowers often need to repay the loan within a short period after construction is completed

![]()

What is Covered: Construction loans typically cover building costs, materials, labor, and land acquisition

Construction loans are designed to cover a wide range of expenses associated with building projects. These loans typically include funds for building costs, materials, labor, and land acquisition. This means that borrowers can use the loan to pay for the construction of a new home, the renovation of an existing property, or the purchase of land for development.

One of the key benefits of construction loans is that they can cover a significant portion of the project's costs. This can be especially helpful for borrowers who may not have the cash on hand to pay for all of the expenses upfront. Additionally, construction loans often have flexible repayment terms, which can make it easier for borrowers to manage their finances during the construction process.

However, it's important to note that construction loans may not cover every single expense associated with a building project. For example, they may not cover the cost of furniture, appliances, or landscaping. Borrowers should carefully review the terms of their loan to understand exactly what is covered and what is not.

In some cases, borrowers may need to secure additional financing to cover expenses that are not included in their construction loan. This could include taking out a separate loan or using a credit card. Borrowers should carefully consider their financial situation and their ability to repay any additional debt before taking on more financing.

Overall, construction loans can be a valuable tool for borrowers who are looking to build or renovate a property. By understanding exactly what is covered by the loan, borrowers can better plan their finances and ensure that they have the funds they need to complete their project.

Understanding Conforming Loan Limits: LTV Ratio Insights

You may want to see also

Explore related products

![]()

What is Not Covered: They often exclude furnishings, appliances, and landscaping unless specified

Construction loans, while comprehensive in many aspects, have specific exclusions that borrowers must be aware of. One of the primary areas not covered by these loans is the cost of furnishings and appliances. This means that if you're planning to outfit your new home with furniture or upgrade your kitchen appliances, you'll need to budget for these expenses separately. The loan will typically cover the construction costs, such as materials and labor, but the finishing touches that make a house a home are generally not included.

Another significant exclusion is landscaping. While the loan may cover the construction of the house itself, the surrounding land and its development are often not part of the package. This includes everything from lawn care and tree planting to the installation of outdoor features like patios or swimming pools. Borrowers who wish to enhance their property's curb appeal or functionality through landscaping will need to allocate additional funds for these projects.

It's important to note that these exclusions can vary depending on the lender and the specific terms of the loan. Some construction loans may offer more inclusive coverage, potentially incorporating some aspects of furnishings, appliances, or landscaping under certain conditions. However, as a general rule, borrowers should anticipate that these items will not be covered and should plan their finances accordingly.

To avoid any surprises, it's crucial for borrowers to carefully review the terms and conditions of their construction loan. This includes understanding what is explicitly covered and what is not, as well as any potential exceptions or clauses that could impact their financial planning. By doing so, borrowers can ensure that they have a comprehensive budget that accounts for all aspects of their home-building project, from the initial construction to the final decorative touches.

Navigating Loan Consolidation: Private vs. Federal Options Explained

You may want to see also

Explore related products

![]()

Loan Limits: There are usually limits on the total loan amount, based on the project's scope and borrower's qualifications

Construction loans, while comprehensive, do come with certain limitations. One of the primary constraints is the loan limit, which is typically determined by the scope of the project and the borrower's qualifications. This means that the total amount you can borrow is capped based on these factors, ensuring that the loan is manageable and that the lender takes on an appropriate level of risk.

For instance, if you're undertaking a large-scale construction project, you might require a higher loan amount to cover the extensive costs involved. However, the lender will assess your ability to repay such a loan, considering factors like your income, credit history, and the projected value of the completed project. If your qualifications don't meet the lender's criteria, you may be offered a lower loan limit or even denied the loan altogether.

On the other hand, smaller projects might have lower loan limits simply because they don't require as much funding. For example, if you're planning a minor renovation, the lender might offer a loan that covers only a portion of the total cost, expecting you to cover the remainder out of pocket or through other means.

It's also important to note that loan limits can vary significantly between different lenders and loan programs. Some lenders might offer more generous limits, while others might be more conservative. Additionally, certain loan programs, such as those backed by the government, might have specific limits and requirements that differ from conventional loans.

Understanding these loan limits is crucial when planning your construction project. It allows you to set realistic expectations and budget accordingly, ensuring that you have enough funds to complete the project without overextending yourself financially. By working within these limits, you can increase your chances of securing the loan and successfully completing your project.

Simplify Your Finances: The Truth About Loan Consolidation Costs

You may want to see also

Explore related products

$103.12 $135.95

![]()

Interest Rates: Construction loans may have variable or fixed rates, usually higher than traditional mortgages

Construction loans often come with variable or fixed interest rates that are typically higher than those of traditional mortgages. This is due to the increased risk associated with construction projects, as lenders must account for the possibility of delays, cost overruns, or other issues that could impact the project's completion and the loan's repayment. Variable rates on construction loans may fluctuate based on market conditions, while fixed rates provide a predictable monthly payment but may be higher overall.

One unique aspect of construction loan interest rates is the potential for a "construction-to-permanent" loan, which allows borrowers to lock in a permanent interest rate during the construction phase. This can provide stability and predictability for borrowers, as they know exactly what their monthly payments will be once the construction is complete. However, this option may come with additional fees or requirements, so borrowers should carefully consider their options before deciding on a construction-to-permanent loan.

Another important consideration for borrowers is the impact of interest rates on their overall construction budget. Higher interest rates can increase the total cost of the project, as more of the loan payments will go towards interest rather than principal. Borrowers should factor in the potential impact of interest rates when creating their construction budget and determining how much they can afford to borrow.

In addition to the interest rate itself, borrowers should also be aware of any additional fees or charges associated with construction loans. These may include origination fees, inspection fees, or other costs that can add up over the course of the loan. By understanding all of the costs associated with a construction loan, borrowers can make more informed decisions about their financing options and ensure that they are getting the best deal possible.

Ultimately, the interest rate on a construction loan is just one of many factors that borrowers must consider when financing their project. By carefully evaluating their options and understanding the potential impact of interest rates on their overall budget, borrowers can make smart decisions that will help them achieve their construction goals while minimizing their financial risk.

Debt Consolidation: A Path to Financial Freedom or a Costly Mistake?

You may want to see also

Explore related products

![]()

Repayment Terms: Borrowers often need to repay the loan within a short period after construction is completed

Borrowers often find themselves in a race against time when it comes to repaying their construction loans. The repayment terms typically require the loan to be repaid within a short period after the completion of the construction project. This can be a significant challenge, especially if the project runs over schedule or budget.

One of the key factors that borrowers need to consider is the interest rate on the construction loan. Interest rates can vary significantly depending on the lender, the borrower's credit history, and the overall economic climate. Borrowers need to be aware of the interest rate and how it will impact their repayment schedule.

Another important consideration is the loan-to-value ratio. This is the percentage of the loan amount compared to the value of the property. Lenders typically have strict guidelines on the loan-to-value ratio, and borrowers need to ensure that they are within these guidelines to avoid any issues with repayment.

Borrowers should also be aware of any prepayment penalties that may apply to their construction loan. Prepayment penalties can be significant, and borrowers need to factor these into their repayment plan.

To ensure that they are able to repay their construction loan within the required timeframe, borrowers should develop a comprehensive repayment plan. This plan should take into account the interest rate, loan-to-value ratio, and any prepayment penalties. Borrowers should also consider their overall financial situation and make sure that they have sufficient funds to cover the loan repayment.

In conclusion, repayment terms for construction loans can be challenging, but borrowers can mitigate these challenges by being aware of the key factors that impact their repayment schedule. By developing a comprehensive repayment plan and considering their overall financial situation, borrowers can ensure that they are able to repay their construction loan within the required timeframe.

Frequently asked questions

A construction loan typically covers most expenses related to building a new home, including land acquisition, construction materials, labor costs, and permits. However, it may not cover every single expense, such as furniture or landscaping, unless these are explicitly included in the loan agreement.

Common items that a construction loan might not cover include furniture, appliances, landscaping, and other finishing touches that are not considered essential to the construction process. Additionally, the loan may not cover any unexpected costs or changes to the original construction plan unless they are approved by the lender.

A construction loan is a short-term loan that covers the costs of building a new home, while a traditional mortgage loan is a long-term loan that covers the purchase of an existing home. Construction loans typically have higher interest rates and require more frequent payments during the construction phase, while mortgage loans have lower interest rates and are paid back over a longer period of time.

The benefits of using a construction loan to build a new home include the ability to finance the construction process without having to pay all the costs upfront, the flexibility to make changes to the construction plan as needed, and the potential to save money by avoiding the costs associated with purchasing an existing home, such as real estate agent fees and closing costs. Additionally, construction loans often have lower down payment requirements than traditional mortgage loans.